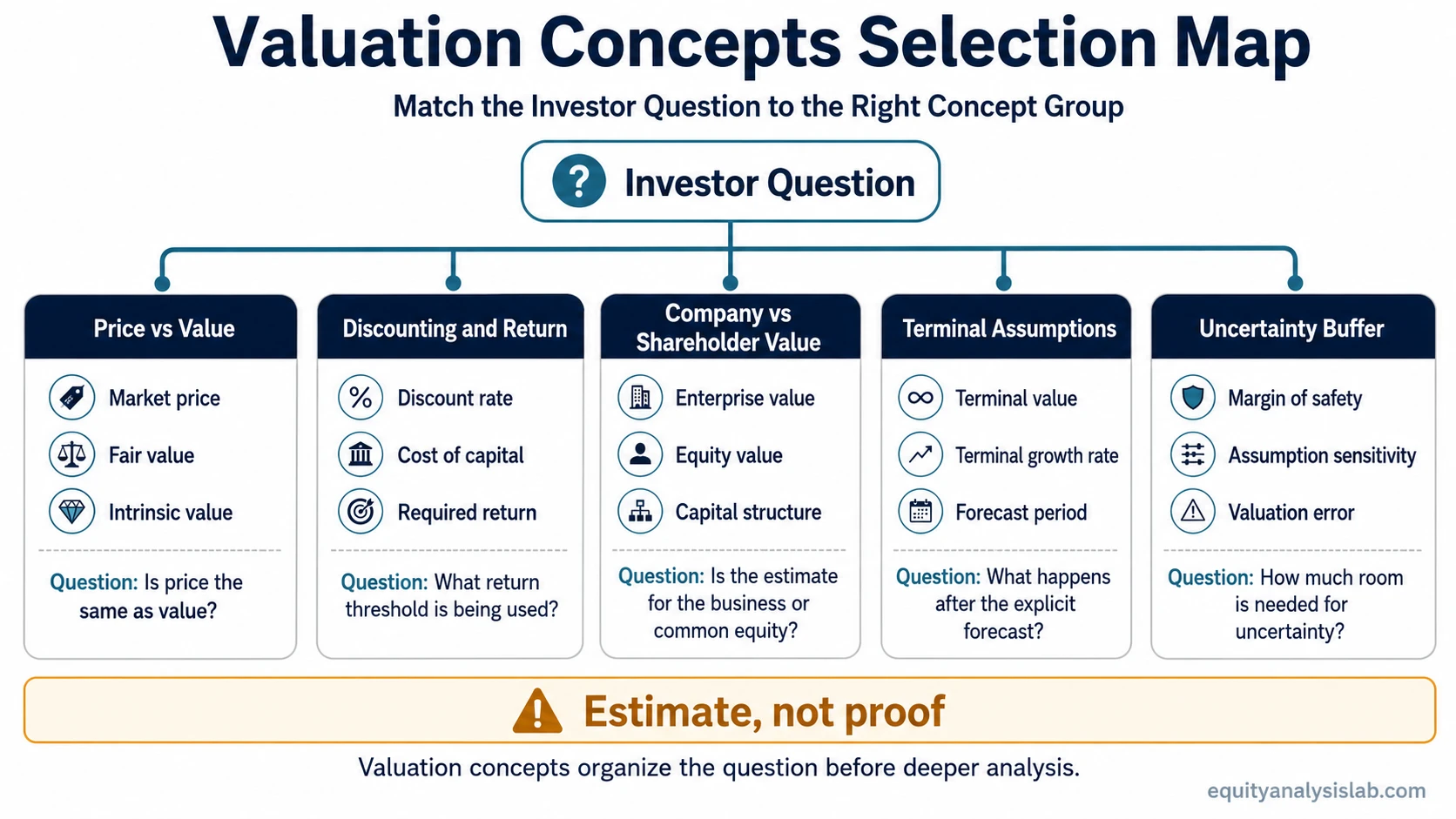

Valuation concepts are the terms investors use to separate price, value, required return, company value, terminal assumptions, and uncertainty before deeper company analysis.

The useful starting point is not every valuation method at once. It is the specific confusion the investor is trying to resolve: whether market price differs from estimated value, whether the required return is reasonable, whether the value belongs to the whole company or only common shareholders, or whether the final estimate depends too heavily on long-range assumptions.

Key Points

- Valuation concepts organize the language behind valuation before a model or spreadsheet is built.

- Price, fair value, and intrinsic value answer different questions, so they should not be treated as interchangeable.

- Discounting concepts connect future cash flows, risk, and the return an investor requires.

- Enterprise value and equity value separate the value of the operating business from the value attributable to shareholders.

- Precise valuation output can still be fragile when growth, discount rates, terminal assumptions, or multiples drive most of the result.

What Valuation Concepts Help Separate

Valuation language becomes useful when it separates similar-looking ideas that lead to different conclusions. A stock price is an observed market quote. A value estimate is an analytical judgment. A required return is the return threshold used to judge whether future cash flows compensate for risk. A terminal assumption is the part of the estimate that reaches beyond the explicit forecast period.

The purpose is not to make a valuation result look certain. The purpose is to make the assumptions visible enough that the investor can see which part of the conclusion is doing the most work.

| Investor confusion | Concept group to start with | What the group clarifies |

|---|---|---|

| Is market price the same as value? | Price and value definitions | Separates quoted price, estimated value, and the investor’s analytical judgment. |

| How should future value be adjusted for risk? | Discounting and required return | Connects expected cash flows, risk, time, and return thresholds. |

| Does the estimate refer to the whole company or shareholders? | Company value versus shareholder value | Separates operating business value from the value attributable to common equity. |

| Why does the long-term assumption dominate the estimate? | Terminal assumptions | Shows how value beyond the forecast period can shape the final result. |

| How much uncertainty should be allowed? | Safety and uncertainty concepts | Frames the gap between a value estimate and the price an investor is willing to pay. |

Valuation Concept Groups by Investor Question

Each valuation question points toward a different concept group. The goal is to identify the term that handles the specific valuation problem before moving into a model or detailed method.

| Question | Start with | Then compare with | Why it matters |

|---|---|---|---|

| What is the business worth apart from today’s quote? | intrinsic value | fair value estimates | These concepts separate analytical value from the price currently visible in the market. |

| How does the market currently value the equity? | market capitalization | Price and value boundaries | Market capitalization reflects the market value of common equity, not necessarily the intrinsic worth of the business. |

| How should future cash flows be converted into present value? | a valuation discount rate | cost of capital | Discounting concepts show how risk, time, and required compensation affect present value. |

| What return threshold is being used? | required rate of return | Capital Asset Pricing Model | These concepts help explain whether the assumed return hurdle is internally consistent. |

| Is the estimate about the business or the common stock? | enterprise value | equity value | Enterprise value looks at the whole operating business, while equity value focuses on what belongs to shareholders after debt and other claims. |

| What happens after the explicit forecast period? | terminal value assumptions | terminal growth rate | Terminal assumptions can dominate a valuation if the forecast period is short relative to the company’s expected life. |

| How much room is needed for valuation error? | margin of safety | Assumption sensitivity | The safety buffer accounts for the possibility that growth, margins, discount rates, or terminal assumptions are wrong. |

Which Valuation Concept to Start With

Start with intrinsic value when the main question is whether the market price differs from a reasoned estimate of business value. Intrinsic value is usually the central concept when the investor is trying to think beyond a quoted share price.

Start with fair value when the issue is whether a current estimate looks reasonable under a defined set of assumptions. Fair value language is useful when the discussion needs a stated basis rather than a vague claim that something is cheap or expensive.

Start with discount rate, cost of capital, or required rate of return when the estimate is most sensitive to the return threshold. This is common when two investors agree on the same future cash flows but disagree about how risky those cash flows are.

Start with enterprise value and equity value when the question is about capital structure. A company with debt, cash, preferred claims, or non-operating assets can look different depending on whether the valuation begins with the whole firm or with common equity.

Start with terminal value and terminal growth rate when most of the estimate comes from the period after the explicit forecast. In that situation, the model may look detailed, but a small long-term growth assumption can carry much of the conclusion.

Start with margin of safety when the estimate is already formed but uncertainty remains. The concept does not prove that a stock is attractive. It shows how much room exists between the estimate and the price before errors in the assumptions become damaging.

How Valuation Concepts Fit Together

Most valuation concepts fit into an assumption stack rather than a simple list. The investor begins with business evidence such as earnings power, free cash flow, margins, reinvestment needs, balance-sheet risk, and competitive durability. Those inputs shape the expected cash flows or earnings base.

The next layer is the return requirement. A higher discount rate or required rate of return lowers the present value of future cash flows. A lower one raises it. This is why valuation can change materially even when the business forecast itself has not changed.

The final layer is the value output and uncertainty buffer. Enterprise value, equity value, intrinsic value, fair value, and margin of safety are not competing labels for the same number. They describe different positions in the chain from business evidence to investor judgment.

Valuation Assumption Stack

Business evidence: revenue quality, margins, cash flow, reinvestment needs, debt, dilution, and competitive durability.

Return requirement: discount rate, cost of capital, required rate of return, and risk assumptions.

Long-range assumption: terminal value, terminal growth rate, normalized margins, and exit multiple logic where relevant.

Value output: enterprise value, equity value, fair value, intrinsic value, and market capitalization comparison.

Uncertainty buffer: margin of safety and sensitivity review before any conclusion is treated as robust.

Where Valuation Concepts Can Mislead

Valuation concepts can make an estimate look more precise than it really is. A spreadsheet may produce an exact number, but the conclusion can still depend heavily on growth assumptions, discount rates, terminal value, normalized margins, or the multiple used at the end of the model.

A valuation term should therefore be treated as a way to identify the assumption being discussed, not as proof that a stock is attractive. If the main conclusion changes when one input moves slightly, the problem is not the vocabulary. The problem is assumption sensitivity.

What This Scope Does Not Cover

Valuation concepts do not replace full company research. A complete valuation still needs business model analysis, earnings quality review, cash-flow analysis, balance-sheet context, competitive position, management and capital allocation judgment, and comparison with plausible alternatives.

These concepts also do not create price targets or investment recommendations. They make the valuation discussion cleaner by showing which assumption is being tested and where the conclusion may be fragile.

Related Concept Comparisons

When the main confusion is between return inputs, use the comparison between discount rate vs WACC after reviewing discount rate and cost of capital separately.

When the main confusion is capital-structure language, use enterprise value vs equity value after the two standalone concepts are clear.

FAQ

What are valuation concepts?

Valuation concepts are the core terms investors use to discuss price, value, required return, company value, shareholder value, terminal assumptions, and uncertainty in a valuation process.

Are valuation concepts the same as valuation methods?

No. Valuation concepts define the ideas used inside valuation work, while valuation methods are broader procedures such as discounted cash flow analysis, relative valuation, or asset-based valuation.

Which valuation concept should an investor learn first?

Intrinsic value is often the best starting point when the question is price versus value. Discount rate, cost of capital, and required return become more important when the question is how risk changes present value.

Can valuation concepts prove that a stock is undervalued?

No. They help organize assumptions and clarify the valuation discussion, but they do not prove that a stock is attractive or that future returns will follow the estimate.

How to Choose the Next Valuation Concept

The most useful next step is to name the uncertainty first. If the question is price versus value, start with value definitions. If the question is risk adjustment, start with discounting and required return. If the question is sensitivity, start with terminal assumptions and margin of safety before treating any estimate as robust.