A discount rate is the rate used to convert expected future cash flows into present value. In equity valuation, it represents the return required for the risk, timing, and type of cash flows being valued. A higher discount rate lowers present value, while a lower rate raises it, so the assumption can materially change a valuation output.

Discount rate definition: A discount rate is a valuation input used to translate future cash flows into today’s value. It is not a stock conclusion, price target, or proof that a company is cheap or expensive.

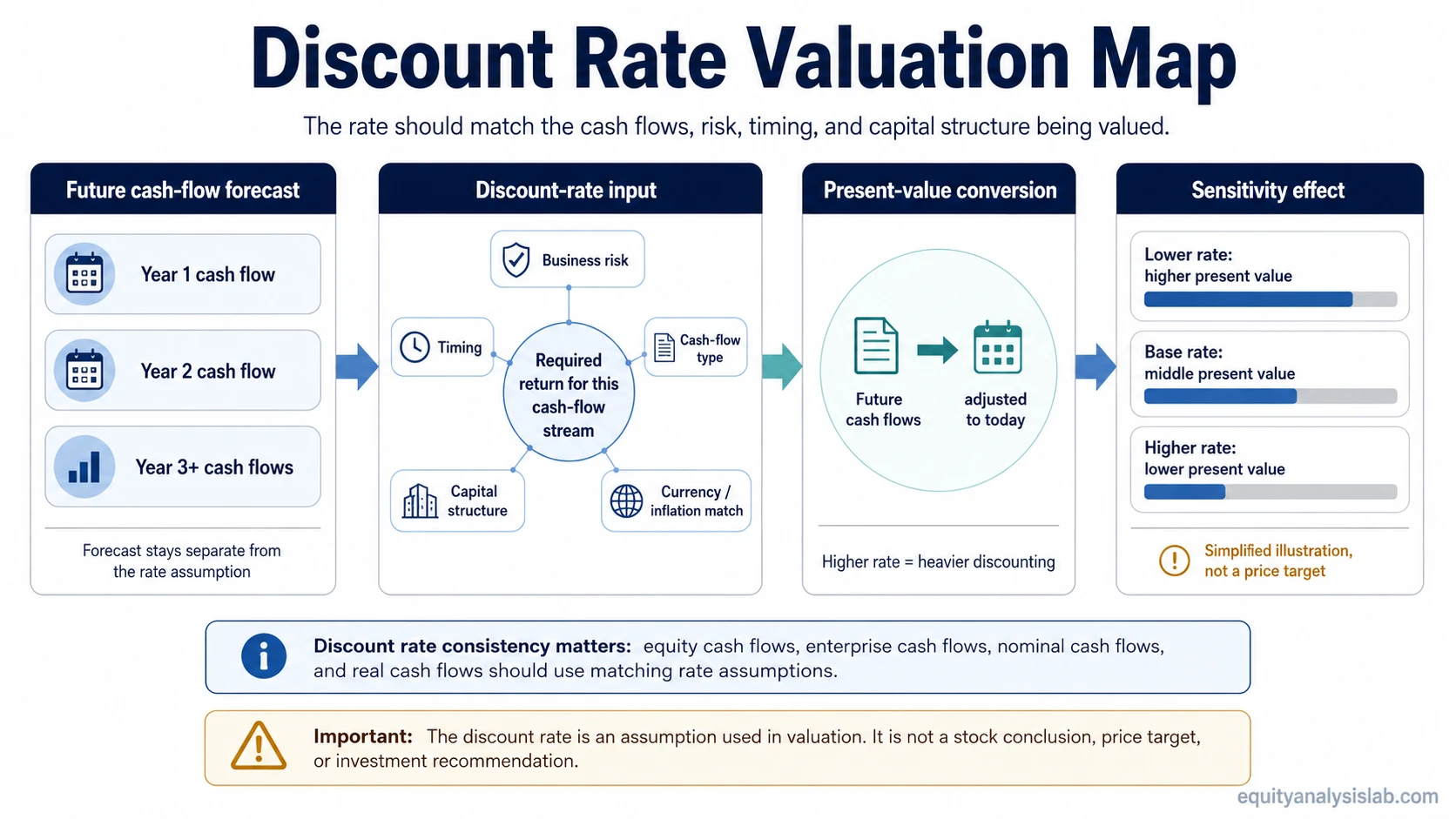

Key Points About the Discount Rate

- A discount rate converts future cash flows into present value.

- The rate should match the risk, timing, currency, and cash-flow type being valued.

- Higher discount rates reduce present value; lower discount rates increase present value.

- The discount rate is a valuation assumption, not a buy or sell conclusion.

What Is a Discount Rate?

A discount rate is the rate applied to future cash flows so they can be compared with value today. The idea is that a dollar expected in the future is not worth the same as a dollar available now, because the future dollar carries time, uncertainty, and opportunity-cost risk.

In a valuation model, the discount rate acts as the bridge between a cash-flow forecast and a present-value estimate. If the future cash flows are riskier, further away, or less predictable, the rate usually needs to reflect that higher uncertainty. If the cash flows are more stable and closer in time, the required rate may be lower, depending on the valuation context.

A simple present-value idea is:

Present value logic: Present value equals a future cash flow adjusted downward by a discount rate over time. The further away or riskier the cash flow is, the more sensitive the valuation can become to the rate assumption.

Simple one-period logic: Present value equals expected future cash flow divided by one plus the discount rate. Multi-period valuations extend the same idea across forecast years.

Where the Discount Rate Fits in Valuation

The discount rate is one part of a wider valuation assumption set. It does not work alone. A valuation estimate also depends on the cash-flow forecast, growth assumptions, terminal assumptions, reinvestment needs, capital structure, and business risk.

For an equity investor, the discount rate helps answer a practical question: what rate is reasonable for converting this specific stream of expected cash flows into present value? That makes the discount rate different from a general market opinion. It must be tied to the type of cash flow being valued.

Some valuation inputs can come from models such as the Capital Asset Pricing Model, but the discount-rate input still has to match the valuation perspective and the cash-flow stream. The important point is that the discount-rate input must be consistent with the valuation setup.

Discount Rate Assumption Stack

A discount rate is easier to interpret when it is treated as an assumption stack rather than a single isolated number. The rate should reflect what is being valued, how risky the cash flows are, and whether the valuation is being performed from an equity or enterprise perspective.

| Assumption layer | Question it answers | Why it matters for the discount rate |

|---|---|---|

| Cash-flow type | Are the cash flows to equity holders, to the firm, or to a specific project? | The rate should match the claim on the cash flows being valued. |

| Business risk | How stable, cyclical, or uncertain are the expected cash flows? | Riskier cash flows usually require a higher return assumption than stable cash flows. |

| Timing | Are most of the cash flows near-term or far in the future? | Long-duration cash flows are more sensitive to discount-rate changes. |

| Capital structure | Is the valuation based on equity value or enterprise value? | The rate must be consistent with whether the cash flows belong to equity holders or all capital providers. |

| Terminal assumptions | How much value depends on the continuing period after the explicit forecast? | A valuation with a large terminal component can be highly sensitive to both the discount rate and the terminal growth rate. |

Simple Discount-Rate Sensitivity Example

The same cash-flow forecast can produce different valuation outputs when the discount rate changes. The example below is a simplified illustration only. It is not a real company valuation, investment recommendation, or price target.

| Discount rate | Same future cash-flow stream | Simplified present-value effect |

|---|---|---|

| 8% | Unchanged | Higher output |

| 9% | Unchanged | Lower than the 8% output |

| 10% | Unchanged | Lower than the 9% output |

The table shows the direction of sensitivity. When the cash-flow forecast stays the same, raising the discount rate reduces the present value because future cash flows are discounted more heavily. Lowering the rate has the opposite effect, which is why an unrealistically low rate can make a valuation look more attractive than the underlying risk justifies.

Matching the Discount Rate to the Cash-Flow Stream

The discount rate should match the cash flows being valued. Equity cash flows should not be discounted with a rate designed for all capital providers unless the rest of the model is built consistently. Enterprise cash flows should not be mixed with an equity-only return threshold unless the valuation is adjusted correctly.

This is where the distinction between discount rate and required rate of return matters. A required return describes the return threshold demanded by an investor or capital provider. A discount rate is the valuation input applied to the forecasted cash-flow stream. The two can overlap in practice, but they are not automatically identical in every valuation context.

The same matching rule applies to currency and inflation treatment. Nominal cash flows should normally be paired with a nominal rate. Real cash flows should normally be paired with a real rate. Mixing cash-flow definitions and discount-rate definitions can create a valuation error even when the spreadsheet mechanics look clean.

Discount Rate vs Nearby Valuation Concepts

The discount rate sits near several related valuation concepts, but it should not replace them. Keeping the boundaries clear helps avoid turning one input into a full valuation method.

| Concept | How it relates to the discount rate | Boundary to keep clear |

|---|---|---|

| WACC | WACC can be used as a discount rate for certain enterprise cash-flow models. | WACC is a specific cost-of-capital estimate, not the entire meaning of discount rate. |

| CAPM | CAPM can help estimate the cost of equity used in some valuation work. | CAPM is an input-estimation model, not a full discount-rate explanation by itself. |

| Required return | Required return can inform the rate an investor demands for taking risk. | The discount rate must still match the cash-flow stream and model perspective. |

| Terminal growth rate | The terminal growth rate affects the continuing-value assumption in a valuation. | Terminal growth changes long-term cash-flow growth; the discount rate converts those cash flows into present value. |

| DCF model | A DCF model uses a discount rate to estimate present value from expected cash flows. | DCF is the valuation method; the discount rate is one major input inside it. |

Common Mistakes and Limitations

Choosing a rate to justify a preferred valuation: The discount rate should not be reverse-engineered only to make a stock look cheap or expensive. That turns the model into a conclusion engine instead of an analytical tool.

Using one rate for every company: A stable utility, a cyclical commodity producer, and a fast-growing unprofitable business do not have the same cash-flow risk profile. A single universal rate can hide those differences.

Calling a lower rate “better”: A lower discount rate raises present value, but that does not make it more correct. The rate is only useful if it matches the risk and cash-flow stream being valued.

Treating the valuation output as a stock conclusion: A present-value estimate is an output of assumptions. It still needs business-quality review, balance-sheet analysis, scenario testing, margin of safety thinking, and evidence from the company’s actual financial statements.

Related Valuation Routes

Discount rate analysis becomes more useful when it is connected to the surrounding valuation inputs instead of treated as a standalone number.

- Cost-of-equity estimation: Use CAPM-related work when the question is how an equity return input may be estimated.

- Investor return threshold: Use required-return analysis when the question is what return an investor demands for taking risk.

- Continuing-value assumptions: Use terminal-growth analysis when the question is how the long-term cash-flow period is modeled.

FAQ

Is a discount rate the same as WACC?

Not always. WACC can be used as a discount rate for certain enterprise cash-flow valuations, but discount rate is the broader valuation concept. The correct rate depends on the cash-flow stream and valuation perspective.

Why does a higher discount rate lower valuation?

A higher discount rate places less present value on future cash flows. The cash-flow forecast may be unchanged, but the model applies a heavier adjustment for time, risk, and required return.

Can one discount rate be used for every company?

No. Different companies can have different business risk, cash-flow durability, leverage, reinvestment needs, and forecast uncertainty. A useful discount rate should reflect the specific valuation context.