A bid-ask spread is the gap between the highest price buyers are currently willing to pay and the lowest price sellers are currently willing to accept. For an exchange-traded fund wrapper, that gap affects the price an investor may receive when buying or selling ETF shares on an exchange, separate from the fund’s ongoing expense ratio.

The spread is not a fee charged by the fund sponsor. It is an exchange-trading friction created by the difference between quoted buying interest and quoted selling interest. A narrow spread usually means buyers and sellers are close together. A wide spread means the market price needed to transact may be farther away from the opposite side of the quote.

Key Points

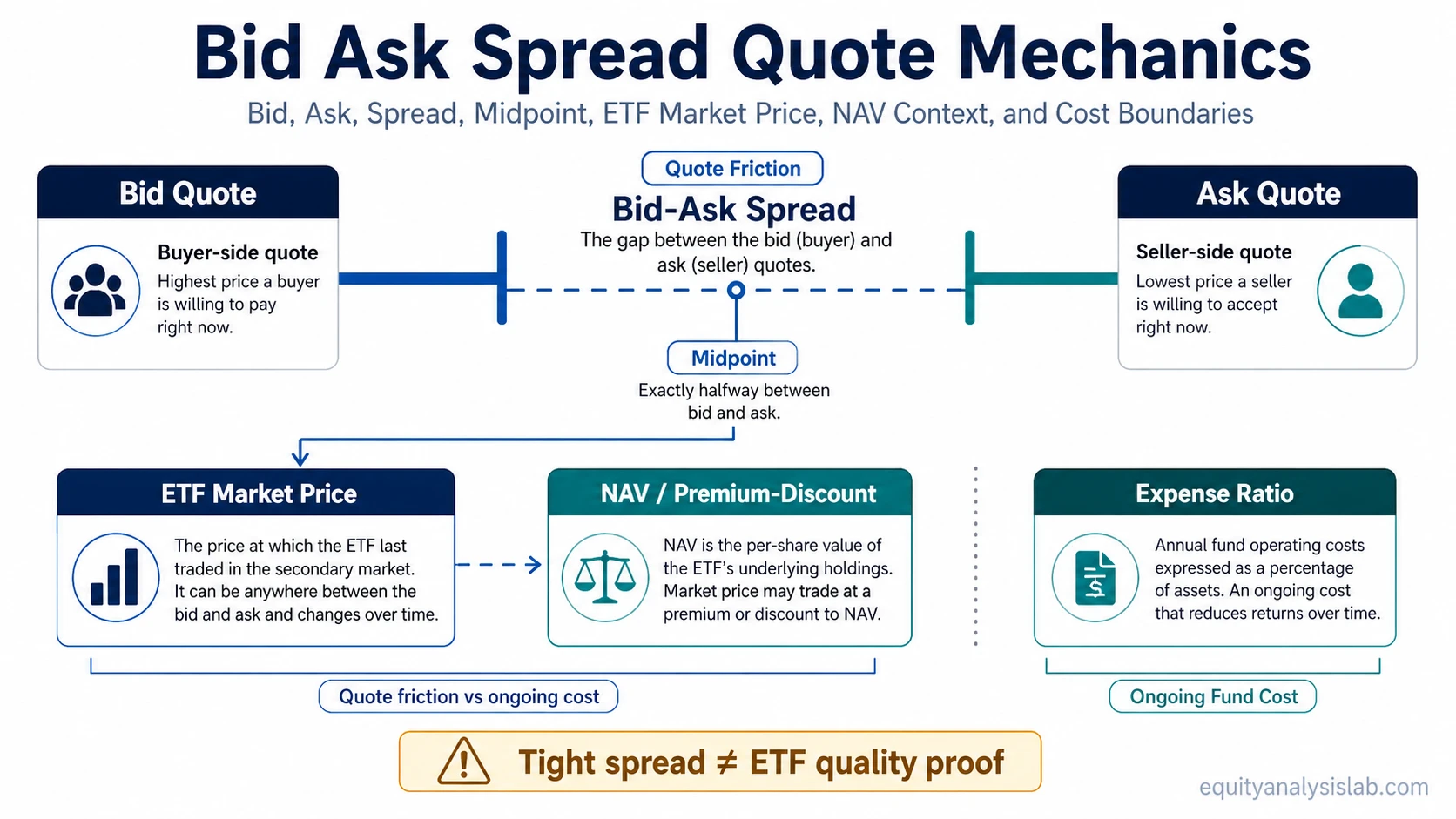

- The bid is the price buyers are currently showing.

- The ask is the price sellers are currently showing.

- The bid-ask spread equals ask price minus bid price.

- For ETFs, the spread is a trading-cost layer, not the same thing as the expense ratio.

- A spread can reflect liquidity, liquidity-provider activity, underlying basket liquidity, and market conditions, but it does not prove ETF quality or suitability.

What Bid, Ask, and Spread Mean

ETF shares trade on an exchange, so the visible quote usually has two sides. The bid shows where buyers are currently willing to buy. The ask shows where sellers are currently willing to sell. The spread is the distance between those two prices.

| Quote item | What it means | Why it matters for an ETF investor |

|---|---|---|

| Bid price | The highest displayed price buyers are willing to pay. | It indicates the current buying side of the market. |

| Ask price | The lowest displayed price sellers are willing to accept. | It indicates the current selling side of the market. |

| Bid-ask spread | The gap between ask and bid. | It shows the immediate quote friction around the ETF’s market price. |

| Last price | The price of the most recent completed transaction. | It may not match the current bid or ask, especially when quotes move or trading is less active. |

The last price can be useful context, but it is not the same as the current executable quote. If the last ETF trade occurred at $50.00 and the current quote is $49.95 bid and $50.05 ask, the current quote gap is still $0.10 even though the last price sits between the two sides.

Bid Ask Spread Formula

The basic bid ask spread formula is:

Bid-ask spread = Ask price – Bid price

A percentage spread can make the quote gap easier to compare across ETFs with different share prices:

Percentage spread = (Ask price – Bid price) / Midpoint price × 100

For example, if an ETF is quoted at a $49.98 bid and a $50.02 ask, the dollar spread is $0.04. The midpoint is $50.00, so the percentage spread is 0.08%. This example is illustrative only. It shows how the quote gap is measured, not whether the ETF is attractive, liquid enough, or appropriate for a portfolio.

| Input | Example value | Calculation role |

|---|---|---|

| Bid | $49.98 | Current buying side |

| Ask | $50.02 | Current selling side |

| Dollar spread | $0.04 | $50.02 minus $49.98 |

| Midpoint | $50.00 | Average of bid and ask |

| Percentage spread | 0.08% | $0.04 divided by $50.00 |

Why ETF Bid Ask Spreads Become Narrow or Wide

ETF bid-ask spreads are shaped by more than the number of shares traded in the ETF itself. Market makers and other liquidity providers may adjust ETF quotes based on current trading interest, underlying basket liquidity, hedging difficulty, volatility, and how easily the ETF’s market price can be related to estimated fund value.

When the underlying securities are easy to trade and the ETF has steady two-sided interest, market makers may be able to quote tighter spreads. When the underlying basket is harder to price, less liquid, or moving quickly, spreads can widen because quote providers face more uncertainty.

| Factor | How it can affect the spread | Interpretation limit |

|---|---|---|

| ETF trading activity | More consistent two-sided interest can support tighter quotes. | Trading volume alone does not fully explain ETF liquidity. |

| Underlying basket liquidity | Harder-to-trade holdings can make quoting the ETF more expensive or uncertain. | The ETF may still trade even when some underlying holdings are less active. |

| Market volatility | Fast price movement can widen quotes as market makers adjust risk. | A temporarily wide spread does not automatically mean the ETF is structurally weak. |

| Time and market conditions | Spreads can change when underlying markets are closed, just opened, or under stress. | One quote snapshot should not be treated as a permanent liquidity profile. |

| Fund structure and exposure | International, fixed-income, or niche exposures may have different quote behavior from broad domestic equity ETFs. | Spread comparison is most useful when ETFs have comparable exposure and market context. |

The spread is one visible piece of liquidity conditions around the fund. It should be read together with trading volume, market depth, underlying asset liquidity, and the fund’s price relationship to its estimated value.

Bid Ask Spread vs Expense Ratio, NAV, and ETF Liquidity

A bid-ask spread is easiest to misread when it is mixed with other ETF cost and pricing concepts. The spread affects the exchange price at the point of transaction. The expense ratio is an ongoing fund operating cost. NAV and premium or discount compare the ETF’s market price with the value of its holdings.

| Concept | What it describes | How it differs from bid-ask spread |

|---|---|---|

| Bid-ask spread | The gap between current bid and ask quotes. | It is an exchange-trading friction visible in the quote. |

| Expense ratio | The fund’s annual operating cost as a percentage of assets. | It is an ongoing fund cost, not a quote gap. |

| ETF liquidity | The ability to trade ETF shares efficiently, supported by secondary-market and underlying-market conditions. | It is broader than the displayed spread at one moment. |

| NAV and premium/discount | The relationship between ETF market price and the value of fund holdings. | It measures price-value alignment, not the width of the quote. |

| Creation and redemption | The primary-market process that allows ETF shares to be created or removed through authorized participants. | It supports ETF share supply mechanics rather than defining the displayed spread. |

| ETF arbitrage | The mechanism that can pressure ETF market price toward the value of the underlying basket. | It can influence alignment, but it does not make every spread disappear. |

The creation and redemption process helps explain how ETF share supply can adjust in the primary market.

The ETF arbitrage mechanism helps explain why market price and fund value often remain connected, but it does not remove the need to observe the actual bid and ask quotes.

What the Spread Can and Cannot Tell You

A bid-ask spread can show immediate quote friction. It can also provide a visible clue about how easily ETF shares are being quoted under current conditions. That makes it useful for interpreting trading costs and liquidity, especially when comparing similar funds or looking at the same fund across different market environments.

- A tight spread does not prove an ETF is suitable for a portfolio.

- A wide spread does not automatically prove the ETF is poor quality.

- The displayed spread can change with market conditions, volatility, and underlying asset availability.

- The spread does not include every possible cost or tax consequence.

- The spread should not be used as a standalone valuation, diversification, or return signal.

The useful interpretation is narrower: the spread shows the current distance between quoted buyers and sellers. For ETF analysis, it belongs next to expense ratio, exposure, fund structure, underlying liquidity, and price-value alignment, not above them.

Common Mistakes When Reading Bid Ask Spread

- Mistaking the spread for the expense ratio: the spread is transaction friction, while the expense ratio is an ongoing fund cost.

- Using the last price as the current quote: the last completed trade may not match the current bid or ask.

- Assuming ETF volume tells the whole liquidity story: underlying basket liquidity and market-maker participation can matter as well.

- Treating a tight spread as an ETF recommendation: a tight quote does not evaluate exposure, risk, fees, tax profile, or portfolio fit.

- Ignoring market context: spreads can behave differently during volatile periods, around market open or close, or when underlying markets are not fully active.

How Bid Ask Spread Fits Into ETF Analysis

Bid-ask spread is a market quote concept, but it has a specific role inside ETF analysis. It helps separate the cost of accessing the ETF’s market price from the fund’s ongoing operating cost and from the value of the holdings inside the portfolio.

A practical review can treat the spread as one observable layer: first identify what the ETF owns, then look at ongoing costs, then compare the current quote behavior with the fund’s liquidity profile and market-price relationship to value. The spread is most useful when it is compared across similar exposures, current quote depth, ongoing costs, and price-value alignment rather than read as a standalone ETF-quality score.

FAQ

What is a bid ask spread?

A bid ask spread is the difference between the highest price buyers are currently willing to pay and the lowest price sellers are currently willing to accept. In ETFs, it appears as the gap between the bid and ask quotes for ETF shares on an exchange.

What is the bid ask spread formula?

The basic formula is ask price minus bid price. A percentage spread can be calculated by dividing that dollar spread by the midpoint price and multiplying by 100.

Is the bid ask spread the same as an ETF expense ratio?

No. The bid ask spread is an exchange-trading friction visible in the quote. The expense ratio is the fund’s ongoing annual operating cost as a percentage of assets.

Does a narrow ETF spread mean the ETF is better?

No. A narrow spread can indicate lower immediate quote friction, but it does not prove ETF quality, suitability, diversification, valuation, or expected return.

Why can ETF spreads widen?

ETF spreads can widen when market volatility rises, underlying holdings become harder to price or trade, liquidity-provider risk increases, or trading conditions become less stable.