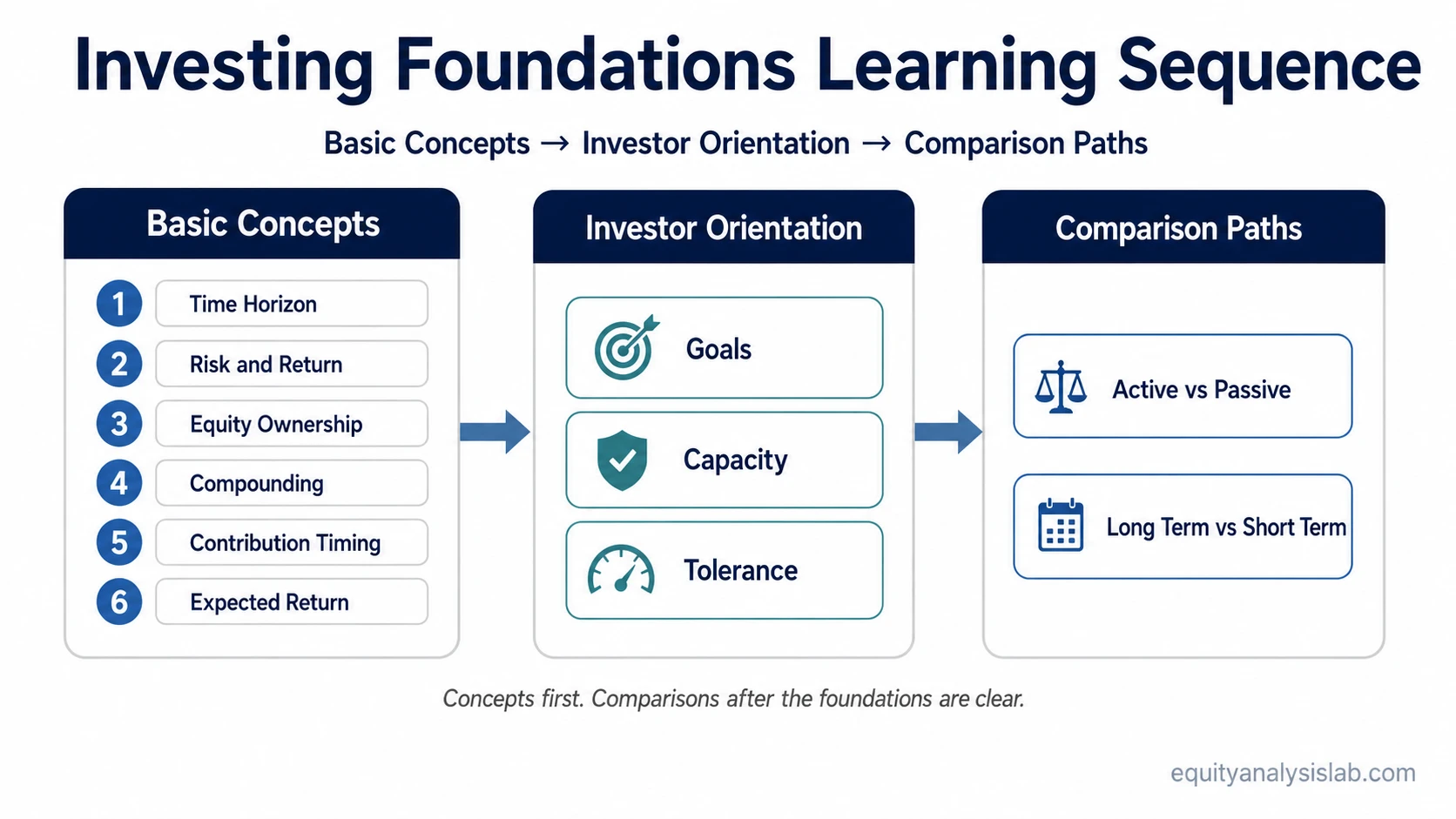

Basic investing concepts are the foundational ideas that shape investment decisions before stock selection, valuation, or portfolio construction begins. The main buckets are time, risk, ownership, contribution timing, and return assumptions. They create a learning sequence, not personal advice, product selection, or a forecast.

Definition: Basic investing concepts are the core ideas investors use to understand what they own, how long they may hold it, what risk they accept, how returns may accumulate, and which assumptions still need to be tested.

Key Points

- Time horizon comes first because the same asset can carry different risks over different holding periods.

- Risk and return should be understood before stock selection because higher potential reward usually comes with more uncertainty.

- Ownership, contribution timing, compounding, and expected return are separate ideas, even when they interact in one investment plan.

- Comparison topics are easier to evaluate after the core vocabulary is clear.

What Are Basic Investing Concepts?

Basic investing concepts help separate the moving parts behind an investment decision. They do not tell an investor what to buy. They clarify the conditions that make a decision understandable: how long capital may be invested, what uncertainty is being accepted, what type of exposure is being owned, how contributions are made, and what return assumption is being used.

The first useful distinction is between concept knowledge and product choice. A stock, fund, ETF, or portfolio mix is a possible expression of an investment decision. The concepts underneath the decision explain why time, risk, ownership, and assumptions matter before any product or security is considered.

Which Investing Concepts Should Come First?

The strongest learning order starts with the constraints that shape every later decision. Time and risk come before return assumptions because they define the boundary of the decision. Ownership and compounding come next because they explain what is being held and how growth may build. Contribution timing and comparison topics are easier to judge after those foundations are clear.

Priority learning path: Start with time horizon, then risk and return, then ownership exposure, then compounding, then contribution timing, then expected return. After that, compare active and passive approaches, and separate long-term from short-term investing.

| Learning order | Concept | Why it comes here |

|---|---|---|

| 1 | investment time horizon | Time changes liquidity needs, volatility tolerance, compounding potential, and the cost of being wrong. |

| 2 | risk and return | Risk frames the uncertainty accepted in pursuit of possible reward. |

| 3 | stock ownership through equity investing | Ownership exposure explains what a stock investor participates in and what risks remain. |

| 4 | compounding | Compounding explains how returns can build on prior gains over time, without guaranteeing the outcome. |

| 5 | dollar-cost averaging | Contribution timing matters after the investor understands what is being bought and why time matters. |

| 6 | expected return | Expected return is an assumption, not a promise, and it should be judged against risk and time. |

Core Concepts by Investor Decision

Each concept answers a different decision question. Treating them as one long vocabulary list makes the learning sequence weaker. A cleaner structure starts with the decision being made and then routes to the concept that helps clarify that decision.

| Investor question | Concept bucket | What the concept clarifies |

|---|---|---|

| How long can capital remain invested? | Time horizon | Whether the decision is short-term, intermediate, or long-term in nature. |

| What uncertainty is being accepted? | Risk and return | The relationship between possible reward, possible loss, volatility, and uncertainty. |

| What is actually being owned? | Equity investing | Participation in business ownership, including earnings, valuation, and company-specific risk. |

| How can growth build over time? | Compounding | The effect of returns building on prior returns when capital remains invested. |

| How should purchases be spaced? | Dollar-cost averaging | The difference between investing all at once and spreading contributions over time. |

| What return assumption is being used? | Expected return | The estimate behind a decision, including the risk that the estimate is wrong. |

How the Main Concepts Connect

The concepts are linked, but they are not interchangeable. Time horizon affects how volatility is experienced. Risk and return frame the uncertainty behind possible outcomes. Equity investing explains the ownership exposure. Compounding explains how outcomes may accumulate. Contribution timing affects the path into the exposure. Expected return summarizes an assumption, not a guaranteed result.

Connection: A long time horizon can make compounding more relevant, but it does not remove risk. Dollar-cost averaging can reduce timing pressure, but it does not guarantee a better outcome than lump-sum investing. Expected return can guide assumptions, but it remains uncertain.

Comparison Paths After the Basics

Comparison topics become more useful after the core concepts are clear. Active versus passive investing is easier to understand when the reader already knows what equity exposure, return assumptions, and risk tradeoffs mean. Long-term versus short-term investing is clearer after the role of time horizon has been separated from product choice or market timing.

| Comparison path | Best read after | Reason |

|---|---|---|

| active vs passive investing | Risk and return, equity investing, expected return | The comparison depends on assumptions about skill, costs, diversification, tracking, and decision responsibility. |

| long-term vs short-term investing | Time horizon, compounding, risk and return | The distinction depends on holding period, volatility tolerance, and whether the decision is based on ownership or timing. |

What Stays Outside the First Concept Path?

Some investing topics are important, but they belong later in the learning path. Company analysis, valuation, portfolio construction, and investor decision process topics require the basic concepts first. Without the foundations, a valuation method or portfolio framework can look more precise than it really is.

Boundary: Basic investing concepts do not replace company analysis, valuation, portfolio construction, or personal financial planning. They create the vocabulary needed before those topics can be evaluated clearly.

| Later topic | Why it comes later |

|---|---|

| Company analysis | Business quality, financial statements, and earnings quality require a clearer understanding of ownership and risk. |

| Valuation | Valuation depends on assumptions about return, growth, discount rates, and uncertainty. |

| Portfolio construction | Allocation, diversification, and concentration require risk, time horizon, and exposure vocabulary. |

Common Mistakes When Learning Investing Concepts

Mistake: Treating a concept as a rule. Compounding, dollar-cost averaging, diversification, and expected return are useful ideas, but none of them guarantees a favorable outcome.

Mistake: Starting with products before understanding exposure. A product label does not explain what risk is being accepted, what is being owned, or which assumption drives the decision.

Mistake: Confusing expected return with a forecast. Expected return is a planning input. It can be wrong if assumptions about valuation, growth, risk, or time are wrong.

Mistake: Assuming diversification eliminates risk. Diversification can reduce some concentration risk, but it cannot remove market risk, valuation risk, behavioral risk, or poor assumptions.

Limitation: Basic investing concepts improve decision clarity, but they do not remove uncertainty. They help organize questions around time, risk, ownership, contribution timing, and assumptions. They do not identify the best investment, guarantee returns, or replace analysis of a specific company, fund, or portfolio.

Basic Investing Concepts FAQ

What are the most important basic investing concepts?

The most important basic investing concepts are time horizon, risk and return, equity ownership, compounding, contribution timing, and expected return. These concepts help organize decisions before stock selection, valuation, or portfolio construction begins.

Why should risk and return come before stock selection?

Risk and return come before stock selection because every potential reward has uncertainty attached to it. A stock idea can look attractive in isolation, but the decision is incomplete without understanding possible loss, volatility, valuation risk, and the investor’s time horizon.

Is dollar-cost averaging always better than lump-sum investing?

No. Dollar-cost averaging spreads purchases over time, which can support discipline and reduce timing pressure. It is not automatically better in every market or for every investor because the result depends on prices, time horizon, cash flow, and opportunity cost.

Does compounding guarantee long-term gains?

No. Compounding describes how returns can build on prior gains when capital remains invested, but losses can also compound. The concept depends on the path of returns, time, reinvestment, and the quality of the underlying investment decision.