An economic moat is a durable competitive advantage that helps a company defend its economics against competition. In company analysis, the moat label should be treated as a testable claim about margins, returns, cash flow durability, customer behavior, and competitive pressure, not as a shortcut for assuming a good investment.

Naming the moat source is only the starting point. The stronger test is whether the advantage appears in customer behavior, pricing resilience, margins, returns on capital, and cash flow durability after competitive pressure is considered.

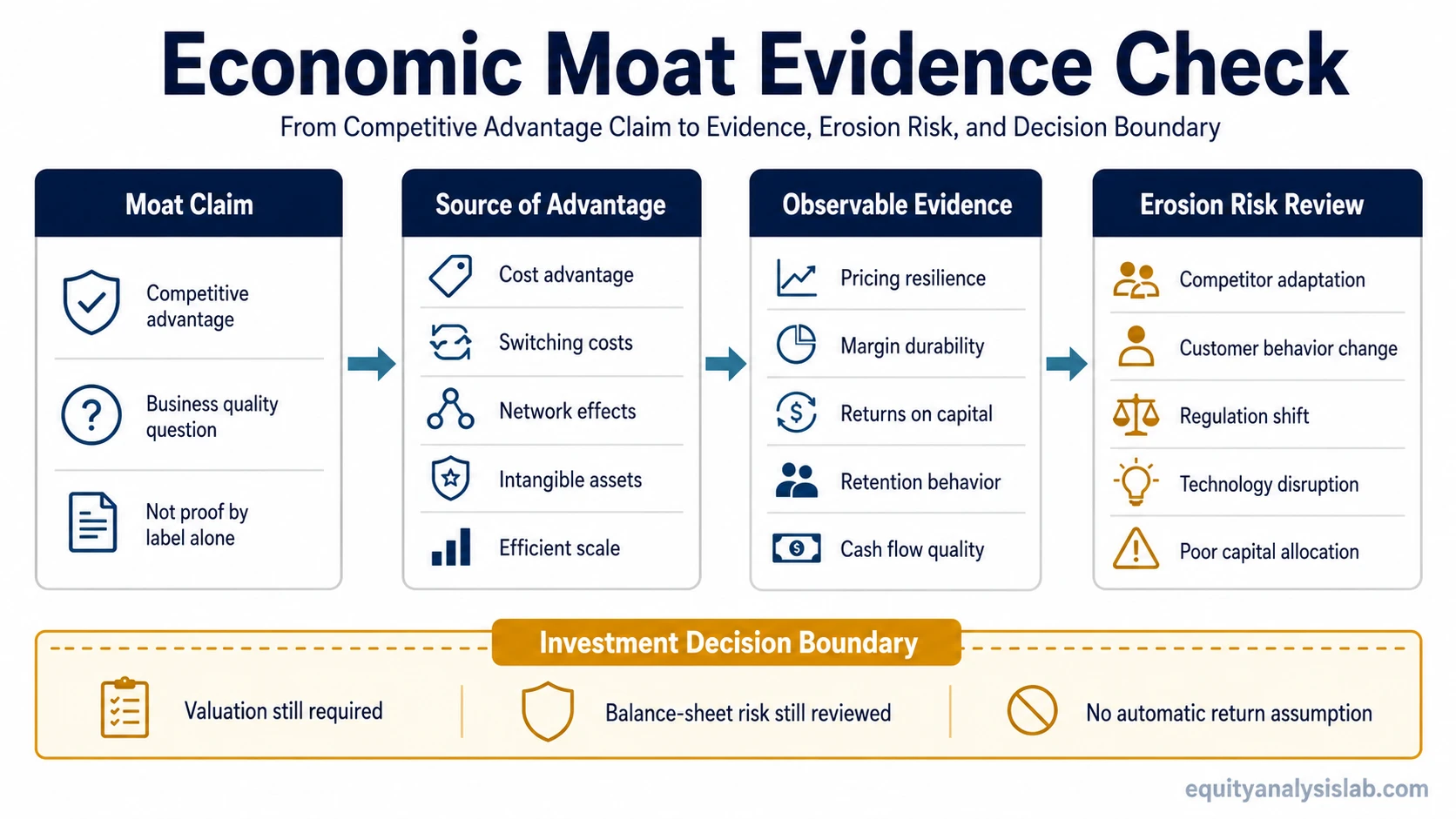

Key Points

- An economic moat describes a company’s ability to protect business economics from competition.

- A moat is not proven by brand recognition, high margins, or market share alone.

- Durable evidence usually appears in returns on capital, pricing resilience, switching behavior, cash flow quality, and margin stability.

- Moats can weaken when competitors adapt, customer behavior changes, regulation shifts, or management allocates capital poorly.

What an Economic Moat Means

Definition: An economic moat is a lasting competitive advantage that allows a company to defend its profitability, returns on capital, or cash flow against competitors for an extended period.

The term is useful because it separates ordinary business success from defended business economics. A company may grow quickly, report strong margins, or dominate a market for a period without having a durable moat. A real moat requires evidence that competitors cannot easily copy, underprice, displace, or neutralize the company’s advantage.

That evidence usually starts with business model analysis. The operating model has to show why customers buy, why competitors struggle to match the offer, and why the company can keep earning attractive economics after normal competitive pressure appears.

How an Economic Moat Defends Company Economics

An economic moat protects the spread between what a company earns and what competition would normally pressure it to earn. Without a moat, attractive profits invite new supply, price competition, substitute products, or customer churn. With a moat, those pressures may still exist, but they are harder to convert into economic damage.

The defense can appear in several ways. A company may retain customers because switching is costly or disruptive. It may produce at a lower cost than rivals. It may benefit from network effects, where the service becomes more useful as more participants join. It may own intangible assets such as trusted brands, patents, licenses, data, distribution relationships, or regulatory positions that competitors cannot easily replicate.

Moat analysis also needs a reinvestment lens. Even a strong competitive position can fade if capital-allocation decisions weaken the core advantage, fund low-return expansion, or ignore new threats. A moat is therefore not only about the source of advantage; it is also about whether management preserves and compounds that advantage without diluting the business quality.

Common Sources of Economic Moats

Most moat sources fall into a small group of mechanisms. The labels are useful, but they should not replace evidence. A brand moat, for example, is not simply a recognizable name. It has to show up in customer preference, price resilience, repeat demand, or distribution strength.

| Moat source | What it can defend | What to check |

|---|---|---|

| Cost advantage | Margins and pricing flexibility | Unit costs, scale economics, supplier terms, logistics, and cost structure versus competitors |

| Switching costs | Customer retention and recurring revenue | Contract depth, workflow dependency, migration friction, renewal behavior, and customer concentration |

| Network effects | Platform value and user retention | Whether the product becomes more useful as more customers, suppliers, users, or data points join |

| Intangible assets | Trust, access, or legal protection | Brand behavior, patents, licenses, regulatory position, proprietary data, or distribution control |

| Efficient scale | Market structure and entry barriers | Market size, capacity needs, fixed costs, local density, and whether new entrants have enough incentive to compete |

Moat Evidence and Erosion Check

Moat evidence should be reviewed as a pattern, not as a single metric. High margins may reflect a moat, but they can also reflect a temporary cycle, accounting mix, supply shortage, or underinvestment by competitors. A stronger review looks for several forms of evidence that point in the same direction.

| Evidence input | What it may suggest | What can weaken the interpretation |

|---|---|---|

| Sustained high returns on capital | The company may be earning above-normal returns that competition has not competed away. | Returns may be inflated by a favorable cycle, asset-light accounting, underinvestment, or temporary supply constraints. |

| Margin durability | The business may have pricing resilience, cost control, or structural efficiency. | Margins may fall if input costs rise, competitors discount, regulation changes, or customer demand weakens. |

| Cash flow consistency | The moat may translate into real economic output rather than only accounting profit. | Cash flow may be distorted by working-capital timing, capitalized costs, or temporary collection patterns. |

| Customer retention | Customers may face switching costs, workflow dependency, or strong preference for the product. | Retention can weaken when substitutes improve, integration costs fall, or contract renewals expose price sensitivity. |

| Pricing resilience | The company may be able to raise or hold price without severe volume loss. | Price resilience may disappear if customers trade down, competitors bundle, or the product becomes easier to replace. |

| Reinvestment quality | The company may be able to deploy capital into areas that strengthen the advantage. | Poor acquisitions, unfocused expansion, or low-return projects can weaken the moat despite strong historical economics. |

Economic Moat vs Business Quality

An economic moat is part of business quality, but it is not the whole analysis. Business quality also includes management behavior, balance-sheet resilience, reinvestment runway, cash conversion, earnings durability, and the risks that can interrupt those strengths.

One common mistake is to treat a moat as a permanent label. A company can have a strong competitive position in one period and a weaker one later if customer needs change, regulation removes an advantage, technology lowers barriers, or competitors find a cheaper distribution model.

Another mistake is to confuse one evidence channel with the entire moat. The ability to maintain prices without severe demand damage can support a moat claim, but that condition should still be tested against costs, retention, competition, and customer behavior. That is where the ability to hold price without losing demand becomes one evidence input, not the full conclusion.

When an Economic Moat Can Weaken

Limitation: A moat can erode even when the historical numbers still look strong. Competitive advantages weaken when the conditions that created them stop protecting the company’s economics.

Moat erosion can come from technology that lowers switching costs, regulation that removes an exclusive advantage, new competitors with better cost structures, customer behavior that shifts away from the product, or management choices that dilute the company’s strongest economics.

A simple scenario illustrates the risk. A software company may appear protected because customers have built workflows around its product. If a cheaper replacement becomes easier to integrate and customers begin testing it at contract renewal, the old switching-cost argument becomes less reliable. The same reported retention rate may deserve a more cautious reading if customer dependency is falling.

Moat analysis should also check fragility from customer dependency. A business may look protected when one major customer is stable, but the advantage can be weaker than it appears if the economics depend on a small number of buyers. That risk belongs in a separate fragility from customer dependency review.

Wide Moat vs Narrow Moat

A wide moat usually means the competitive advantage appears strong, durable, and difficult to attack across a long period. A narrow moat usually means the advantage exists, but the protection is more limited, easier to pressure, or dependent on a smaller set of conditions.

The distinction is useful, but it should not become a false precision exercise. The more important question is what evidence supports the classification. If returns, margins, retention, pricing resilience, and cash conversion all point in the same direction, the moat claim has more support. If only one indicator is strong, the conclusion should remain more cautious.

Related Business Quality Concepts

Economic moat analysis sits inside a wider business-quality review. It identifies whether a company has a defensible advantage, but adjacent concepts explain different parts of the same evidence set.

| Concept | How it relates to economic moat |

|---|---|

| Business model analysis | Shows how the company creates value, earns revenue, controls costs, and turns its operating structure into durable economics. |

| Pricing power | Tests whether customers accept price changes without enough demand loss to damage the economics. |

| Capital allocation | Shows whether management strengthens the moat through reinvestment, acquisitions, buybacks, debt use, or strategic restraint. |

| Customer concentration risk | Tests whether the apparent moat depends too heavily on a small number of customers or contracts. |

FAQ

What is an economic moat?

An economic moat is a durable competitive advantage that helps a company defend its profitability, returns on capital, or cash flow against competition.

What are common economic moats?

Common economic moats include cost advantages, switching costs, network effects, intangible assets, efficient scale, and other advantages that competitors cannot easily copy or neutralize.

Does an economic moat make a stock a good investment?

No. A moat can support business quality, but it does not replace valuation, risk review, balance-sheet analysis, or evidence about whether the advantage is still durable.

Can an economic moat disappear?

Yes. Moats can weaken when technology changes, competitors adapt, regulation shifts, customers switch behavior, or management decisions damage the company’s advantage.