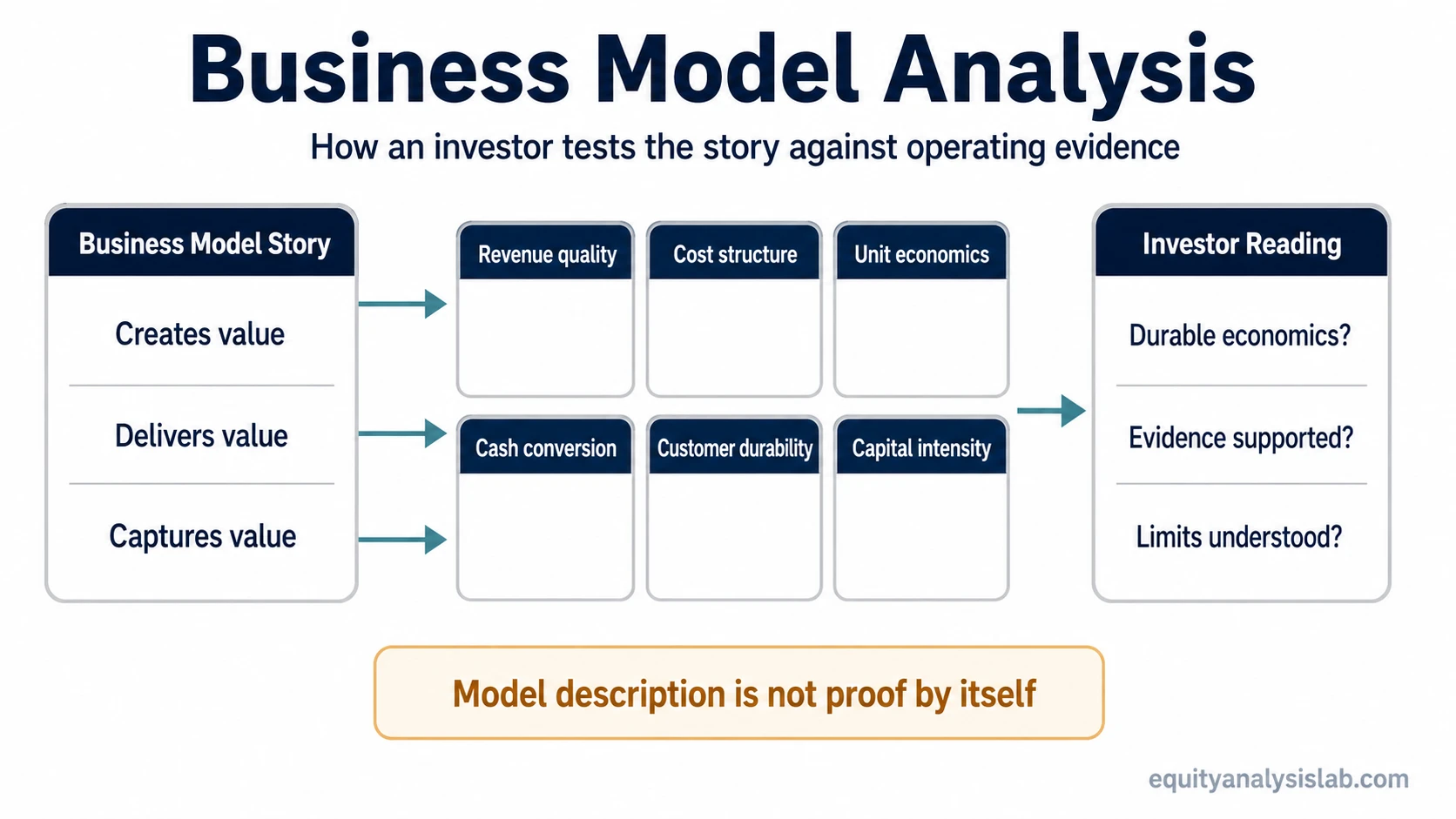

Business model analysis examines how a company creates, delivers, and captures value. For investors, the concept is useful only when the business model description is tested against operating and financial evidence.

A company can describe an attractive model without having a strong business. Revenue mix, cost structure, margins, unit economics, cash conversion, customer durability, capital intensity, and competitive context determine whether the model is producing durable economics or only a convincing narrative.

Definition: Business model analysis is the process of evaluating how a company turns its products, customers, operations, and resources into revenue, profit, and cash flow. It does not prove business quality or predict investment returns by itself.

- Business model analysis starts with how a company creates, delivers, and captures value.

- Investor analysis must connect the model to revenue quality, margins, cash conversion, and capital intensity.

- Growth alone is not enough if the model depends on weak economics, rising costs, or fragile customers.

- A business model can support business-quality review, but it does not automatically prove moat durability.

What Business Model Analysis Means for Investors

For investors, the task is not only to describe what a company sells. The useful question is whether the company’s way of earning money can support durable revenue, acceptable margins, cash generation, and reinvestment over time.

A basic business model description may say that a company sells subscriptions, products, advertising, services, licenses, or marketplace access. An investor reading goes further. It asks whether those revenues are recurring or transactional, whether customers stay or churn, whether growth requires heavy spending, and whether the company can convert reported revenue into cash.

The analysis also separates business appeal from business quality. A company may serve a large market, solve a real customer problem, and grow quickly, while still having weak economics if acquisition costs are high, gross margins are pressured, or working capital absorbs cash.

What Evidence Supports a Business Model Reading

A strong business model reading is evidence-based. The model should be tested through revenue behavior, cost structure, customer durability, cash conversion, and the way management funds growth.

| Evidence area | Investor question | What supports the reading | What weakens the reading |

|---|---|---|---|

| Revenue sources | Where does the company actually make money? | Revenue is diversified, understandable, repeatable, and tied to clear customer demand. | Growth depends on one product, one channel, one customer group, or unstable transaction volume. |

| Cost structure | Does growth improve or strain economics? | Gross margins, operating leverage, and fulfillment costs remain consistent as the business scales. | Revenue growth requires rising incentives, support costs, logistics expense, or sales spending. |

| Value proposition | Why do customers pay? | The product solves a recurring or high-value problem and is difficult to replace casually. | The story depends more on market size or branding than visible customer retention and willingness to pay. |

| Customers and channels | How durable is demand? | Customer retention, repeat usage, and channel economics support the growth story. | Customer concentration risk, channel dependency, or high churn makes revenue less durable. |

| Unit economics | Does each customer, order, or account create attractive economics? | Customer lifetime value, contribution margin, and acquisition cost relationships improve or remain stable. | The company must spend more to acquire lower-quality growth, or payback periods stretch as it scales. |

| Cash conversion | Does accounting growth become usable cash? | Operating cash flow and free cash flow support reported revenue and earnings over time. | Working capital, deferred costs, receivables, or capital expenditure consume cash faster than growth creates it. |

| Capital intensity | How much investment is required to keep the model working? | The company can grow without constantly requiring heavy new assets, financing, or dilution. | The model needs repeated external funding, large infrastructure spending, or constant reinvestment just to maintain position. |

When Business Model Analysis Can Mislead Investors

Business model analysis becomes misleading when the description sounds stronger than the evidence. A scalable model, large addressable market, recurring revenue label, or platform narrative can hide weak economics if the numbers do not support the story.

Narrative risk: A company may explain its model clearly while still failing to show pricing power, retention, cash conversion, or margin durability.

TAM overstatement: A large market does not prove that the company can capture profitable demand. Market size matters less if the business must discount heavily or spend aggressively to grow.

Revenue growth misuse: Fast revenue growth can look attractive while the underlying model weakens. The reading changes if growth comes with lower gross margins, rising acquisition costs, slower collections, or heavier working-capital needs.

Capital intensity: Some models require constant reinvestment in inventory, infrastructure, content, distribution, or physical assets. That can limit free cash flow even when revenue is expanding.

Durability confusion: A good business model does not automatically create an economic moat. Durability depends on competitive advantage, switching costs, scale benefits, brand strength, network effects, or other defensible features that must be analyzed separately.

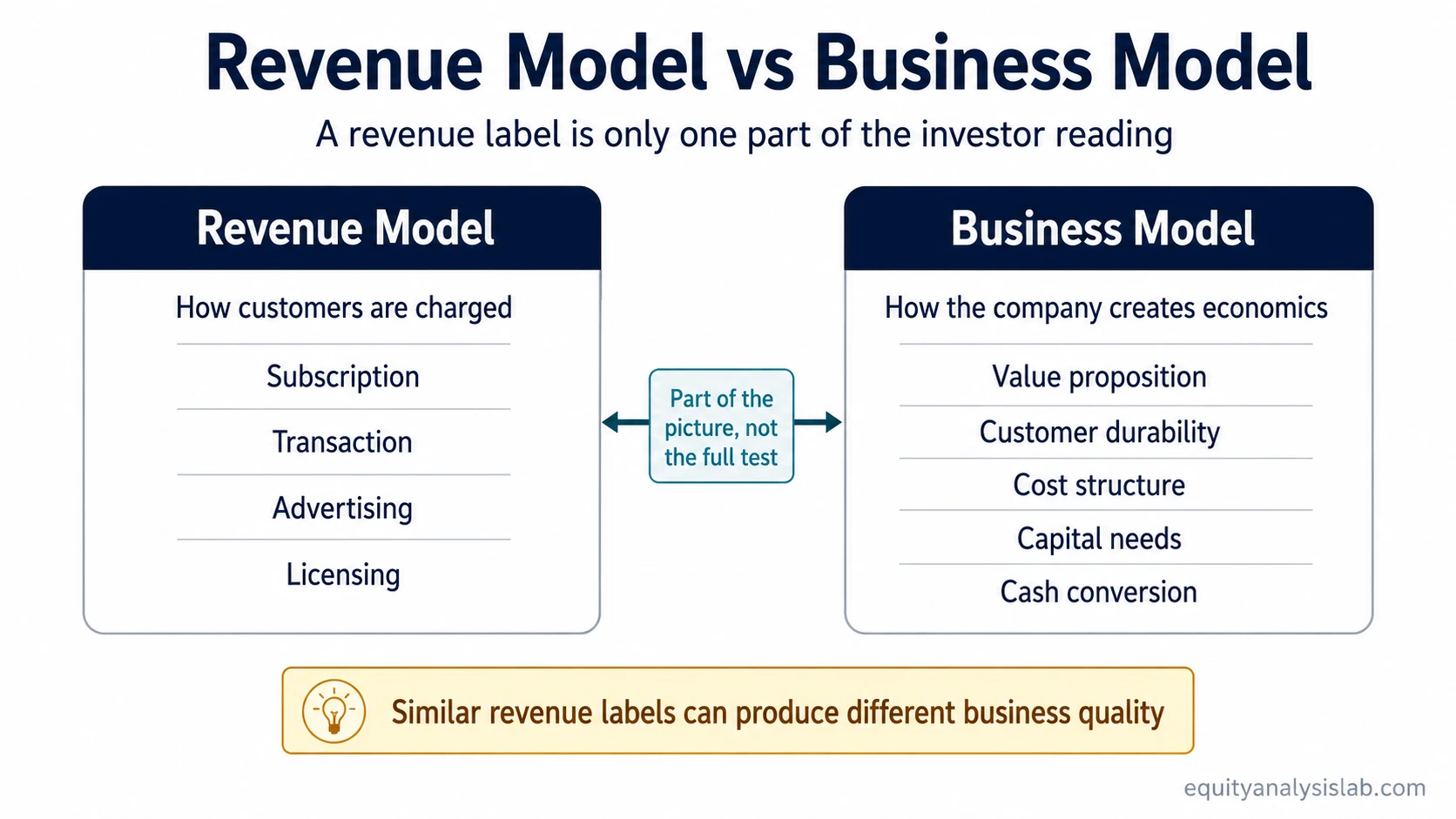

Business Model Analysis vs Revenue Model

A revenue model explains how a company charges customers. A business model explains the broader system that makes those revenues possible, including customers, value proposition, cost structure, operations, capital needs, and cash conversion.

For example, two companies may both have subscription revenue. One may have low churn, high gross margins, and efficient customer acquisition. Another may need heavy discounts, high sales spending, and constant product investment to keep customers. The revenue model looks similar, but the business model quality can be very different.

This distinction matters because revenue labels can create false comfort. Subscription, marketplace, advertising, licensing, and transaction models all need evidence. The label is only the starting point; the economics decide whether the model is attractive for investor analysis.

Practical Scenario

A company describes itself as a scalable recurring-revenue business. Revenue is growing, the market opportunity sounds large, and management presents the model as asset-light.

The initial read is tempting because recurring revenue can suggest predictability. The read is incomplete if customer acquisition costs are rising, gross margin is declining, cash conversion remains weak, and a small group of customers drives a large share of revenue.

The stronger case would show stable retention, improving acquisition efficiency, healthy contribution margins, and operating cash flow that supports reported growth. The weaker case would show that revenue expansion depends on heavier spending, customer dependency, or capital needs that dilute the apparent quality of the model.

The useful investor question is whether the model is producing durable economics, not whether the narrative sounds attractive.

How Business Model Analysis Connects to Capital Decisions

Even a strong model still depends on management decisions. A company that generates cash must decide whether to reinvest, acquire, reduce debt, repurchase shares, or distribute dividends. That is why this analysis should eventually connect to capital allocation.

The business model shows how value may be created. Capital decisions show whether management can preserve or compound that value. A durable model can be weakened by poor reinvestment, excessive dilution, overpriced acquisitions, or debt choices that reduce flexibility.

Related Business Quality Concepts

Moat durability: Use moat analysis to test whether a business model has durable competitive protection rather than only attractive economics today.

Customer dependency: Use customer dependency analysis when a company’s revenue depends heavily on a small number of customers, contracts, or channels.

Capital decisions: Use capital allocation analysis to judge whether management turns the model’s cash flows into long-term value or weakens them through poor reinvestment choices.

Business Model Analysis FAQ

Is business model analysis the same as business quality analysis?

No. Business model analysis is one part of business quality analysis. It studies how the company creates and captures value, while business quality also includes durability, competitive position, management decisions, financial strength, and risk.

Can a company have a good business model but still be a weak investment?

Yes. A company can have an attractive model but still face valuation risk, weak cash conversion, poor capital allocation, competitive pressure, dilution, or execution problems. The model is evidence for analysis, not a complete investment decision.

Does revenue growth prove that a business model is working?

No. Revenue growth needs to be tested against margins, customer retention, acquisition costs, working capital, capital intensity, and cash flow. Growth that requires deteriorating economics may weaken the business model reading.