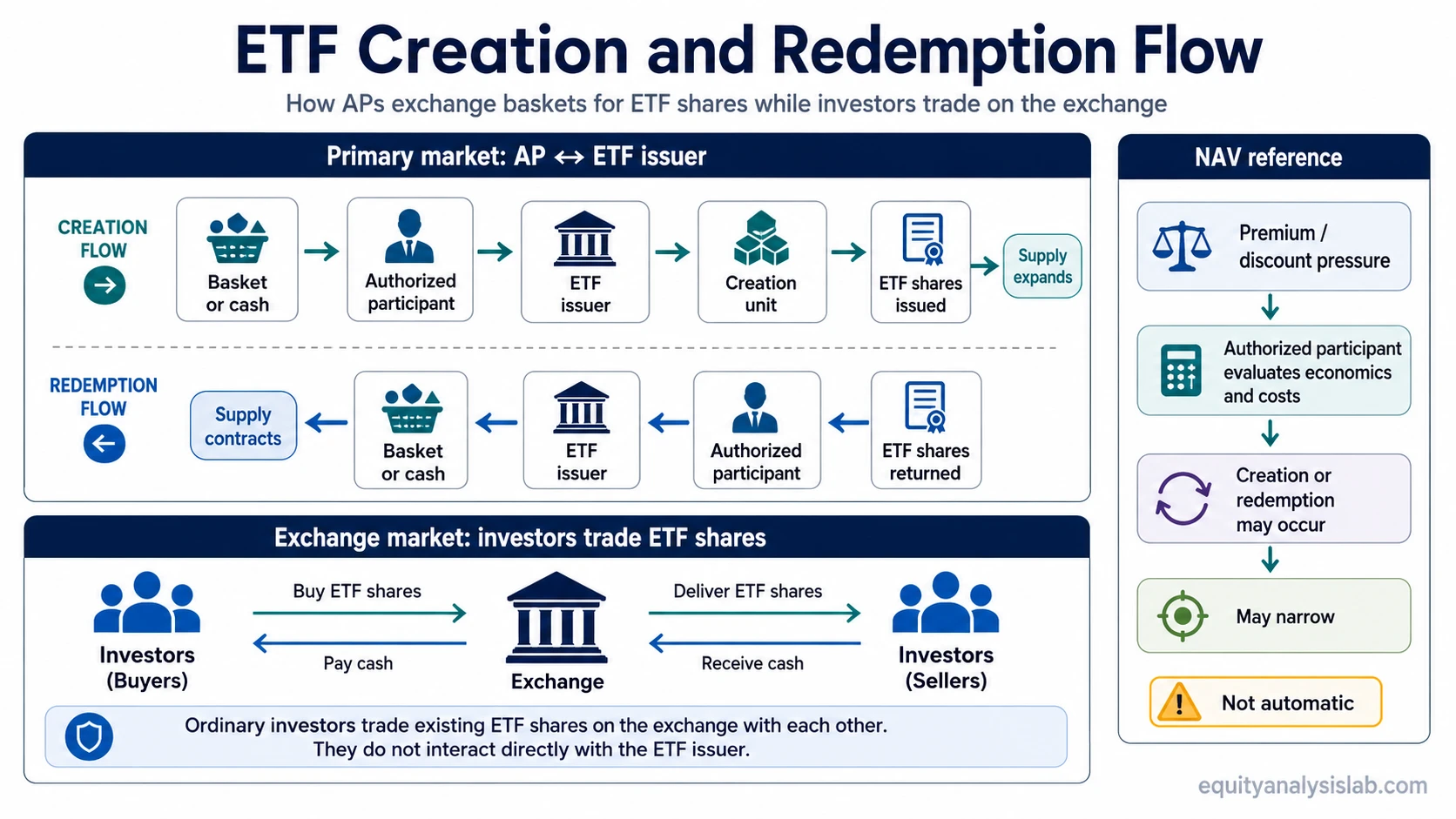

ETF creation and redemption is the primary-market mechanism that lets authorized participants exchange a basket of securities or cash with an ETF issuer for ETF shares, or return ETF shares to receive the basket or cash back.

Authorized participants, often called APs, are the institutional firms that interact directly with the ETF. Ordinary investors usually do not create or redeem ETF shares with the fund. They buy and sell existing ETF shares on an exchange, where trading costs, order execution, and the bid-ask spread matter.

The creation and redemption mechanism helps ETF share supply adjust when demand changes. It can support market-price alignment with NAV, but it does not guarantee perfect tracking, unlimited liquidity, or a specific tax result for every investor.

What ETF Creation and Redemption Means

ETF creation happens when an authorized participant delivers a specified basket of securities, or sometimes cash, to the ETF and receives a large block of newly issued ETF shares called a creation unit.

ETF redemption works in the opposite direction. The authorized participant returns ETF shares to the fund and receives the underlying basket or cash. The returned ETF shares are removed from circulation.

The mechanism belongs to the ETF primary market. Exchange trading between ordinary buyers and sellers belongs to the secondary market. That distinction is central: most investors experience ETF liquidity through the exchange, while APs handle fund-level share creation and redemption.

Key Points

- Creation and redemption happen between authorized participants and the ETF issuer.

- Ordinary investors usually trade ETF shares on exchanges rather than with the fund itself.

- Creation units are large blocks of ETF shares, not the small share quantities most investors trade.

- The mechanism can help ETF market prices stay closer to NAV when premiums or discounts appear.

- Creation and redemption support ETF efficiency, but they do not remove all liquidity, tracking, cost, or tax considerations.

How ETF Creation Works

ETF creation begins when demand for ETF shares is strong enough that new shares may be useful. An authorized participant assembles the required basket of securities, or provides cash if the fund uses cash creation, and delivers it to the ETF.

The ETF then issues a creation unit to the AP. That creation unit is a large block of ETF shares. The AP can hold those shares, sell them into the secondary market, or use them as part of a market-making process.

The economic point is supply adjustment. When more ETF shares are needed, the creation process can increase the number of shares outstanding without the ETF manager having to sell shares directly to each ordinary investor.

How ETF Redemption Works

ETF redemption runs the same mechanism in reverse. An authorized participant gathers ETF shares, returns them to the fund, and receives the underlying basket of securities or cash from the ETF.

After redemption, the ETF shares returned by the AP are removed from circulation. Share supply can shrink when market demand for the ETF falls or when the AP can use redemption to reconnect ETF share pricing with the value of the underlying holdings.

Redemption is also one reason ETFs may be operationally different from some other pooled vehicles. In-kind redemptions can reduce the need for the fund to sell holdings inside the portfolio, although tax outcomes depend on fund structure, jurisdiction, and investor circumstances.

Creation vs Redemption vs Secondary-Market Trading

Creation, redemption, and exchange trading are often discussed together, but they are not the same transaction.

| Mechanism | Who participates | What happens | Investor boundary |

|---|---|---|---|

| Creation | Authorized participant and ETF issuer | The AP delivers a basket or cash and receives newly issued ETF shares. | Ordinary investors usually do not create ETF shares directly. |

| Redemption | Authorized participant and ETF issuer | The AP returns ETF shares and receives the basket or cash from the fund. | Ordinary investors usually do not redeem ETF shares directly with the ETF. |

| Secondary-market trading | Investors, brokers, market makers, and exchanges | Existing ETF shares trade between buyers and sellers on an exchange. | This is the level most ordinary investors interact with. |

Why Authorized Participants Matter

Authorized participants connect the ETF portfolio to the exchange-traded share price. They are not simply large ordinary investors. Their role is operational: they can transact directly with the fund in large blocks and use the creation or redemption process when the ETF share price diverges from the value of the underlying holdings.

That AP role is one reason the ETF wrapper can adjust share supply more flexibly than a fixed pool of shares. The mechanism still depends on market conditions, the liquidity of the underlying basket, AP willingness to transact, and the costs of carrying out the trade.

Why Creation and Redemption Matter for NAV

An ETF has an underlying net asset value, or NAV, based on the value of its portfolio holdings. The ETF share price can trade above NAV at a premium or below NAV at a discount.

When an ETF trades above NAV, an authorized participant may be able to deliver the underlying basket, receive newly created ETF shares, and sell those shares in the market. That additional supply can help reduce the premium. When an ETF trades below NAV, the AP may buy ETF shares, redeem them with the fund, and receive the underlying basket. That can help reduce the discount.

Operational Sequence

Premium or discount pressure appears → the AP evaluates basket economics, transaction costs, and market risk → creation or redemption may occur → ETF share supply expands or contracts → premium or discount pressure may narrow.

This relationship is closely connected to ETF arbitrage, but creation and redemption are the fund-level mechanism rather than the full price/NAV trading logic. The mechanism can support alignment; it does not force every ETF to trade exactly at NAV at every moment.

A Premium and Discount Scenario

An ETF can trade above the estimated value of its underlying basket when exchange demand for the ETF shares is stronger than available supply. An authorized participant may respond by delivering the basket to the fund, receiving newly created ETF shares, and selling those shares into the market. The trade only makes sense if the premium is large enough after transaction costs, execution risk, and settlement considerations.

The reverse can happen when an ETF trades below the value of its underlying basket. An AP may buy ETF shares in the market, redeem them with the fund, and receive the basket. That can help reduce the discount, but the process is not automatic. Market stress, less liquid holdings, AP balance-sheet capacity, and timing differences can all affect whether redemption is practical.

What Investors Should Check

Creation and redemption explain part of how ETF structure works, but they should not be treated as a shortcut for evaluating an ETF. Several checks still matter for an ordinary investor.

| Check | Why it matters | What not to assume |

|---|---|---|

| Premium or discount to NAV | Shows whether ETF shares are trading above or below the estimated value of the portfolio. | Do not assume every premium or discount disappears instantly. |

| Bid-ask spread | Shows the visible trading cost faced by exchange buyers and sellers. | Do not treat fund-level creation/redemption as the same thing as your execution spread. |

| ETF liquidity and underlying holdings | The ETF’s trading volume is only one part of liquidity; the underlying basket also matters. | Do not assume the ETF is more liquid than the market for what it owns. |

| Tracking behavior | Shows how closely ETF performance follows the intended exposure over time. | Do not assume creation and redemption remove all tracking difference or tracking error. |

| Tax and distribution mechanics | Fund structure can affect taxable events, distributions, and investor reporting. | Do not assume in-kind mechanics guarantee the same tax result for every investor. |

The ETF liquidity picture is especially important when the underlying holdings are less liquid than the ETF shares appear to be. A narrow spread and active AP participation can help, but liquidity still depends on what the fund owns and how easily those holdings can be traded.

The expense ratio is separate from creation and redemption. It affects long-term fund cost, while creation and redemption explain how ETF share supply can expand or contract.

Common Misunderstandings

- Retail investors do not usually create or redeem directly. Creation and redemption are normally handled by authorized participants in large blocks.

- Share supply flexibility is not unlimited liquidity. The mechanism can help, but stressed markets, less liquid holdings, or high transaction costs can still widen premiums, discounts, and spreads.

- In-kind mechanics do not guarantee tax outcomes. ETF structure may support tax efficiency in some settings, but investor-level tax results depend on the fund, jurisdiction, account type, holding period, and transaction history.

- Arbitrage does not erase every premium or discount immediately. The opportunity must be large enough after costs, operational constraints, and market risk.

- Creation and redemption are not fund selection signals. They explain ETF structure; they do not make a specific ETF attractive or unattractive by themselves.

Related ETF Concepts

The ETF structure combines fund ownership with exchange trading. Creation and redemption explain the primary-market share mechanism inside that structure.

NAV gives the portfolio reference value. ETF arbitrage explains the price/NAV reconnect logic. ETF liquidity explains the trading and underlying-market depth behind execution quality. Bid-ask spread and expense ratio separate exchange-level trading cost from recurring fund cost.

FAQ

Can ordinary investors create or redeem ETF shares directly?

Usually no. Ordinary investors normally buy and sell ETF shares on an exchange. Creation and redemption are usually handled by authorized participants in large blocks with the ETF issuer.

Does creation and redemption keep an ETF exactly at NAV?

No. The mechanism can help ETF market prices stay closer to NAV, but premiums and discounts can still appear because of transaction costs, market stress, timing, liquidity, or AP participation limits.

Is ETF creation and redemption the same as ETF arbitrage?

No. Creation and redemption are the fund-level process. Arbitrage is the price/NAV trading logic that may use that process when the economics are attractive.

Does in-kind redemption guarantee tax efficiency?

No. In-kind mechanics can support tax efficiency in some ETF structures, but investor tax outcomes depend on the fund, jurisdiction, account type, distributions, and the investor’s own transactions.