Equity investing means allocating capital to business ownership exposure, usually through publicly traded stocks or pooled vehicles that hold stocks. That exposure can benefit from business growth, dividends, or higher market valuation, but it can also lose value when fundamentals, valuation, dilution, leverage, or investor behavior work against it.

Definition: Equity investing is investing for ownership exposure. The investor participates in the economics of a business or a group of businesses, but the value of that exposure depends on evidence: business quality, cash generation, earnings durability, valuation, balance-sheet risk, share count changes, and portfolio context.

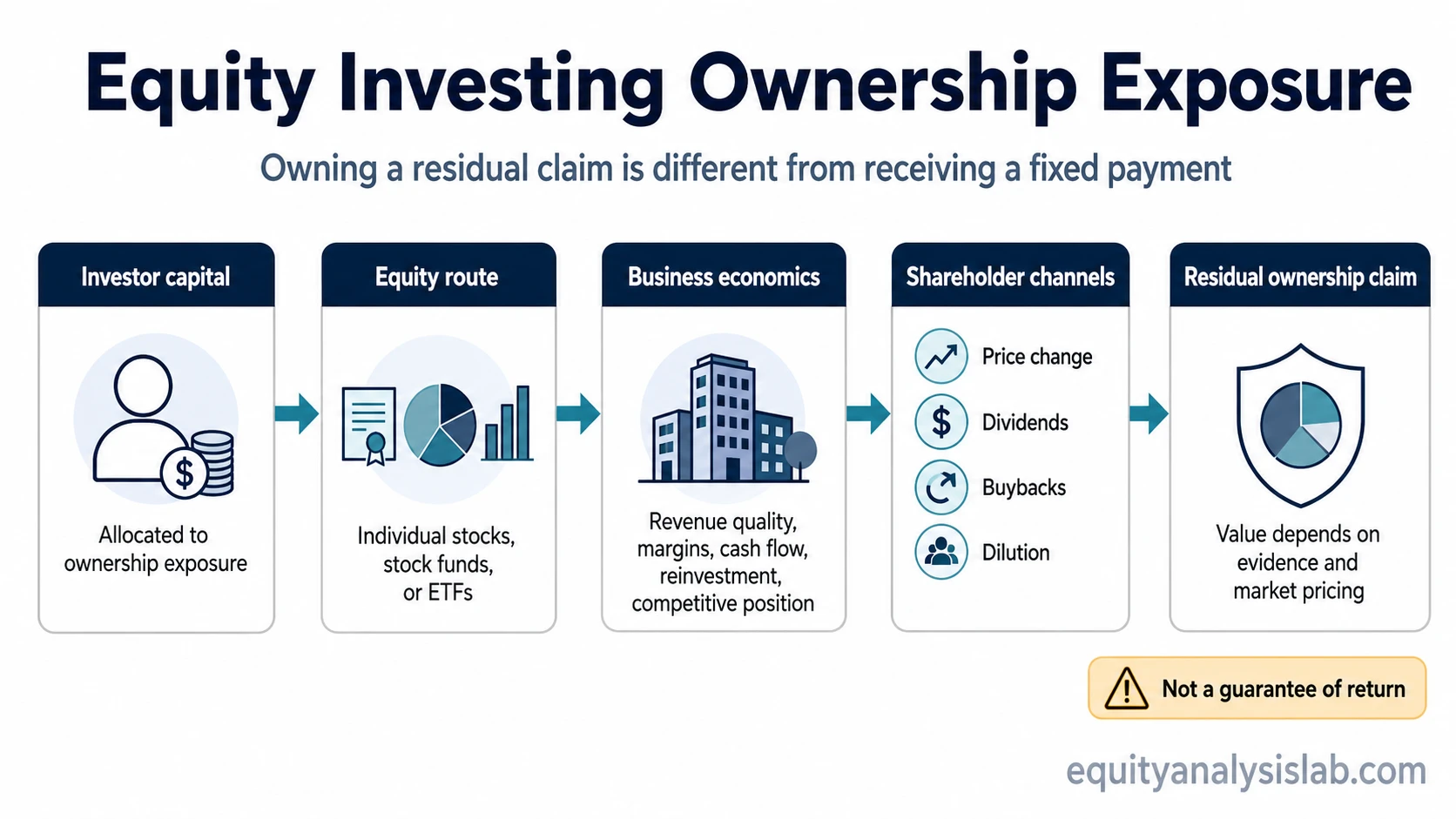

Key points about equity investing

- Equity investing is ownership-based exposure, not a fixed payment contract.

- The exposure can come through individual stocks, equity funds, or ETFs that hold stocks.

- Returns can come from price appreciation, dividends, or both, but neither is guaranteed.

- The same equity label can hide very different risks depending on valuation, cash flow, leverage, dilution, and concentration.

- Equity exposure is more useful to analyze when the ownership claim is connected to evidence rather than narrative alone.

What equity investing means

Equity investing starts with a claim on business ownership. A common share represents a residual claim: after expenses, lenders, taxes, reinvestment needs, and other obligations, shareholders participate in what remains. That residual nature is why equity can offer upside when a business compounds value, but it is also why equity can absorb large losses when the business weakens or the market reprices it.

The word “equity” can sound broad, but in an investing context it usually points to stocks or stock-based exposure. The core question is not simply whether something is an equity. The more useful question is what the claim is worth, how durable the underlying business economics are, and what risks can change the outcome.

How equity ownership works

Equity value changes through several channels. Business performance matters because revenue quality, margins, cash conversion, reinvestment needs, and competitive position shape the economics available to shareholders. Market valuation matters because even a strong business can become a poor investment outcome if the starting price already reflects unrealistic expectations.

Dividends and buybacks can also affect shareholder economics. Dividends distribute part of the company’s cash to owners. Buybacks can reduce share count when executed at sensible prices, while new share issuance or other dilution can spread the same business value across more claims. The investor’s economic exposure can therefore change even when the business name stays the same.

Portfolio design changes the practical meaning of equity exposure. Owning one company, owning a basket of companies, and owning a broad equity fund are all equity investing routes, but they create different concentration, diversification, fee, and behavior risks.

Equity investing vs related terms

Several terms sit close to equity investing, but they do not mean exactly the same thing. The distinctions matter because the wrong label can lead to the wrong analysis.

| Term | Meaning | Investor relevance | Boundary |

|---|---|---|---|

| Equity investing | Allocating capital to ownership exposure in businesses. | Frames the investor as an owner of residual business economics. | Not automatically attractive; the evidence still has to support the ownership claim. |

| Equities or stocks | Shares that represent ownership interests in companies. | Usually the main instrument used for public equity exposure. | A stock is the instrument; equity investing is the broader ownership activity. |

| Equity funds or ETFs | Pooled vehicles that hold stocks or stock-like exposure. | Can spread exposure across many companies, sectors, or regions. | The fund wrapper does not remove valuation, concentration, cost, or behavior risk. |

| Shareholder equity | An accounting measure of assets minus liabilities on a balance sheet. | Can help analyze a company’s capital base and book value context. | It is not the same as the act of investing in equities. |

| Private equity | Ownership exposure in private companies or private-company transactions. | Can involve equity ownership outside public stock markets. | It has different liquidity, access, valuation, and structure questions. |

What changes the meaning of equity exposure

Equity investing becomes clearer when the ownership label is separated from the evidence behind it. A stock, fund, or portfolio can all create equity exposure, but the interpretation depends on what the exposure actually represents.

| Analytical layer | Question to ask | Why it changes interpretation |

|---|---|---|

| Business quality | Does the company have durable economics, pricing power, or a defensible position? | Ownership is more fragile when the business depends on weak margins, temporary demand, or constant reinvestment without clear returns. |

| Cash flow | Does accounting profit convert into cash after operating needs and reinvestment? | Cash flow can reveal whether the ownership claim is backed by economic substance rather than narrative alone. |

| Earnings quality | Are earnings recurring, cash-supported, and not driven mainly by one-off items? | Weak earnings quality can make equity exposure look better than the underlying business really is. |

| Valuation context | What expectations are already reflected in the price? | A strong business can still disappoint investors if the purchase price assumes too much future growth. |

| Balance-sheet risk | Can debt, refinancing needs, or liquidity pressure reduce the value left for shareholders? | Equity sits below lenders in the capital structure, so leverage can magnify both upside and downside. |

| Share count changes | Is ownership being diluted or supported by sensible capital returns? | New shares can weaken per-share economics, while buybacks can help only when price, funding, and business quality make sense. |

| Portfolio exposure | How much of the investor’s total exposure depends on one company, sector, country, or factor? | The same equity idea can carry very different risk when it is concentrated rather than diversified. |

Basic routes to equity exposure

Individual stocks give direct ownership exposure to specific companies. That can make the analysis more company-specific because the investor has to judge business quality, financial statements, valuation, management decisions, competitive position, and risks that may affect one company more than the market as a whole.

Equity funds and ETFs create pooled exposure. The analysis shifts from one company to the fund’s holdings, weighting method, costs, tax mechanics, concentration, tracking behavior, and category design. A broad stock fund and a narrow sector fund are both equity exposure, but they do not carry the same practical risk.

Implementation style also matters. Active selection, passive rules-based exposure, periodic contribution plans, and long holding periods are different decisions around equity exposure. None of them removes the need to understand what is owned, what price is paid, and what could change the outcome.

Simple equity investing example

Consider two generic companies whose shares both give investors equity ownership. Company A produces steady cash flow, uses little debt, keeps share count stable, and trades at a valuation that leaves room for moderate expectations. Company B reports fast revenue growth but burns cash, issues new shares regularly, and trades at a price that already assumes very strong future results.

Both investments are equities. The label is the same, but the ownership economics are different. Company A may still be overpriced or face business risk. Company B may still become valuable if its economics improve. The point is that the equity label does not answer the investment question by itself; it only identifies the type of claim being analyzed.

Risks and limitations of equity investing

Equity investing does not guarantee a return. The investor owns exposure to uncertain business results and uncertain market pricing. A company can grow while its stock performs poorly if expectations were too high. A cheap-looking stock can stay cheap or become cheaper if the business deteriorates. A diversified equity fund can still decline when broad market risk rises.

The central trade-off is that equity investors accept uncertainty in exchange for the possibility of participating in business growth and market revaluation. The balance depends on price, quality, time horizon, diversification, and behavior under stress.

Common mistake: treating ownership as the conclusion. Ownership is only the starting claim. The investment case still has to be tested against cash flow, valuation, durability, dilution, balance-sheet risk, and portfolio exposure.

Time horizon and compounding

Equity investing is often discussed in long-term language because business value can take time to develop. A longer holding period can give business results more time to matter, but time alone does not fix weak valuation, poor cash generation, permanent dilution, excessive leverage, or a broken business model.

Compounding can become relevant when earnings, cash flows, or retained capital are reinvested productively. The same concept can work against the investor when losses, dilution, or poor capital allocation accumulate over time. Time horizon is therefore not only about calendar length; it is also about whether the evidence supports the chosen holding period.

Related investing concepts

Related investing concepts clarify the broader decision framework around equity exposure, including risk, expected return, compounding, contribution method, selection style, and holding period.

| Concept | Why it matters after equity investing |

|---|---|

| Risk and return | Clarifies the upside/downside trade-off behind uncertain equity outcomes. |

| Expected return | Organizes scenarios, probabilities, valuation, and possible outcomes without treating them as promises. |

| Compounding | Explains how retained gains, losses, reinvestment, or dilution can change the base over time. |

| Dollar-cost averaging | Separates a contribution method from the quality or valuation of the equity exposure itself. |

| Active vs passive investing | Separates judgment-led selection from rules-based exposure. |

| Long-term vs short-term investing | Shows how holding period changes the way evidence, risk, and behavior should be interpreted. |

FAQ

Is equity investing the same as stock investing?

Stock investing is the most common form of equity investing in public markets. Equity investing is the broader idea of owning business exposure, while stocks are one instrument used to get that exposure.

Can equity investing include funds or ETFs?

Yes. Equity funds and ETFs can provide equity exposure when they hold stocks or stock-like ownership interests. The analysis then includes holdings, weighting, costs, concentration, and tracking behavior, not only the equity label.

Does equity investing guarantee higher returns?

No. Equity investing can participate in business growth and market revaluation, but outcomes depend on business results, valuation, dilution, balance-sheet risk, time horizon, diversification, and investor behavior.