Pricing power is a company’s ability to raise prices without materially weakening demand, customer retention, volume, or margin quality. For investors, the useful test is not the price increase by itself. The useful test is what happens after the increase: whether customers stay, whether volumes hold, whether margins improve for the right reasons, and whether competitors are unable to take share easily.

Pricing power means: a business can charge more while preserving enough customer demand and economic value to support durable margin quality. It is strongest when higher prices reflect real customer value, limited substitutes, switching friction, or a hard-to-replace product rather than temporary inflation, weak competition, or short-term discount withdrawal.

- Pricing power is about the relationship between price, demand, retention, and margin quality.

- A higher selling price is not enough; investors need evidence that customers continue to accept the value proposition.

- The evidence becomes more useful when it appears across margins, volume behavior, customer retention, and competitive conditions.

- Pricing power can weaken when substitutes improve, customer budgets tighten, or the company must spend heavily to preserve demand.

What pricing power means for investors

Pricing power reveals how much control a company may have over the economics of its product or service. A business with pricing power does not depend only on selling more units to protect profitability. It may be able to defend margins when input costs rise, wages increase, distribution costs change, or competitors discount aggressively.

The investor question is not whether management raised prices. The question is whether the business still looks strong after customers respond. If higher prices are followed by stable demand, limited churn, healthy gross margins, and restrained discounting, pricing power may be part of the company’s business-quality profile.

Pricing power also needs context. A company can report stronger margins because of temporary cost relief, accounting mix, lower promotions, or a short-term supply shortage. Those outcomes may help results for a period, but they do not automatically show durable customer acceptance.

Pricing power and demand sensitivity

The core boundary is demand sensitivity. A company has stronger pricing power when customers absorb a price increase without quickly reducing purchases, switching providers, delaying orders, or demanding offsetting concessions.

Demand does not have to be perfectly unchanged. Some volume pressure can still be acceptable if the company earns better unit economics and keeps the most valuable customers. The pricing-power case becomes weaker when price increases create broad volume decline, higher churn, heavier discounts, or faster competitive share loss.

Useful distinction: a price increase is an action; pricing power is the market’s response to that action. The response is visible in customer behavior, competitive alternatives, margin quality, and the company’s ability to repeat price increases without damaging the franchise.

Where pricing power comes from

Pricing power usually comes from some form of customer dependence, differentiated value, limited alternatives, or structural advantage. The source matters because not every source is equally durable.

| Source | Why it can help | What can weaken it |

|---|---|---|

| Brand trust | Customers may accept higher prices when the brand reduces uncertainty or signals quality. | Brand value can fade if quality slips, cheaper substitutes improve, or customers become more price-sensitive. |

| Switching costs | Customers may stay because changing providers is disruptive, expensive, risky, or operationally difficult. | Switching costs weaken when competitors make migration easier or the existing product stops justifying the friction. |

| Mission-critical use | A product that supports essential operations can be less sensitive to small price changes. | The advantage weakens if the product becomes less essential or customers find acceptable workarounds. |

| Scarcity or capacity constraints | Limited supply can allow higher prices when customers have few alternatives. | Temporary scarcity can disappear when supply expands or demand normalizes. |

| Regulatory, patent, or network advantages | Structural barriers can limit direct competition and support pricing discipline. | Regulation can change, patents expire, and network advantages can erode if user behavior shifts. |

| Superior customer value | Customers may accept higher prices when the product saves time, reduces risk, improves outcomes, or supports revenue. | The advantage weakens if value delivery becomes harder to prove or the customer can capture similar value elsewhere. |

How investors can observe pricing power

Pricing power is not directly visible from one line item. It usually appears through a pattern across prices, margins, volume, retention, competitive behavior, and management commentary. A single strong quarter is not enough to separate durable pricing power from timing, mix, or cost effects.

| Evidence area | What to look for | How to interpret it carefully |

|---|---|---|

| Gross margin | Margins hold or improve after price increases. | Check whether improvement comes from price realization, product mix, cost relief, or accounting effects. |

| Operating margin | Higher prices flow through after sales, support, and retention costs. | Pricing power is weaker if the company must spend heavily to defend demand. |

| Volume response | Unit volumes remain stable enough after higher prices. | Some volume decline may be acceptable, but broad demand loss can show weak customer acceptance. |

| Retention or churn | Customers stay despite higher prices. | Retention quality matters; customers may stay temporarily while searching for alternatives. |

| Discounting behavior | The company does not need larger discounts to close sales. | Published price increases are less meaningful if realized prices are offset by promotions or concessions. |

| Competitive alternatives | Competitors struggle to win share only by offering lower prices. | Pricing power is stronger when customers still prefer the product after comparing value and cost. |

| Customer value | The product remains important relative to the customer’s budget or operating needs. | A small cost item can have strong pricing power if it protects a much larger revenue or risk exposure. |

Pricing power versus economic moat

Pricing power can be evidence of a competitive advantage, but it is not the same thing as a full moat. A company may raise prices for a short period because supply is tight, demand is temporarily strong, or competitors are slow to react. That can improve reported results without proving long-term durability.

An economic moat is broader than pricing power because it also includes the durability of the advantage, the threat of substitution, the strength of the customer relationship, and the company’s ability to defend returns over time.

The stronger investor reading appears when pricing power is connected to a durable source of value and not merely to a favorable pricing moment.

What pricing power is not

- Not just high prices: a company can charge high prices and still lack pricing power if customers leave or competitors undercut the offer.

- Not just premium branding: a premium label matters only if customers keep paying for the value behind it.

- Not automatic margin quality: margins can rise because of temporary cost relief, product mix, or reduced discounting.

- Not proof of permanent advantage: pricing power can decay when substitutes improve or customer priorities change.

- Not a stock-selection rule: pricing power is one business-quality input, not a standalone investment conclusion.

Short example of pricing power

A company sells a product that represents a small share of the customer’s total cost but prevents a costly operational problem. Management raises prices moderately. If customers continue renewing, volumes remain stable, and discounts do not rise, the company may be showing pricing power because the value delivered still exceeds the added cost.

The same price increase would look weaker if customers delay purchases, competitors quickly win share, or the company protects revenue only by offering larger concessions. In that case, the price increase may have tested the market rather than revealed durable pricing power.

When pricing power can mislead

Pricing power can be overstated when investors look only at reported prices or short-term margin gains. The cleaner test is whether the company can keep customer value, competitive position, and margin quality intact after the market has had time to respond.

- Input-cost illusion: margins may improve because costs fall, not because customers accepted higher economic value.

- Temporary scarcity: supply shortages can support prices until capacity returns or demand cools.

- Customer concentration: a few large customers can pressure terms even when headline pricing looks strong.

- Competitive catch-up: competitors may need time to respond with similar quality at lower prices.

- Value decay: customers can tolerate price increases for a while before switching, negotiating, or reducing usage.

Customer dependence can change the interpretation. A company may appear to have pricing power across reported revenue while a small number of large customers still hold enough negotiating leverage to weaken future price realization.

Pricing power and the wider business model

Pricing power is more useful when it fits the company’s broader economics. A business may raise prices, but the investor still needs to understand acquisition costs, retention costs, product reinvestment, supply constraints, and whether higher prices support or damage long-term demand.

Business model analysis helps test whether pricing power is supported by the broader system that creates revenue, controls costs, serves customers, and converts profit into cash.

Management decisions also matter. A company may need to reinvest in product quality, distribution, service, or capacity to preserve the value that supports higher prices. Strong pricing power can erode if management extracts price without maintaining the reason customers pay.

That makes capital allocation decisions part of the sustainability check. Reinvestment, maintenance spending, acquisitions, and buybacks can all affect whether today’s pricing advantage remains valuable over time.

How pricing power fits investor interpretation

Pricing power is best treated as a diagnostic signal. It can support a stronger business-quality view when it appears with durable customer value, stable retention, disciplined competition, and healthy cash conversion. The reading becomes less reliable when higher prices are offset by churn, volume pressure, larger discounts, or rising costs needed to keep customers.

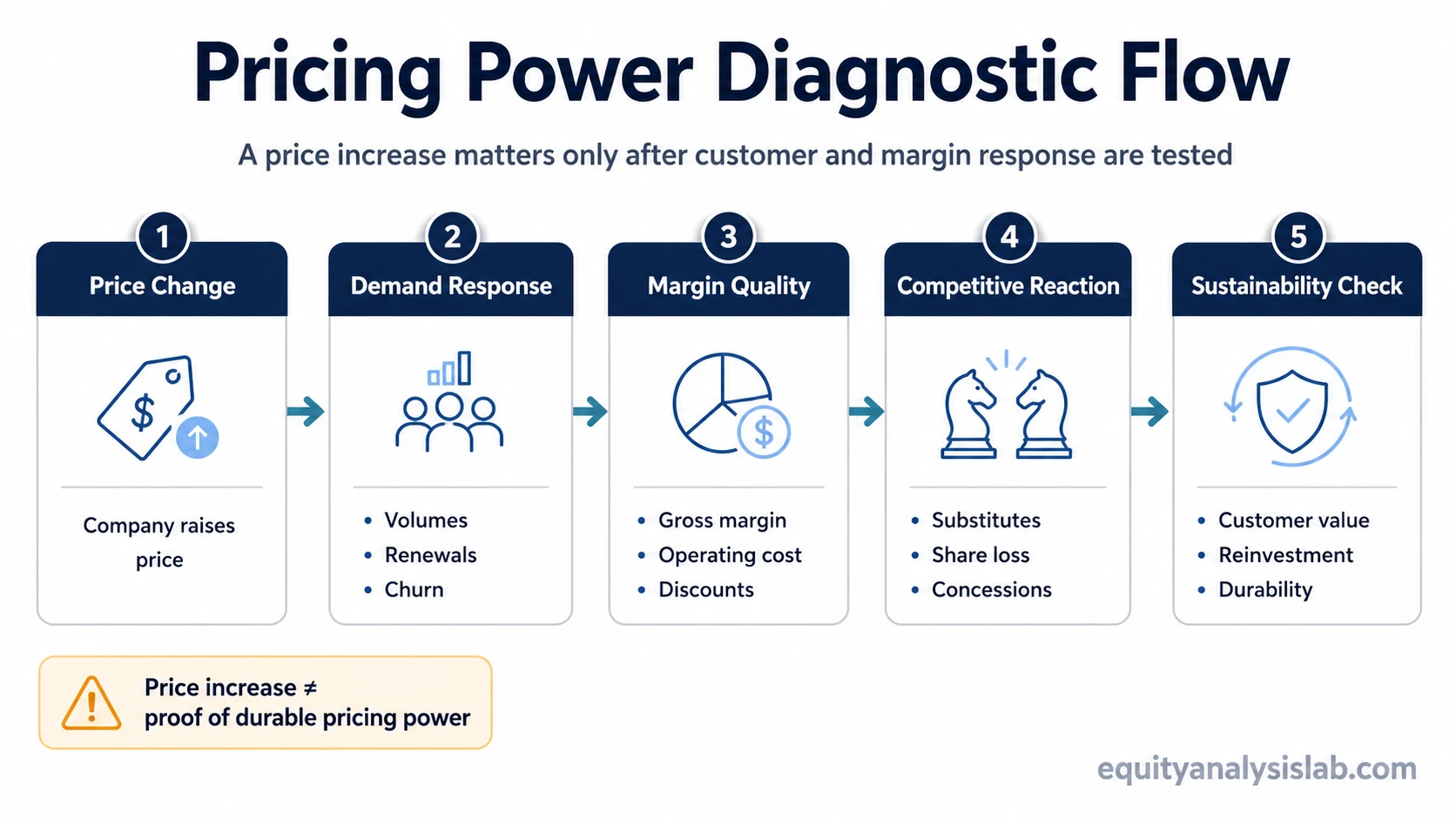

The most useful sequence is price increase, customer response, margin behavior, competitive context, and sustainability. Each step reduces the risk of mistaking a temporary pricing event for a durable business advantage.

Investor diagnostic sequence: price change → demand response → margin quality → competitive reaction → sustainability check.

Related concepts

- Economic moat: this concept tests whether pricing power reflects a durable competitive advantage rather than a temporary pricing moment.

- Business model analysis: this analysis connects pricing power to the revenue, cost, customer, and cash-conversion system behind the company.

- Customer concentration risk: this risk shows why a few large customers can weaken price realization even when headline pricing looks strong.

- Capital allocation: this area helps evaluate whether management reinvests enough to preserve the value that supports higher prices.

- Pricing power measurement: pricing power measurement should compare realized prices, margins, volume, retention, and competitive behavior rather than rely on one reported metric.

Pricing power FAQ

Is pricing power the same as raising prices?

No. Raising prices is a management action. Pricing power is shown by the customer and competitive response after the increase.

Does pricing power prove that a company has a moat?

No. Pricing power can be evidence of advantage, but a moat also requires durability, competitive defense, and a longer-term test of returns.

Why can margin improvement mislead investors?

Margins can improve because of cost relief, product mix, accounting effects, or temporary scarcity. Pricing power requires evidence that customers accept higher value over time.