The Rule of 40 is a SaaS metric that adds a company’s revenue growth rate to a profitability margin to judge the balance between growth and profit.

The result is useful only after the growth input, margin base, time period, company stage, and retention context are clear. A company can reach the 40% threshold through fast growth, strong profitability, or a mix of both, but the same score can describe very different business conditions.

Definition: The Rule of 40 measures a SaaS company’s growth and profitability balance by adding a growth rate to a profitability margin. A score near or above 40% is often treated as a high-level balance marker, not as a standalone business-quality verdict.

Key Points

- The Rule of 40 combines SaaS growth and profitability in one percentage-based metric.

- The formula is simple, but the inputs can vary across revenue growth, ARR growth, EBITDA margin, free cash flow margin, or adjusted profitability.

- The score carries more weight when growth quality, retention, gross margin, and cash conversion also support the result.

- A single-period score can mislead when margins are temporarily boosted, retention is weakening, or the peer set is not comparable.

What Is the Rule of 40?

The Rule of 40 is an investor-facing SaaS metric used to evaluate whether a software company is balancing revenue growth with profitability. It does not say whether a company is attractive, undervalued, or high quality by itself. It only compresses two broad operating forces into one headline number.

The metric matters because many SaaS companies reinvest heavily while scaling. A fast-growing company may look weak on margins because it is still funding sales, product development, and customer acquisition. A slower-growing company may still look durable if profitability and cash conversion are strong. The Rule of 40 creates a starting point for comparing those tradeoffs.

The score becomes more useful when the growth input is tied to recurring revenue quality. For SaaS companies, annual recurring revenue often gives a cleaner view of recurring scale than one-off revenue, especially when contracts, renewals, and expansion revenue drive the business model.

Rule of 40 Formula

The basic Rule of 40 formula is:

Rule of 40 = Revenue growth rate + Profitability margin

For example, a SaaS company growing revenue at 30% with a 12% free cash flow margin would have a Rule of 40 score of 42%.

| Formula part | Common input | Why the input matters |

|---|---|---|

| Growth rate | Revenue growth, ARR growth, MRR growth, or recurring revenue growth | The growth base affects whether the score reflects repeatable subscription expansion or a broader revenue figure. |

| Profitability margin | EBITDA margin, EBIT margin, net income margin, free cash flow margin, or adjusted margin | Different margin bases can describe different economic realities, especially when adjustments, stock-based compensation, or working-capital timing affect the result. |

| Time period | Quarterly, trailing twelve months, fiscal year, or forward estimate | A short period can reflect temporary spending, delayed collections, cost cuts, or unusual revenue timing. |

Free cash flow margin is often useful because it connects profitability to cash conversion, but it can still be distorted by billing cycles, collections, capitalized costs, or temporary expense reductions. EBITDA margin can make operating profitability easier to compare, but it may ignore cash-flow pressure and some economic costs.

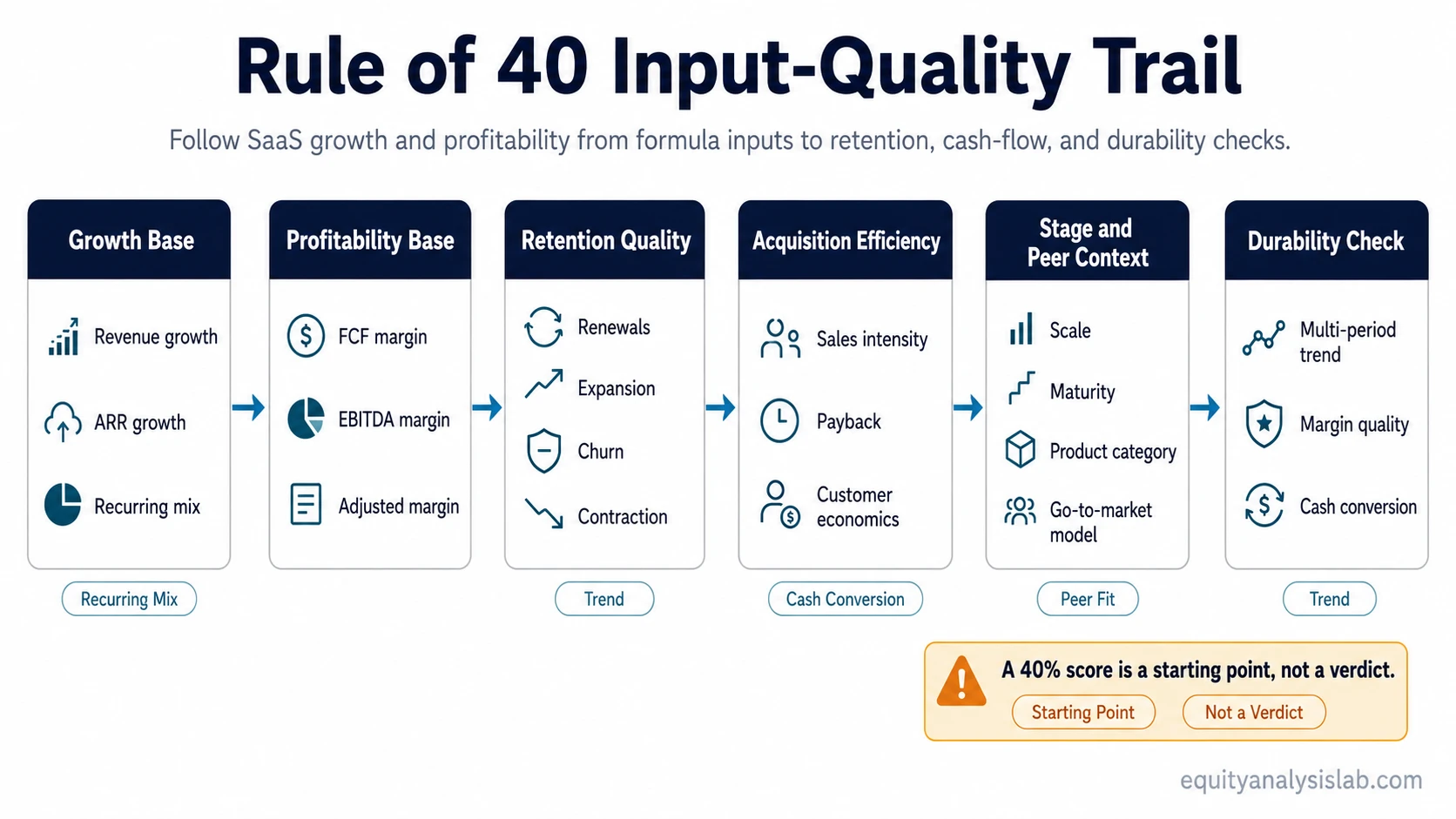

Rule of 40 Input-Quality Trail

A Rule of 40 score is only as useful as the inputs behind it. The input-quality trail separates the formula result from the business evidence that gives the result meaning.

| Input-quality checkpoint | What to check | Why it changes interpretation |

|---|---|---|

| Growth base | Revenue growth, ARR growth, net expansion, and recurring revenue mix | The score is easier to trust when growth is recurring and not mainly driven by one-time services, price timing, or low-quality volume. |

| Profitability base | EBITDA margin, free cash flow margin, adjusted margin, and stock-based compensation treatment | The same Rule of 40 score can look stronger or weaker depending on whether profitability converts into cash. |

| Retention quality | Renewals, expansion, contraction, and churn pressure | Weak retention can make a high growth rate more expensive to sustain and can reduce confidence in future recurring revenue. |

| Acquisition efficiency | Sales and marketing intensity, payback period, and new customer economics | Growth funded by inefficient acquisition can inflate the growth side while leaving future margins exposed. |

| Company stage | Early scaling, growth-stage, mature, or post-hypergrowth profile | Young SaaS companies may score through growth, while mature companies may need more profit contribution for the same score to be meaningful. |

| Peer set | Similar size, growth stage, product category, gross margin profile, and go-to-market model | A Rule of 40 comparison can mislead when a company is compared with peers that have different sales motions or margin structures. |

| Trend durability | Multi-period score, margin trend, growth trend, and cash-flow consistency | A single strong period is less useful than a pattern that holds across different spending and renewal conditions. |

Rule of 40 Example

A SaaS company reports 28% recurring revenue growth and a 14% free cash flow margin. Its Rule of 40 score is 42% because 28% plus 14% equals 42%.

At the formula level, that result sits above the 40% marker, but the number is still incomplete. It carries more weight when recurring revenue is expanding from retained customers, gross margins are stable, acquisition spending is efficient, and free cash flow reflects normal operations.

The same result deserves more caution when retention is falling, growth depends on unusually heavy customer acquisition spending, or free cash flow margin reflects temporary cost reductions. A company can reach the formula threshold while the underlying growth engine is becoming less efficient.

Sales efficiency matters because growth can be expensive even when headline revenue is rising. CAC payback period helps qualify whether customer acquisition spend is turning into recurring gross profit at a reasonable pace.

How to Interpret Different Rule of 40 Mixes

The Rule of 40 score should be read as a mix, not only as a total. Two companies can both score 40%, but one may be reinvesting for durable growth while another may be protecting margins as growth slows.

| Rule of 40 mix | Possible interpretation | What still needs to be checked |

|---|---|---|

| High growth, low margin | The company may still be prioritizing expansion over profit. | Retention, gross margin, sales efficiency, and whether losses narrow as the company scales. |

| Moderate growth, moderate margin | The company may have a balanced profile if both inputs are stable. | Whether growth and profitability persist across multiple periods rather than one clean reporting window. |

| Low growth, high margin | The company may be more mature and profit-oriented. | Whether slower growth reflects market saturation, weaker demand, stronger discipline, or a deliberate shift toward cash generation. |

| High score from temporary margin improvement | The formula may improve even if the business engine is not improving. | Cost cuts, delayed hiring, working-capital timing, capitalized costs, and whether cash conversion is repeatable. |

| Weak score with improving retention base | The current score may lag an improving revenue-quality trend. | Renewal strength, expansion revenue, customer concentration, and whether better retention can later support healthier growth and margins. |

Retention quality is especially important because recurring revenue can look strong while churn or contraction is weakening the base. Gross revenue retention helps separate revenue that is being kept from revenue that must be replaced through new sales.

When the Rule of 40 Can Mislead

Limitation: The Rule of 40 can combine growth and profitability, but it does not prove earnings quality, cash conversion, retention durability, valuation attractiveness, or future returns.

A common mistake is treating 40% as a pass/fail line. A company just above 40% is not automatically stronger than a company slightly below it. The mix of growth, margin quality, customer retention, and cash-flow durability matters more than the threshold alone.

The metric can also mislead when the margin base is not consistent. EBITDA margin, free cash flow margin, net income margin, and adjusted margin can move differently. A company may look strong on an adjusted basis while cash conversion remains weak.

Stage matters as well. Early-stage SaaS companies can score through growth while accepting low or negative margins. Mature SaaS companies may need stronger profitability because high growth is harder to maintain at scale. Comparing those companies without stage context can produce a false sense of precision.

One-period readings are especially fragile. Renewal timing, temporary expense cuts, hiring pauses, delayed marketing spend, or working-capital swings can improve the score without proving durable operating improvement.

Related SaaS Metrics That Change the Reading

The Rule of 40 is most useful when it sits beside the SaaS metrics that explain the inputs. Annual recurring revenue helps clarify the recurring growth base. CAC payback period helps test whether growth is being purchased efficiently. Gross revenue retention helps reveal whether the existing revenue base is stable enough to support future growth and margin improvement.

Those related metrics do not replace the Rule of 40. They explain why the same headline score can represent a durable balance, a temporary accounting effect, or an expensive growth profile that still needs more evidence.

FAQ

What is a good Rule of 40 score?

A score around or above 40% is often used as a high-level balance marker for SaaS growth and profitability. It should still be checked against margin base, retention quality, company stage, and multi-period durability.

Should the Rule of 40 use EBITDA margin or free cash flow margin?

Both are used, but they answer different questions. EBITDA margin can compare operating profitability, while free cash flow margin adds a cash-conversion lens. The margin base should be stated clearly before comparing companies.

Can a SaaS company meet the Rule of 40 threshold and still have weak input quality?

Yes. A company can reach the threshold through temporary cost cuts, weakly defined adjusted margins, expensive growth, or weakening retention. The score is a starting point for analysis, not a final quality verdict.