Annual recurring revenue is the annualized value of active recurring subscription or contract revenue. ARR is a diagnostic metric, not proof that a SaaS company has strong retention, high margins, pricing power, or attractive valuation.

Annual recurring revenue, or ARR, measures the recurring revenue base of a subscription business over a one-year period. It usually excludes one-time setup fees, non-recurring services, temporary usage spikes, and revenue that is not tied to an active recurring contract or subscription.

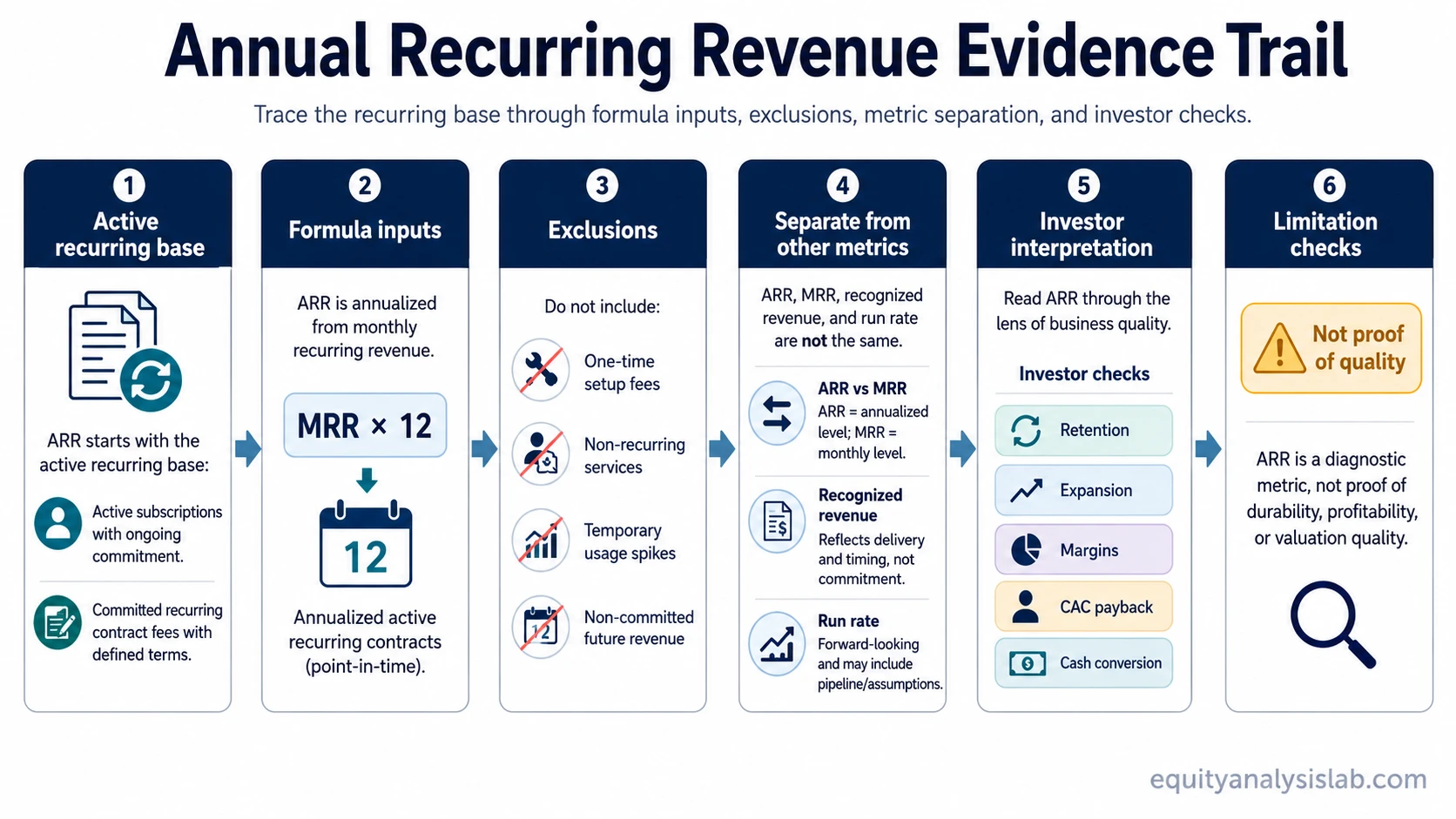

Key points about annual recurring revenue

- ARR annualizes recurring subscription or contract revenue.

- ARR is not the same as recognized revenue under accounting rules.

- ARR can grow even when churn, discounts, weak cash conversion, or margin pressure reduce business quality.

- Investors should read ARR alongside retention, expansion, gross margin, acquisition payback, and cash flow.

What annual recurring revenue means

Annual recurring revenue represents the recurring revenue base that is active at a point in time or over a defined measurement period. For a SaaS company, that base usually comes from subscriptions, recurring licenses, committed contract fees, or other repeatable customer payments.

The important boundary is recurrence. A customer payment belongs in ARR only when it reflects an ongoing revenue relationship. A one-time implementation fee may increase reported revenue, but it does not usually increase ARR because it does not repeat each year by itself.

ARR helps investors separate the recurring part of a business from revenue that may be temporary, transactional, or service-heavy. That separation matters because recurring revenue can make future revenue easier to analyze, but it does not automatically make the business durable or profitable.

How annual recurring revenue is calculated

The basic ARR formula annualizes recurring revenue. The simplest version is:

ARR = monthly recurring revenue × 12

For contract-based businesses, ARR can also be built from the active recurring contract base:

ARR = annualized value of active recurring subscriptions and committed recurring contract fees

| Formula part | What it means | Investor interpretation |

|---|---|---|

| Active recurring subscriptions | Current customers paying for repeat access to a product or service | Shows the current recurring base, but not whether the customer base is improving in quality |

| Committed recurring contract fees | Contracted payments expected to recur over the subscription term | Useful for visibility, but still needs comparison with billing, revenue recognition, and renewal behavior |

| Expansion revenue | Recurring upgrades, seat additions, or plan expansions from existing customers | Can improve ARR quality when it comes from healthy customer usage rather than temporary discounting or forced packaging |

| Churned or downgraded revenue | Recurring revenue lost when customers cancel, reduce seats, or move to lower plans | Must be deducted or analyzed separately because new ARR can hide weakening retention |

What counts and what does not count in ARR

ARR quality depends on what the company includes. The same headline number can mean different things if one company includes only committed recurring subscriptions while another includes more variable or service-heavy revenue.

| Revenue item | Usually included in ARR? | Why the boundary matters |

|---|---|---|

| Active subscription fees | Yes | They represent recurring customer payments tied to the product or service. |

| Recurring contract fees | Yes | They reflect committed repeat revenue if the contract is active and recurring. |

| Recurring upgrades or seat additions | Often yes | They can increase ARR if they are recurring and not one-time usage or temporary service work. |

| One-time setup or implementation fees | Usually no | They may increase reported revenue, but they do not usually repeat each year. |

| Professional services revenue | Usually no | Service-heavy revenue may not have the same recurrence, margin profile, or scalability as subscription revenue. |

| Temporary usage spikes | Usually no | Short-term usage can inflate a period without proving that the recurring base has permanently expanded. |

| Churned contracts | No | Revenue from customers who have cancelled should not remain in the active recurring base. |

Simple ARR example

If a SaaS company has $500,000 of monthly recurring revenue from active subscriptions, the simple annualized ARR calculation is:

$500,000 × 12 = $6,000,000 ARR

That number describes the annualized recurring base, not the full income statement. If the company also earns one-time implementation fees, custom service revenue, or temporary usage revenue, those items may affect reported revenue without changing ARR in the same way.

ARR vs MRR vs recognized revenue

ARR, MRR, and recognized revenue answer different questions. Treating them as interchangeable can lead to weak analysis because each metric uses a different time frame and measurement basis.

| Metric | What it measures | Common investor mistake |

|---|---|---|

| ARR | Annualized recurring subscription or contract revenue | Assuming it is the same as accounting revenue or future cash collection |

| Monthly recurring revenue | Recurring revenue measured monthly | Annualizing a volatile monthly base without checking churn, discounts, or seasonality |

| Recognized revenue | Revenue recorded under accounting rules during a reporting period | Confusing accounting recognition with contracted recurring revenue visibility |

| Billings or cash collections | Amounts invoiced or collected from customers | Assuming cash timing and revenue recognition move together |

ARR is useful because it highlights the recurring base, but recognized revenue and cash flow still matter. A company can show strong ARR growth while cash conversion is weak if commissions, discounts, deferred revenue timing, or implementation costs absorb the benefit.

How investors should interpret ARR

ARR is most useful when it becomes the starting point for better questions. A high ARR number may show scale, but the quality of that scale depends on customer behavior, pricing, margins, and cash economics.

| Investor check | Question to ask | Why it matters |

|---|---|---|

| Retention | Are customers staying? | Gross revenue retention helps show whether the existing base is leaking before expansion is added. |

| Expansion | Are existing customers spending more? | Net revenue retention helps separate customer expansion from pure new-logo growth. |

| Acquisition efficiency | How expensive is new ARR? | CAC payback period helps connect recurring revenue growth with the cost of acquiring it. |

| Profitability balance | Does growth come with improving economics? | The Rule of 40 can help frame growth and profitability together, but it should not replace margin, cash flow, and retention analysis. |

| Cash conversion | Does ARR turn into cash? | Recurring revenue visibility is less valuable if working capital, discounts, commissions, or implementation costs absorb the cash benefit. |

When ARR can mislead

ARR can overstate business quality when it is read without churn, margin, cash flow, and revenue recognition context. A larger recurring revenue base is helpful information, but it is not a complete quality signal.

- New ARR can hide churn. A company may add enough new customers to grow ARR while losing older customers at an unhealthy rate.

- Expansion can mask weakness in the core base. Upsells can lift ARR even if many customers are downgrading or using the product less.

- Booked contract value is not the same as recognized revenue. A contract may increase visibility, but revenue recognition and billing timing can differ.

- ARR can grow while margins weaken. Heavy discounts, high support costs, implementation work, or high sales commissions can reduce the economic value of ARR growth.

- Definitions can differ by company. ARR comparisons are stronger when the included and excluded revenue items are consistent.

- ARR does not prove product quality or valuation upside. The number needs support from retention, expansion, unit economics, and cash conversion.

Related SaaS metrics to check next

ARR becomes more useful when it is compared with the metrics that explain customer behavior and business economics. MRR clarifies the monthly base. GRR and NRR separate customer retention from expansion. CAC payback connects growth with acquisition cost. The Rule of 40 frames growth and profitability together without treating ARR as a standalone quality score.

| Metric | Use it to understand | Best next question |

|---|---|---|

| Monthly recurring revenue | The recurring base measured monthly | Is the monthly base stable enough to annualize? |

| ARR vs MRR | The difference between annual and monthly recurring revenue views | Which time scale fits the analysis? |

| Gross revenue retention | Revenue kept from existing customers before expansion | How much of the base survives without upsells? |

| Net revenue retention | Existing-customer revenue after churn, downgrades, and expansion | Are retained customers expanding enough to offset losses? |

| CAC payback period | How long acquisition spend takes to pay back | Is new ARR being bought efficiently? |

| Rule of 40 | Growth and profitability balance | Does recurring revenue growth come with acceptable economics? |

FAQ

Is ARR the same as revenue?

No. ARR is an annualized measure of recurring subscription or contract revenue. Revenue is the amount recognized during an accounting period, and it can include recurring revenue, services revenue, one-time fees, and other items depending on the business.

Is ARR the same as MRR?

No. MRR measures recurring revenue on a monthly basis, while ARR annualizes recurring revenue over a year. A simple conversion is ARR equals MRR multiplied by 12, but contract timing, churn, expansion, and billing terms can make the interpretation more complex.

Does high ARR mean a SaaS company is high quality?

No. High ARR shows a large recurring revenue base, but business quality depends on what supports that base. Retention, expansion, gross margin, acquisition cost, cash conversion, and revenue recognition all affect how useful the ARR figure is for investors.