Capital allocation is not just a list of spending choices. It is the management decision process that determines whether company resources are reinvested, returned to shareholders, used to reduce debt, used for acquisitions, or retained for future flexibility.

Definition: Capital allocation is the way management chooses where company capital goes and whether those choices improve durable value per share after cost, risk, and opportunity cost.

For investors, capital allocation connects operating performance to management judgment. A company can produce strong cash flow and still destroy value if capital is deployed into low-return projects, overpriced acquisitions, poorly timed buybacks, or dividends that weaken reinvestment capacity.

The useful question is not only where money went. The useful question is whether each use of capital had a credible reason, a reasonable expected return, and a better risk-adjusted purpose than the alternatives available at the time.

Key Points

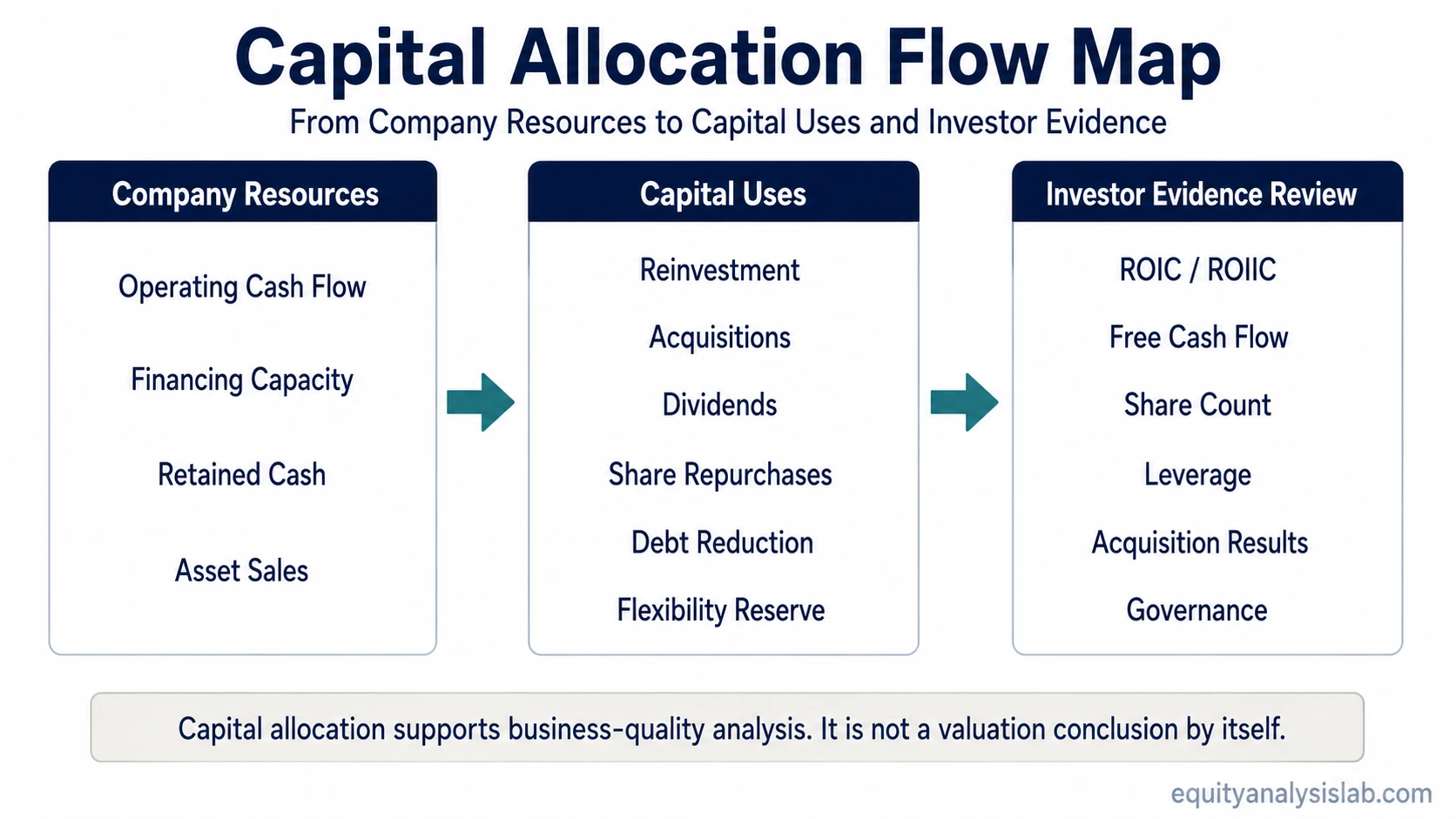

- Capital allocation shows how management uses cash flow, financing capacity, retained cash, debt repayment, acquisitions, dividends, buybacks, and reinvestment.

- Good analysis compares each capital decision with opportunity cost, not with the size of the spending decision alone.

- ROIC, ROIIC, free cash flow, share count, leverage, and reinvestment rate help investors judge whether capital is being used productively.

- Capital allocation can strengthen value per share, but it does not by itself prove that a stock is attractive.

What Capital Allocation Means in Company Analysis

In company analysis, capital allocation sits inside management quality and business quality. It asks how resources move from the operating business into future growth, balance-sheet strength, shareholder returns, or strategic flexibility.

A strong operating business gives management more choices. Those choices still need discipline. Cash can fund reinvestment, but reinvestment only helps if the projects earn attractive returns. Debt reduction can lower risk, but it may be less useful if the balance sheet is already conservative and high-return internal projects are available. Buybacks can increase value per share, but only when the price paid is sensible relative to value.

Capital allocation should be judged inside the company’s business model analysis, because the same action can mean different things in different businesses. A capital-light software company, a regulated utility, and a cyclical industrial company may all retain cash for valid reasons, but the evidence needed to justify that decision will differ.

Sources and Uses of Capital

Capital allocation begins with the resources available to management. The main source is usually cash generated by the business, but companies can also raise capital through debt, equity issuance, asset sales, or working-capital release.

Those resources are then assigned to competing uses. Each use has a different effect on growth, risk, flexibility, and value per share.

| Capital use | What it can do | Investor question |

|---|---|---|

| Reinvestment | Funds organic growth, capacity, product development, technology, or distribution. | Can incremental capital earn returns above the company’s opportunity cost? |

| Acquisitions | Expands the business through purchased assets, customers, capabilities, or markets. | Was the price paid reasonable after integration risk and expected returns? |

| Dividends | Returns cash directly to shareholders. | Does the payout fit the company’s reinvestment needs and balance-sheet position? |

| Share buybacks | Reduces share count when shares are repurchased and retired. | Were shares repurchased at a price that improved value per remaining share? |

| Debt repayment | Reduces financial risk and interest burden. | Does deleveraging improve resilience, or does it crowd out better capital uses? |

| Retained cash | Preserves flexibility for resilience, future investment, or disciplined timing. | Is cash being held for a credible purpose, or is it lowering capital efficiency? |

Capital has an opportunity cost. A dollar used for one purpose cannot be used for another. That is why the analysis should compare management’s chosen use of capital with the alternatives, not just with the stated intention behind the decision.

How Investors Evaluate Capital Allocation Quality

Capital allocation quality depends on the relationship between returns, risk, durability, and per-share value. A decision may look attractive in accounting terms but still fail if it requires too much capital, raises leverage too far, or produces returns below a reasonable cost of capital.

Return on invested capital helps show how efficiently the company earns operating profit relative to the capital invested in the business. Incremental return on invested capital is often more useful for capital allocation because it focuses on what new capital is earning, not only what the existing asset base earned in the past.

Free cash flow gives another view. It shows whether reported earnings translate into cash that can actually be allocated. A company with high accounting profit but weak cash conversion may have less real capital flexibility than headline numbers suggest.

Share count matters because capital allocation is ultimately judged by what happens to value per share. A buyback funded by excess cash can help if shares are bought below a reasonable estimate of value. A buyback funded by excessive debt or executed at an inflated price can weaken the same per-share outcome it was supposed to improve.

Reinvestment is most powerful when it reinforces a durable advantage rather than merely increasing size. Capital spent to deepen customer switching costs, improve distribution, or protect a profitable niche may support a stronger moat, while capital spent only to chase revenue can dilute returns if the underlying advantage is weak.

Capital Allocation Evidence Map

Investors do not have to rely only on management commentary. Capital allocation leaves traces across financial statements, footnotes, investor presentations, and long-term operating results.

| Evidence area | What to observe | What it can reveal |

|---|---|---|

| Cash flow statement | Capital expenditures, acquisitions, dividends, buybacks, debt repayment, and cash retained. | Where cash actually went, not only what management emphasized. |

| ROIC and incremental returns | Returns on the existing capital base and returns on newly deployed capital. | Whether reinvestment is creating value or absorbing capital at weak returns. |

| Share count | Diluted shares outstanding over time, net of buybacks and equity issuance. | Whether repurchases are improving ownership per share or only offsetting dilution. |

| Debt and interest expense | Leverage, maturity schedule, interest coverage, and refinancing needs. | Whether capital returns are being funded in a way that increases financial fragility. |

| Acquisition notes | Purchase price, goodwill, integration costs, impairments, and acquired revenue or earnings. | Whether acquisitions are improving economics or masking organic weakness. |

| Segment performance | Growth, margins, capital intensity, and returns by segment where disclosed. | Whether capital is moving toward the most productive parts of the business. |

| Revenue concentration | Dependence on major customers, contracts, channels, or end markets. | Whether capital deployment is exposed to concentrated revenue risk. |

Revenue durability can change the interpretation of capital deployment. If a business depends heavily on a small customer base, a major investment program may carry more risk than it would in a company with more diversified demand and lower customer concentration exposure.

Common Capital Allocation Mistakes

Mistake: Treating every use of cash as value creation.

Cash only creates value when it is used or retained for a reason that improves the company’s risk-adjusted future. Idle cash can be useful when it protects resilience or preserves optionality, but it can also lower capital efficiency if management has no credible plan.

Mistake: Calling buybacks good without asking about price.

A repurchase can improve value per share when shares are bought below a reasonable estimate of value. The same buyback can destroy value if management pays too much, uses too much debt, or only offsets stock-based compensation.

Mistake: Rewarding acquisitions before checking returns.

Acquisitions can add capabilities or scale, but the price paid, integration risk, goodwill, and later impairments matter. A larger company is not automatically a better company if the acquired returns are weak.

Mistake: Treating dividends as automatically disciplined.

A dividend can signal maturity and cash generation, but it can also constrain reinvestment if the business still has attractive internal opportunities. The payout should fit the company’s return profile, capital intensity, and balance-sheet risk.

A compact way to test these decisions is to ask whether the capital action improves durable value per share after cost, risk, and opportunity cost. If the answer depends only on a management slogan, the evidence is not strong enough.

Governance, Incentives, and Decision Quality

Capital allocation is partly a financial question and partly a governance question. Boards and executives decide which metrics matter, how much risk is acceptable, and whether incentives reward durable value or short-term optics.

Useful governance evidence includes compensation metrics, acquisition approval discipline, leverage targets, dividend policy, buyback authorization language, and management’s explanation of reinvestment priorities. The most useful evidence usually appears across several reporting periods, not in one polished presentation.

Incentives can distort allocation. If executive pay rewards revenue growth without enough attention to returns on capital, management may prefer expansion even when incremental returns are poor. If incentives overemphasize short-term earnings per share, management may favor buybacks even when reinvestment or balance-sheet repair would be more durable.

Pricing strength also affects the decision set. A company with the ability to raise price without eroding demand may have more room to reinvest through cost pressure, while a business with weak price control may need to protect liquidity before expanding.

Limitations of Capital Allocation Analysis

Limitation: Capital allocation does not replace valuation. A well-managed company can still be a poor investment if the price already assumes too much future success.

Limitation: ROIC does not explain everything by itself. High returns can fade, low returns can improve, and accounting measures can be distorted by asset-light models, acquisitions, write-downs, or underinvestment.

Limitation: Management intent is not the same as evidence. A clear capital allocation framework is useful, but investors still need to compare it with actual cash flow, reinvestment results, leverage, share count, and long-term returns on capital.

Capital allocation is best treated as one part of business-quality analysis. It helps explain whether management is compounding resources wisely, but it does not create an automatic investment conclusion.

Related Business-Quality Concepts

Capital allocation becomes clearer when it is separated from neighboring business-quality ideas. The operating model explains how the company earns money, while capital allocation explains what management does with the resources that model produces.

Reinvestment quality is closely tied to durable competitive advantage. A company that can reinvest into customer relationships, distribution, product depth, or cost advantages may strengthen its competitive position, but only if those investments earn acceptable returns.

Capital deployment also depends on revenue resilience. A business with unstable or concentrated demand may need a more conservative balance-sheet and reinvestment policy than a company with broader, repeatable customer economics.

Margin durability shapes the reinvestment runway. When a company can defend pricing and margins, management may have more flexibility to fund growth without weakening cash flow or balance-sheet strength.

FAQ

What is capital allocation?

Capital allocation is management’s process for deciding how company resources are reinvested, returned to shareholders, used for acquisitions, used to reduce debt, or retained for future flexibility.

Why does capital allocation matter to investors?

It matters because management can either build or weaken value per share depending on how cash flow, debt capacity, reinvestment, buybacks, dividends, acquisitions, and retained cash are used.

How is capital allocation judged?

Investors usually compare capital decisions with free cash flow, ROIC, incremental returns, cost of capital, leverage, share count, acquisition results, and the opportunity cost of alternative uses.

Are buybacks always good capital allocation?

No. Buybacks depend on price, funding source, balance-sheet risk, and whether repurchases improve value per remaining share after considering other available uses of capital.

Does good capital allocation make a stock attractive?

No. Capital allocation can support business quality, but investors still need valuation, risk, durability, and portfolio context before forming an investment view.