Dollar cost averaging is an investing method that spreads purchases across regular intervals instead of committing all capital on one date. It changes the timing of capital deployment, not the underlying quality, valuation, or return potential of the investment.

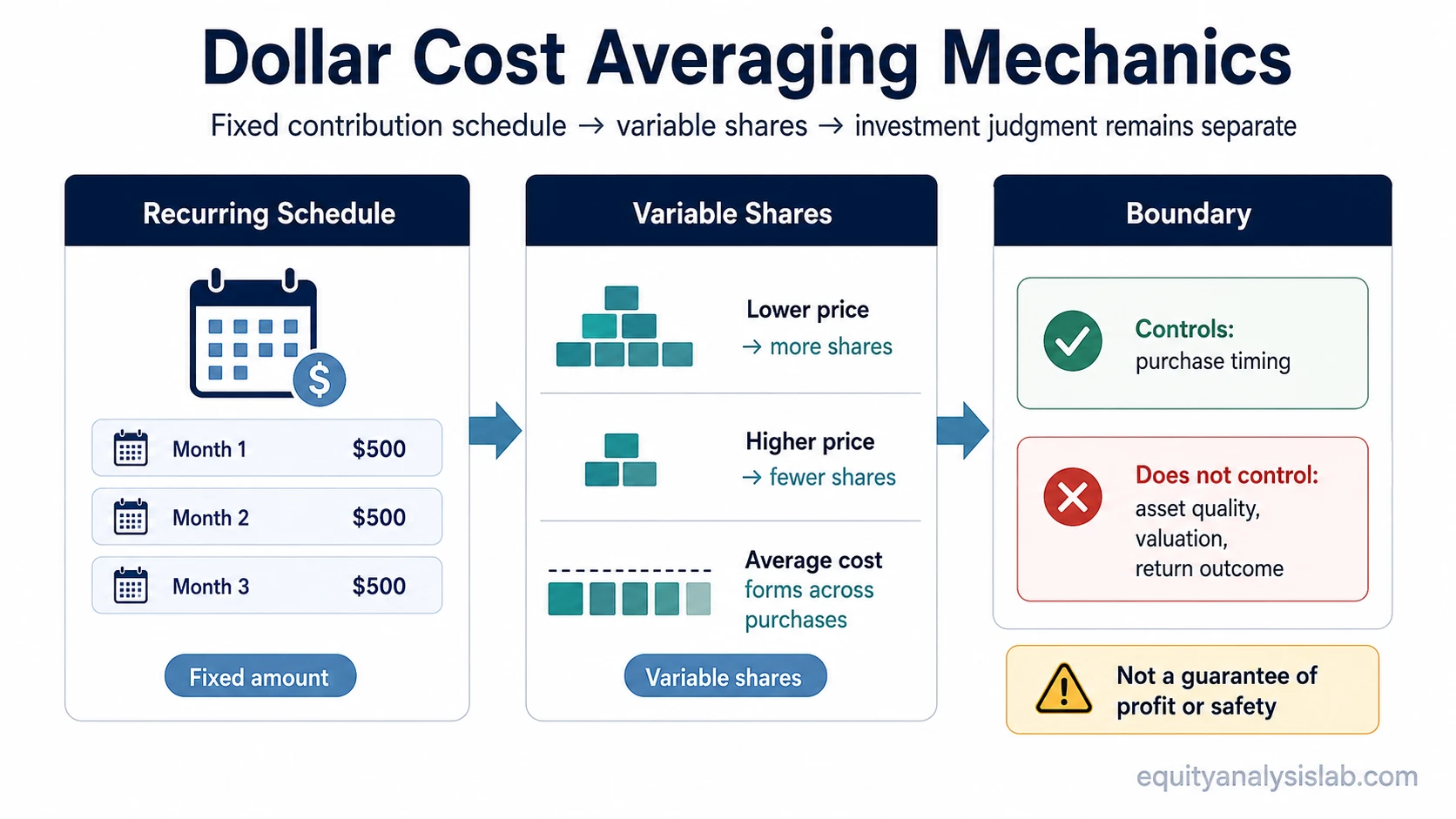

Definition: Dollar cost averaging means investing a fixed or regular amount into the same investment on a repeated schedule. When the price is lower, the fixed contribution buys more shares or units. When the price is higher, the same contribution buys fewer shares or units.

The useful boundary is simple: dollar cost averaging answers how capital is staged into an investment. It does not answer whether the investment is attractive, whether the price is reasonable, or whether the investor will avoid losses.

Key Points

- Dollar cost averaging uses a repeated investment schedule instead of a single purchase date.

- The method reduces dependence on one entry price, but it does not forecast market direction.

- Fixed contributions buy more shares at lower prices and fewer shares at higher prices.

- It is a deployment method, not a test of business quality, valuation, or return certainty.

- Costs, cash drag, opportunity cost, and asset selection still matter.

How Dollar Cost Averaging Works

A dollar-cost averaging plan has four observable inputs: the contribution amount, the interval, the investment being purchased, and the period over which purchases continue. The investor does not wait for a specific price level before each purchase. The schedule controls the purchase rhythm.

The share count changes because the contribution amount stays fixed while the purchase price changes. If the scheduled amount is $500, a lower hypothetical price buys more shares, and a higher hypothetical price buys fewer shares.

| Month | Fixed contribution | Hypothetical price | Shares bought |

|---|---|---|---|

| Month 1 | $500 | $50.00 | 10.0 |

| Month 2 | $500 | $40.00 | 12.5 |

| Month 3 | $500 | $62.50 | 8.0 |

The example is limited to purchase mechanics. It does not show a profit, a loss, a future return, or a reason to prefer the investment itself.

What Dollar Cost Averaging Controls

Dollar cost averaging controls the schedule of purchases. It can make the deployment process more systematic because the investor is not forced to choose one single purchase date for the full amount.

It also changes one-date timing exposure. A single lump-sum purchase depends heavily on the price available on one date. A staged purchase plan spreads that timing exposure across several dates, which can make the average purchase price less dependent on one market point.

| Area | What DCA can control | What DCA cannot control |

|---|---|---|

| Purchase schedule | How often capital is deployed | Whether the asset deserves investment |

| Contribution rhythm | The amount invested at each interval | Future price direction |

| One-date timing risk | Dependence on one purchase date | Loss risk after purchases are made |

| Average purchase price | The blended cost across scheduled purchases | Whether the final outcome is positive |

| Cash deployment | How quickly available cash is put to work | Opportunity cost from waiting in cash |

What Dollar Cost Averaging Does Not Control

Dollar cost averaging does not make a weak investment strong. The investment still needs to fit the investor’s objective, risk boundary, and asset-selection process. In the context of equity investing, staged purchases do not remove company risk, market risk, valuation risk, or the possibility that the investor chose the wrong exposure.

DCA also does not prove that the investment has attractive return potential. A staged purchase schedule can be consistent and still be applied to an asset with poor fundamentals, excessive valuation, weak risk-adjusted assumptions, or an unattractive return profile. The schedule should not replace analysis of the investment’s expected return drivers.

Common mistake: Treating dollar cost averaging as proof that the investment itself is good. DCA can organize how purchases happen, but it does not validate the asset, the price, or the long-term case.

Dollar Cost Averaging vs Market Timing

Dollar cost averaging is different from market timing. Market timing tries to choose entry points based on expected price movement. Dollar cost averaging uses a schedule, so each purchase happens because the interval arrives, not because the investor believes the price is ideal.

This can reduce the pressure of choosing one perfect entry point. It does not remove the need to understand what is being bought, and it does not mean the investor is protected if the asset declines after the scheduled purchases.

Dollar Cost Averaging vs Lump-Sum Investing

Lump-sum investing commits the available capital at once. Dollar cost averaging commits capital in stages. The distinction matters most when the investor already has a meaningful amount of cash available and must decide whether to deploy it immediately or over time.

The comparison should stay narrow. Lump-sum investing may do better when markets rise strongly after the first date because more capital is invested earlier. Dollar cost averaging may reduce regret from a poorly timed single purchase, but it can also leave cash undeployed while prices rise.

Limits of Dollar Cost Averaging

Dollar cost averaging does not guarantee profit and does not prevent loss. If the investment declines over the full period or remains fundamentally unattractive, spreading purchases over time cannot turn the outcome into a safe one.

Cash drag and opportunity cost are also real limitations. When capital is held back for future scheduled purchases, that cash may miss gains if the market rises before it is deployed. In that environment, a staged approach can underperform a lump-sum approach.

Transaction costs may matter when each scheduled purchase creates a fee, spread, commission, tax friction, or other trading cost. The impact depends on the account structure, the instrument, the purchase size, and the frequency of transactions.

Dollar cost averaging can support regular participation, but compounding still depends on time, reinvestment, return path, asset quality, and the investor’s ability to stay invested through uncertainty.

Inputs That Define a Dollar-Cost Averaging Plan

A dollar-cost averaging plan is easier to evaluate when the inputs are explicit. The basic inputs are the amount contributed at each interval, how often purchases occur, what asset or fund is being purchased, how long the schedule will continue, and whether the cash flow is recurring or already available as a lump sum.

The final input is the investment boundary. A purchase schedule does not replace analysis of the asset’s risk, valuation, and return assumptions. The more uncertain those assumptions are, the more important it becomes to separate the deployment method from the investment judgment.

Related Investing Concepts

Dollar cost averaging connects to three nearby concepts: the growth mechanism after capital is invested, the ownership exposure being built, and the return assumptions behind the asset itself.

- Compounding explains the growth mechanism that may operate after capital is invested.

- Equity investing places DCA inside ownership-based investing rather than short-term trading.

- Return assumptions help separate a purchase plan from the investment’s risk and reward profile.

FAQ

Is dollar cost averaging the same as market timing?

No. Dollar cost averaging uses a regular purchase schedule. Market timing tries to choose purchase dates based on expected price movement.

Can dollar cost averaging lose money?

Yes. Dollar cost averaging does not protect against losses if the investment declines, remains overvalued, or fails to produce attractive long-term returns.

Is dollar cost averaging always better than lump-sum investing?

No. Dollar cost averaging can reduce dependence on one purchase date, but lump-sum investing can perform better when prices rise after the initial investment date.

What inputs define a dollar-cost averaging plan?

The main inputs are contribution amount, purchase interval, investment choice, time horizon, cash source, transaction costs, and the risk boundary for the asset being purchased.