Margin of safety is the gap between an estimated intrinsic value and the current market price, usually expressed as a percentage of estimated intrinsic value. It is used as a buffer against valuation error, not as proof of true value, a guaranteed floor, a price target, or an investment recommendation.

Definition: In investing, margin of safety measures how far market price sits below an estimated valuation benchmark. The concept depends on the quality of the intrinsic value estimate, because the buffer is calculated against an estimate rather than an observable fact.

Key Points About Margin of Safety

- Margin of safety compares estimated intrinsic value with market price.

- The common formula is: estimated intrinsic value minus market price, divided by estimated intrinsic value.

- The output changes when valuation assumptions change.

- A larger percentage does not automatically mean a better investment.

- Investing margin of safety is different from accounting margin of safety.

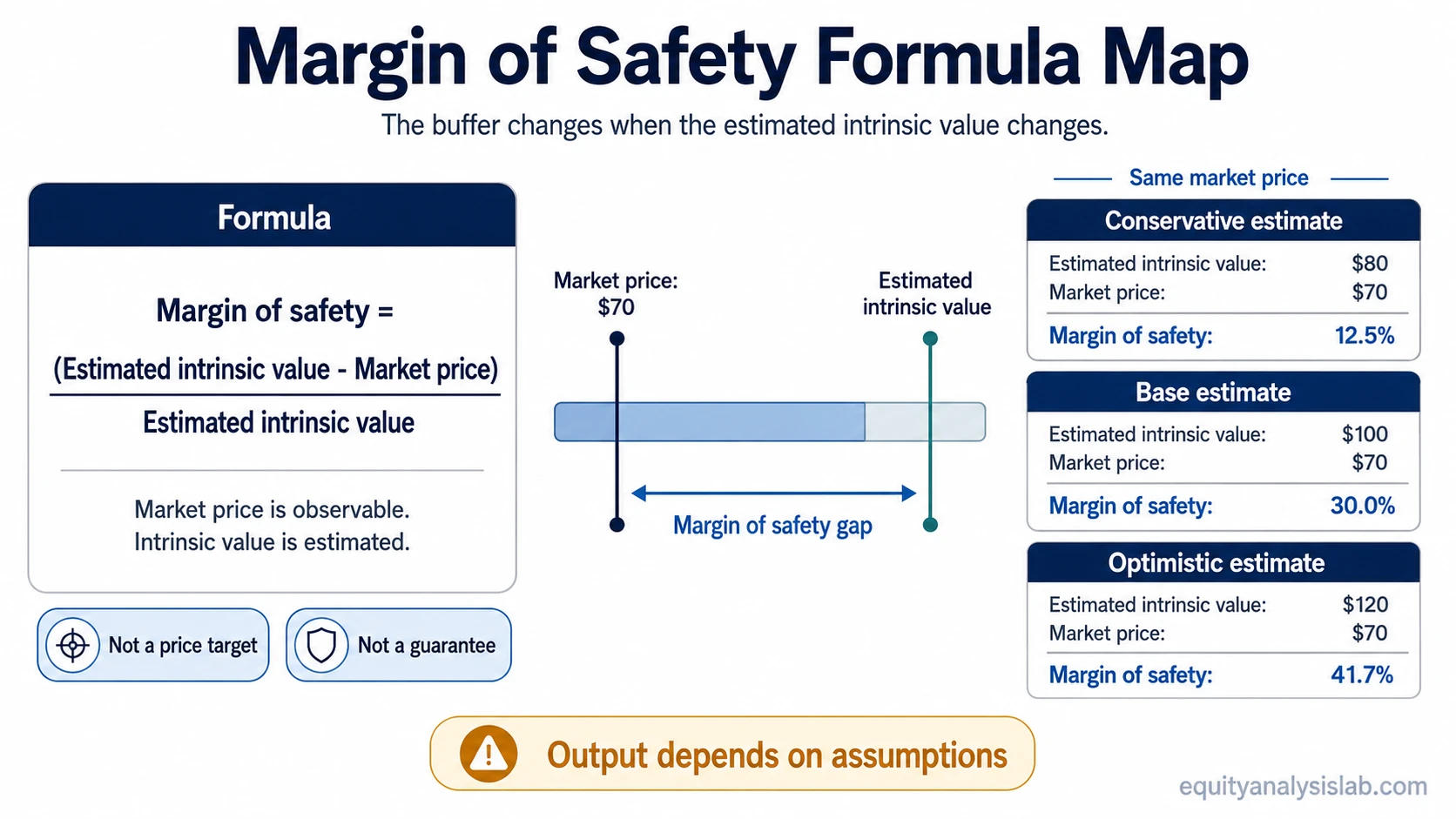

Margin of Safety Formula

The standard investing formula is:

Margin of safety = (Estimated intrinsic value – Market price) / Estimated intrinsic value

The numerator measures the estimated gap between value and price. The denominator expresses that gap as a percentage of the estimated value. If the result is positive, the market price is below the estimate. If the result is zero or negative, the market price is at or above the estimate.

The formula is only useful when the valuation estimate is built from realistic assumptions. An estimated fair value can help frame valuation risk, but it should not be treated as a guaranteed support level or a precise future trading price.

How to Calculate Margin of Safety

Assume a hypothetical company has an estimated intrinsic value of $100 per share and a current market price of $70 per share.

Illustrative calculation:

Margin of safety = ($100 – $70) / $100

Margin of safety = $30 / $100

Margin of safety = 30%

Under those assumptions, the market price is 30% below the estimated intrinsic value. The example is illustrative only and does not value a real company. A different valuation method, earnings base, discount rate, or growth assumption could produce a different result.

Why the Intrinsic Value Estimate Matters

Margin of safety is only as reliable as the valuation work behind it. Market price is observable, but estimated intrinsic value comes from assumptions. A small change in those assumptions can materially change the calculated buffer.

| Valuation input | Why it affects margin of safety |

|---|---|

| Earnings or cash-flow base | Higher or lower normalized earnings and cash flow change the starting point for valuation. |

| Growth assumption | Higher expected growth usually raises the estimate, while slower growth can reduce it. |

| Discount rate or required return | A higher required rate of return usually lowers present value estimates. |

| Terminal value or exit assumption | Long-term assumptions can drive a large part of the valuation output. |

| Balance sheet adjustments | Cash, debt, preferred claims, and other adjustments can change the value available to common shareholders. |

| Share count and dilution | A higher future share count can reduce per-share value even if business value is unchanged. |

| Valuation multiple | Multiple-based estimates depend on whether the selected multiple is realistic for the business quality, growth, and risk profile. |

The practical mistake is treating the margin as an independent safety number. The margin comes after the valuation estimate. If the estimate is too optimistic, the reported buffer may be overstated.

Margin of Safety Sensitivity Example

The same market price can produce very different margin-of-safety readings when the estimated intrinsic value changes. The same $70 market price produces different outputs under three valuation scenarios.

| Scenario | Estimated intrinsic value | Same market price | Margin of safety | Interpretation caveat |

|---|---|---|---|---|

| Conservative | $80 | $70 | 12.5% | Smaller buffer if assumptions are cautious |

| Base | $100 | $70 | 30.0% | Larger buffer under the base-case estimate |

| Optimistic | $120 | $70 | 41.7% | Larger number depends on more optimistic assumptions |

The sensitivity matters because valuation is not a single fixed truth. A stronger margin under an optimistic estimate may be less protective than a smaller margin built on conservative, cash-flow-supported assumptions.

What Margin of Safety Is Not

Margin of safety should not be read as a guarantee. It does not remove business risk, financial risk, valuation error, execution risk, or the possibility that the market price stays below estimated value for a long period.

- It is not a price target.

- It is not true value.

- It is not a guaranteed floor under the stock price.

- It is not a buy signal.

- It is not proof that downside is limited.

- It is not a replacement for business analysis.

A useful margin should be tested against business quality, earnings durability, cash flow, balance-sheet risk, dilution risk, competitive position, and the cost of capital used in the valuation work.

Margin of Safety vs Accounting Margin of Safety

Investing margin of safety compares estimated intrinsic value with market price. Accounting margin of safety compares actual or expected sales with break-even sales. The terms share a similar buffer idea, but they measure different things.

| Use case | What is compared | Main question |

|---|---|---|

| Investing | Estimated intrinsic value vs market price | How much valuation buffer exists under the estimate? |

| Accounting | Actual or expected sales vs break-even sales | How far can sales fall before break-even is reached? |

The investing usage belongs to valuation and market price interpretation. The accounting usage belongs to break-even and operating leverage analysis.

Related Valuation Concepts

Margin of safety sits inside a wider valuation framework. These related concepts help separate estimated value, market value, required return, and ownership value.

Intrinsic value, fair value, required return, and cost of capital shape the estimate; market capitalization and equity value help separate market value from shareholder value.

- Market capitalization measures the market value of common equity using share price and shares outstanding.

- Equity value describes the value attributable to common shareholders after relevant claims and adjustments.

The core distinction remains simple: market price is observable, while intrinsic value is estimated. Margin of safety is the calculated gap between the two, and the usefulness of that gap depends on the quality of the assumptions behind the estimate.

FAQ

What is margin of safety?

Margin of safety is the percentage gap between estimated intrinsic value and market price. In investing, it is used as a buffer against valuation error, but it does not guarantee protection or create an investment recommendation.

How do you calculate margin of safety?

Use the formula: estimated intrinsic value minus market price, divided by estimated intrinsic value. For example, if estimated intrinsic value is $100 and market price is $70, the margin of safety is 30%.

Is a higher margin of safety always better?

Not necessarily. A higher number may come from optimistic valuation assumptions. The margin is more useful when the valuation estimate is supported by durable earnings, cash flow, realistic discount rates, and conservative assumptions.