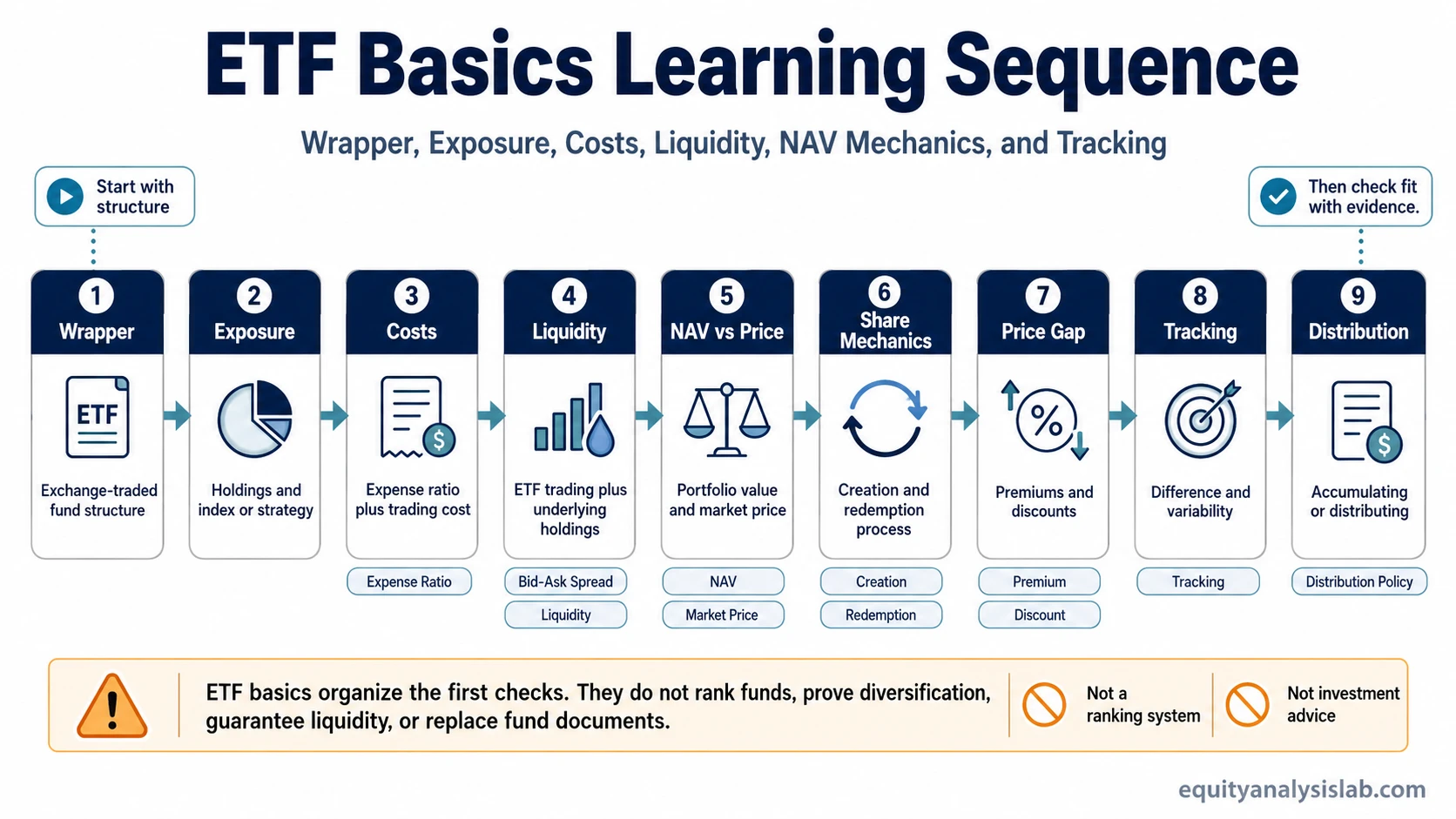

ETF Basics should start with the ETF wrapper, the fund’s exposure, its trading and liquidity mechanics, its costs, and its tracking behavior.

An ETF label does not prove diversification, liquidity, low cost, tax treatment, tracking quality, or portfolio fit. A cleaner sequence is to understand the wrapper first, then examine what the fund holds, how it trades, what it costs, how its market price relates to net asset value, and how closely it follows its intended exposure.

Start With the Core ETF Concepts

ETF basics definition: An exchange-traded fund is a fund wrapper that holds a basket of assets and trades on an exchange during market hours. The wrapper tells you how the fund is packaged and traded, while the holdings and strategy determine the exposure an investor actually receives.

The first distinction is between the fund wrapper and the investment exposure. The word ETF tells you that the fund trades on an exchange, but it does not tell you whether the portfolio is broad, narrow, index-based, active, liquid, low-cost, or suitable for a specific tax situation.

What to Resolve First

- Wrapper: confirm that you understand the fund structure before comparing costs or performance.

- Exposure: look past the fund name and check what the ETF actually holds or tracks.

- Cost: separate ongoing fund cost from trading cost.

- Liquidity: review both ETF trading liquidity and the liquidity of the underlying holdings.

- Price mechanics: understand how market price, NAV, creation and redemption, arbitrage, and premiums or discounts connect.

- Tracking: distinguish long-term tracking outcome from day-to-day tracking variability.

ETF Basics Learning Map

The sequence moves from the ETF wrapper into the mechanics that usually create confusion for investors.

| Question to resolve | Concept to study | Why it comes next |

|---|---|---|

| What is the fund wrapper? | ETF | Start here to separate the exchange-traded fund structure from the assets inside the portfolio. |

| What is the direct trading cost? | bid-ask spread | The spread is part of the real trading cost, especially in funds that do not trade tightly. |

| What is the ongoing fund cost? | expense ratio | The expense ratio affects ownership cost over time, separate from the price paid to enter or exit. |

| Can the ETF trade efficiently? | liquidity in an ETF | ETF liquidity depends on both exchange trading activity and the liquidity of the underlying holdings. |

| What is the fund worth before market-price effects? | net asset value | NAV gives a reference value for the portfolio, while the market price can move above or below it. |

| How are ETF shares created or removed? | creation and redemption | This mechanism helps connect ETF share supply with demand for exposure to the underlying basket. |

| Why can market price differ from NAV? | ETF premium discount | Premiums and discounts show when the market price is above or below the fund’s reference value. |

| What helps align ETF price and portfolio value? | ETF arbitrage | Arbitrage can help reduce gaps between market price and portfolio value, but it is not a guarantee in every market condition. |

| How far did the fund lag or exceed its target? | tracking difference | Tracking difference focuses on the realized gap between fund return and the benchmark or intended exposure. |

| How variable is the tracking gap? | tracking error | Tracking error focuses on the variability of the fund’s return gap over time. |

| How does the ETF handle distributions? | Accumulating vs Distributing ETF | Distribution policy affects whether income is reinvested inside the fund or paid out to investors. |

| Is an ETF the same thing as an index fund? | ETF vs Index Fund | The ETF wrapper describes trading structure, while an index fund describes a strategy that may exist in different fund wrappers. |

Priority Path Notes

Begin with structure before judging cost or tracking. Two funds can both be ETFs while holding very different assets, following different rules, trading with different spreads, and producing different tracking results.

After the wrapper and exposure are clear, compare the two cost layers. The expense ratio is the recurring fund-level cost, while the bid-ask spread is part of the trading cost when entering or exiting the fund.

Next, separate market price from portfolio value. NAV gives a reference point for the underlying basket, while creation and redemption, arbitrage, and premium or discount behavior help explain why market price usually stays close to that value but can still diverge.

Finally, review tracking. Tracking difference asks how far the ETF’s realized return moved away from the intended benchmark or exposure. Tracking error asks how unstable that gap was across the measurement period.

A Simple Learning Sequence Example

For example, an investor comparing two broad equity ETFs should not stop at the fund names. The first check is whether both funds hold the same kind of exposure. The second check is whether one fund has a wider spread or weaker trading depth. The third check is whether ongoing cost, NAV behavior, and tracking history change the comparison. The ETF label is only the starting point.

When an ETF Label Can Be Misleading

An ETF name can suggest a theme, region, sector, index, factor, or asset class, but the label does not prove what the fund actually owns. Holdings, weighting rules, index methodology, active-management rules, derivatives exposure, currency exposure, and distribution policy can all change the investor’s real exposure.

The label also does not prove liquidity. A fund can trade on an exchange and still have wide spreads, limited trading depth, or underlying holdings that are harder to transact during stressed market conditions.

The label does not prove low cost. A fund may be exchange-traded while still carrying a higher expense ratio, trading cost, or tracking drag than a similar alternative.

What ETF Basics Should Not Be Used For

ETF basics can help organize the first checks, but they should not be treated as an ETF ranking system, an investment recommendation, or portfolio allocation advice.

- An ETF label does not prove diversification.

- An ETF wrapper does not prove low cost.

- Exchange trading does not prove strong liquidity.

- NAV alignment does not eliminate premium or discount risk.

- Tracking history does not guarantee future tracking quality.

- Distribution policy does not automatically create a better tax result.

- Broad exposure does not prove portfolio fit.

Fund documents, provider data, holdings files, expense disclosures, trading data, and tax information are still needed before drawing fund-specific conclusions.

FAQ

What should I learn first in ETF basics?

Start with the ETF wrapper, then check exposure, cost, liquidity, NAV and market price mechanics, creation and redemption, tracking, and distribution policy.

Is an ETF automatically diversified?

No. An ETF can be broad or narrow depending on what it holds and how the portfolio is weighted. The holdings and methodology matter more than the wrapper label.

Is ETF liquidity only about trading volume?

No. Trading volume matters, but ETF liquidity also depends on spreads, market-making conditions, and the liquidity of the underlying holdings.

What is the difference between tracking difference and tracking error?

Tracking difference describes the realized return gap between the ETF and its benchmark or intended exposure. Tracking error describes how variable that gap is over time.