Business quality in investment analysis means reviewing whether a company’s economics, competitive position, cash generation, and management choices can support a durable thesis.

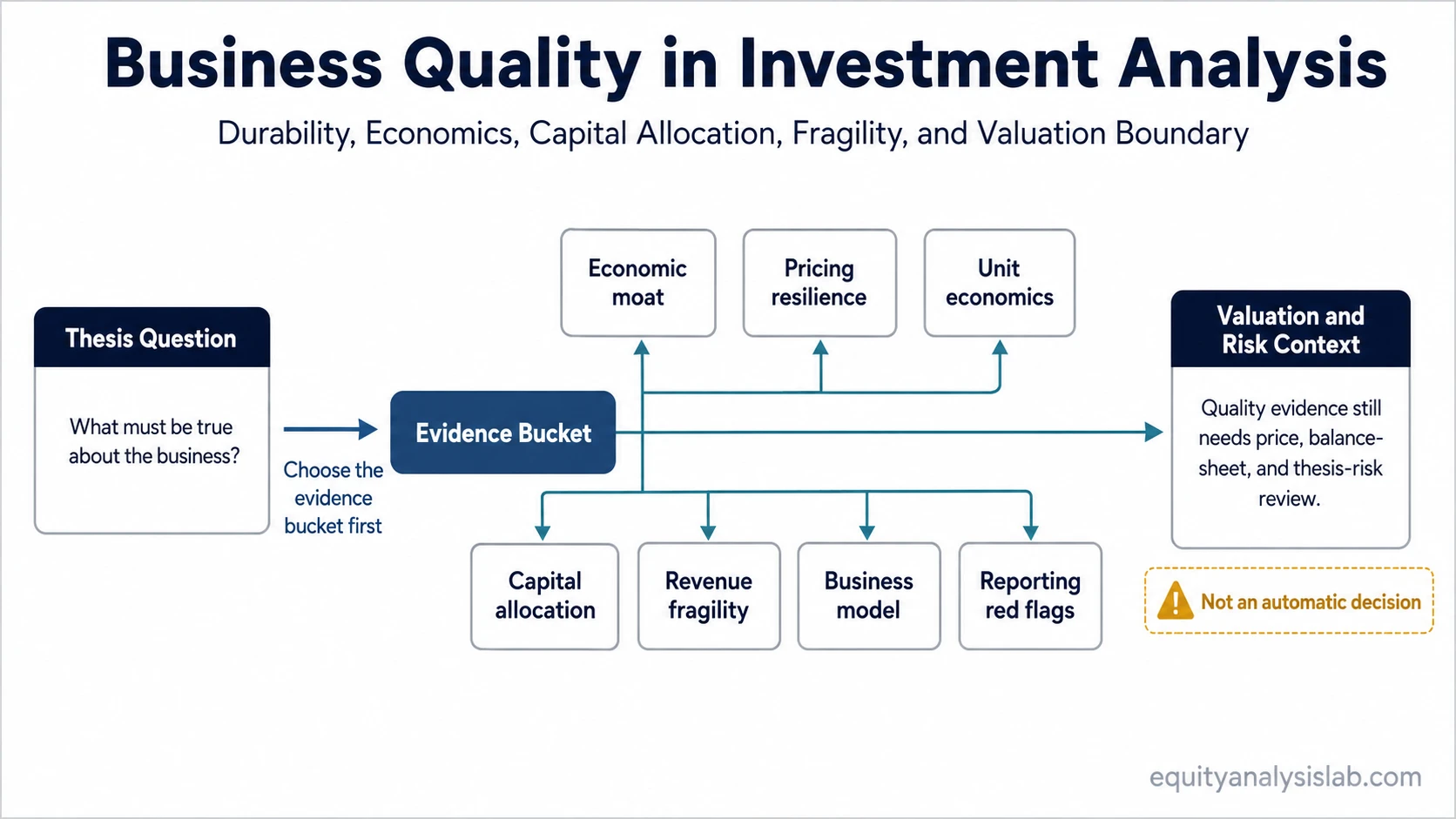

The useful starting point is not one universal score. The better starting point is the evidence bucket that matters most: durability, pricing resilience, operating economics, reinvestment discipline, revenue fragility, or accounting warning signs.

It helps choose which evidence to inspect first; it does not decide whether the stock is automatically attractive.

Definition: Business quality is the company-analysis lens used to test whether a business can defend economics, convert activity into cash, allocate capital sensibly, and avoid fragility that can damage an investment thesis.

Key Points

- Business quality organizes evidence; it does not prove that a stock is attractive.

- Durability usually starts with competitive position, pricing resilience, and the economics behind each sale or customer relationship.

- Management choices matter when cash generation depends on reinvestment, buybacks, debt reduction, or acquisition discipline.

- Quality evidence still needs valuation, balance-sheet, and thesis-risk context before it can support an investor decision.

What Business Quality Means in Investment Analysis

Business quality connects the operating company to the investment thesis. A company may have an admired product, a recognizable brand, or strong revenue growth, but those observations are incomplete unless margins, cash flow, competition, reinvestment needs, and balance-sheet pressure support the story.

The strongest analysis separates business strength from stock attractiveness. A durable business can still be priced for too much optimism. A weaker business can look statistically cheap while carrying risks that the valuation multiple does not fully show.

A business-quality review also separates market pressure from business damage. A broad selloff can move the share price without proving that the company thesis is broken. The analytical question remains whether the business model, economics, cash generation, and competitive position have changed.

Which Business Quality Evidence to Check First

Different investor questions point to different evidence buckets. The route should start with the weakness, uncertainty, or thesis dependency that matters most rather than treating every company with the same checklist.

| Investor question | Business-quality evidence | Deeper concept | Why it matters |

|---|---|---|---|

| Can the company defend its economics over time? | Competitive position, switching costs, brand strength, network effects, or cost advantage | economic moat | Durability depends on whether competitors can erode returns, margins, or customer relationships. |

| Can margins hold when costs, competition, or demand change? | Ability to raise prices without losing too much volume or customer trust | pricing power | Margin resilience often depends on whether value to the customer supports price increases. |

| Does growth create attractive economics or just more activity? | Contribution margin, customer acquisition cost, retention, payback period, and gross profit structure | unit economics | Growth is more useful when each incremental customer, product, or transaction supports cash-flow quality. |

| Does management turn cash into long-term value? | Reinvestment choices, acquisitions, debt reduction, dividends, buybacks, and capital discipline | capital allocation | Strong operations can be weakened if cash is reinvested poorly or financial flexibility is reduced. |

| Is revenue more fragile than it first appears? | Dependence on one customer, one contract, one channel, or one buying group | customer concentration risk | A concentrated revenue base can make reported growth less durable than headline numbers suggest. |

| How does the company actually make money? | Revenue model, cost structure, customer behavior, competitive position, and operating leverage | business model analysis | The business model explains the engine behind revenue, margins, reinvestment needs, and risk exposure. |

| Do reported numbers conflict with the thesis? | Cash-flow mismatch, margin deterioration, leverage pressure, aggressive accounting, or unusual working-capital signals | financial statement red flags | Accounting and cash-flow warnings can reveal business-quality risk before the narrative changes. |

Priority Paths for a Business Quality Review

When durability is the main question, begin with competitive advantage. A company with high margins may still face pressure if competitors can copy the product, undercut pricing, or weaken customer retention.

When growth is the main attraction, operating economics should come first. Revenue expansion carries more weight when the underlying units produce acceptable margins, repeat behavior, and cash-flow support rather than relying only on scale promises.

If margin pressure is central, pricing resilience becomes the first test. A company may report healthy demand, but weak pricing power can make that demand less valuable when input costs rise or competitors become more aggressive.

When free cash flow drives the thesis, management’s use of cash deserves earlier review. Reinvestment, buybacks, acquisitions, and balance-sheet choices can strengthen or dilute business quality depending on discipline and timing.

If revenue depends on a narrow base, fragility should be reviewed before headline growth is trusted. A single customer, contract, distribution channel, or supplier relationship can make business quality more conditional than the headline growth rate suggests.

Where Business Quality Can Mislead

Business quality can become misleading when it is treated as a complete investment decision. A strong business does not automatically make a stock attractive, and a low valuation does not automatically fix weak economics.

Limitation: Quality evidence must be checked against valuation, balance-sheet risk, cash-flow durability, and the assumptions already reflected in the stock price. A durable company can be overpriced if the valuation already assumes too much future success.

Product admiration is another common mistake. A product can be useful, popular, or personally impressive while the company still has weak margins, poor cash conversion, heavy reinvestment needs, or fragile competitive positioning.

Business quality should also avoid one-metric shortcuts. High margins, high returns on capital, strong revenue growth, or low debt can each support a thesis, but none of them explains the full business without context.

Simple Business Quality Routing Example

A company reports steady revenue growth and strong customer demand, but margins are flattening while sales and marketing costs remain high. The first question is not whether the company is high quality in a broad sense. The first check is whether the operating engine creates attractive economics after customer acquisition costs, retention, and gross profit are considered.

If each incremental customer supports cash generation, the review can move toward durability and reinvestment discipline. If growth depends on constant spending without clear payback, the business-quality claim remains incomplete even before valuation is considered.

What Belongs Outside the Business Quality Review

Business quality does not replace valuation work, portfolio sizing, risk tolerance, or a full investment thesis. It supplies one part of the evidence base: whether the company itself has durable economics and manageable fragility.

Deep moat taxonomy, detailed pricing-power measurement, full unit-economics mechanics, accounting red-flag checklists, and complete capital-allocation frameworks require more focused analysis. Business-quality analysis is strongest when it identifies the evidence that most directly tests the thesis before moving into valuation or portfolio judgment.

FAQ

Is business quality enough to make a stock attractive?

No. Business quality is only one part of analysis. Valuation, balance-sheet risk, cash-flow durability, portfolio fit, and thesis assumptions still need separate review.

What is the first thing to check in business quality analysis?

The first check depends on the thesis risk. Durability points toward competitive advantage, margin pressure points toward pricing power, growth quality points toward unit economics, and fragility points toward concentration or accounting warnings.