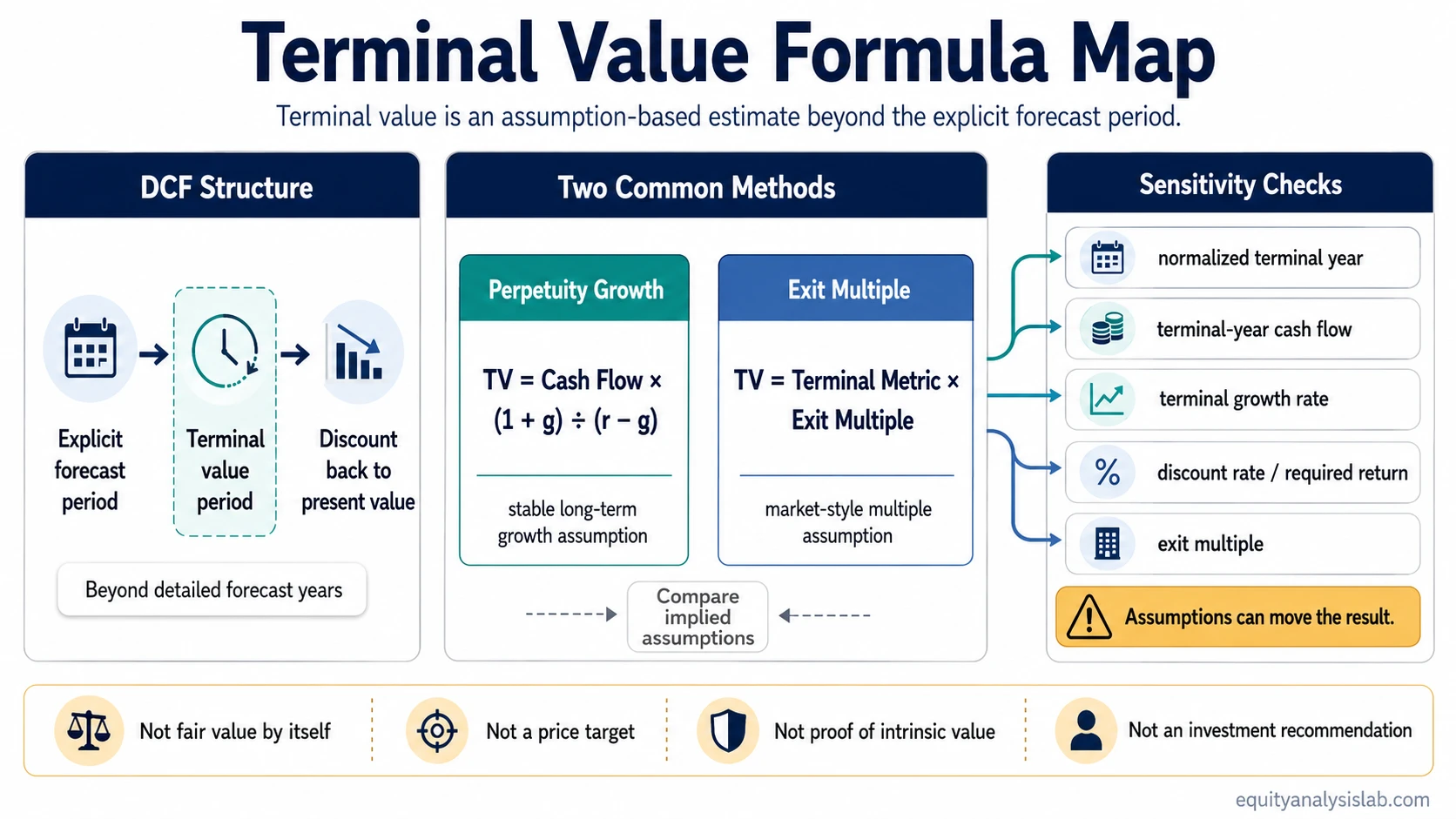

Terminal value is the estimated value assigned to a business or cash-flow stream beyond the explicit forecast period in a valuation model. It is not a guaranteed future value, a price target, or proof that a stock is worth a specific amount.

Definition: Terminal value is the part of a valuation model that estimates value after the detailed forecast years end. In a DCF model, it usually represents the value of future cash flows beyond the explicit forecast period, based on a terminal growth assumption or an exit multiple assumption.

Terminal value is an assumption-driven model output. A small change in the growth rate, discount rate, terminal-year cash flow, or exit multiple can change the valuation result materially.

Key Points

- Terminal value covers the period after the explicit forecast years in a valuation model.

- It is commonly estimated with either a perpetuity growth method or an exit multiple method.

- The result is usually discounted back to present value in a DCF model.

- Terminal value can be highly sensitive to growth, discount-rate, multiple, and terminal-year assumptions.

- Terminal value is a valuation component, not a price target, investment recommendation, or proof of fair value.

How Terminal Value Fits Into a DCF Model

A DCF model usually separates value into two parts. The explicit forecast period estimates cash flows year by year for a limited window, often a period where the analyst is willing to make detailed assumptions. Terminal value estimates what comes after that forecast window.

The terminal period matters because many businesses are valued as continuing operations, not as assets that stop producing cash flow at the end of the forecast. The model therefore needs a way to estimate value beyond the years that are forecast directly.

After terminal value is estimated, it is usually discounted back to present value along with the explicit forecast cash flows. That discounted amount may form a large part of the model output, which is why the terminal assumptions need to be checked rather than accepted mechanically.

Terminal Value Formula Methods

The two most common terminal value methods are the perpetuity growth method and the exit multiple method. They answer the same broad question in different ways: what value should be assigned to the business after the explicit forecast period?

| Method | Basic formula idea | Main assumption | Main risk |

|---|---|---|---|

| Perpetuity growth method | Terminal-year cash flow × (1 + terminal growth rate) ÷ (discount rate − terminal growth rate) | The business can grow at a sustainable long-term rate after the forecast period. | A small denominator can make the result very sensitive to growth-rate and discount-rate assumptions. |

| Exit multiple method | Terminal-year metric × selected valuation multiple | The business could be valued at a reasonable market or peer-based multiple at the end of the forecast period. | The multiple may reflect a cycle peak, peer mismatch, or market condition that does not fit the business. |

Cross-check: The two methods can challenge each other. A perpetuity growth output can be translated into an implied exit multiple, while an exit multiple output can be checked against the long-term growth assumption it would require. If one method only works under an aggressive implied assumption, the terminal value needs another reasonableness check.

Perpetuity Growth Method

The perpetuity growth method estimates terminal value by assuming that a cash-flow stream grows at a stable long-term rate after the forecast period. The basic structure is:

Terminal value = terminal-year cash flow × (1 + terminal growth rate) ÷ (discount rate − terminal growth rate)

The denominator is the critical part of the formula. When the terminal growth rate moves closer to the discount rate, the denominator becomes smaller and the terminal value can rise sharply. That does not mean the business is truly worth more. It means the model is more sensitive to the spread between those two assumptions.

A conservative terminal growth rate is often used as a reasonableness check because long-term growth cannot be separated from the size, maturity, reinvestment needs, and competitive position of the business. A mature company usually cannot justify the same terminal growth assumption as a smaller business still expanding from a low base.

Exit Multiple Method

The exit multiple method estimates terminal value by applying a valuation multiple to a terminal-year financial metric. The metric may be EBITDA, revenue, earnings, or another normalized figure, depending on the type of model and business being analyzed.

An exit multiple is not automatically more realistic than a growth assumption. It still embeds a view about market conditions, business quality, profitability, growth durability, capital intensity, and peer comparability.

The method can be useful as a cross-check because it translates terminal value into a market-style valuation lens. The weakness is that the selected multiple can import market-cycle noise into the model. A multiple based on unusually strong margins, low rates, or high investor enthusiasm may overstate the value of the terminal period.

Why Terminal Value Is Sensitive to Assumptions

Terminal value becomes fragile when the model treats one long-term assumption as if it were a precise fact. The final result can change because the terminal year is too high, the discount rate is too low, the terminal growth rate is too aggressive, or the exit multiple is not grounded in the business context.

| Assumption | How it affects terminal value | Reasonableness check |

|---|---|---|

| Terminal-year cash flow | A higher final-year cash-flow base can lift terminal value before any growth or multiple assumption is applied. | Check whether the final forecast year reflects a normalized operating level rather than a temporary peak. |

| Terminal growth rate | A higher growth assumption can increase terminal value, especially when it approaches the discount rate. | Compare the growth assumption with maturity, reinvestment needs, competitive pressure, and long-term economic limits. |

| Discount rate or required return | A lower discount rate can raise the present value of both explicit cash flows and terminal value. | Check whether the required return reflects business risk, financial risk, and uncertainty in the forecast. |

| Exit multiple | A higher selected multiple directly increases terminal value under the exit multiple method. | Compare the multiple with business quality, peer selection, margins, growth, cyclicality, and market conditions. |

| Discount period | The longer the terminal value is discounted back, the more the present value depends on the discounting assumption. | Make sure the timing of the terminal value matches the model’s forecast structure. |

A useful terminal value review asks whether the result still looks reasonable after several assumption changes. If the valuation conclusion depends on one aggressive terminal assumption, the model may be describing assumption leverage rather than business value.

Simple Terminal Value Example

A company is modeled for five explicit forecast years. The fifth year includes unusually high margins because costs were temporarily low and demand was unusually strong. If that fifth-year cash flow becomes the base for terminal value, the terminal period may inherit a temporary peak as if it were a stable long-term level.

A cleaner reading would separate the explicit forecast from a normalized terminal year. If margins, reinvestment, or working capital are unlikely to remain at the year-five level, the terminal cash-flow base should be adjusted before applying a growth formula or exit multiple.

Normalized Terminal Year Check

The terminal year should usually represent a steady-state version of the business, not merely the last number in a spreadsheet. A distorted terminal year can make both formula methods look more precise than they are.

Normalization is especially important when the final forecast year includes unusual margins, temporary tax effects, one-time working-capital movement, unsustainably low reinvestment, unusually high revenue growth, or a cyclical peak in demand.

The goal is not to make the terminal year pessimistic. The goal is to avoid capitalizing a temporary condition as if it were permanent. A terminal value built on an unrealistic base can distort the rest of the valuation model, even when the formula is applied correctly.

Terminal Value, Enterprise Value, Equity Value, and Fair Value

Terminal value is not the same thing as the full value of a company. In many DCF models, terminal value is one component of an estimated enterprise value, especially when the cash flows are measured before financing effects.

After enterprise value is estimated, additional bridge items may be needed to reach equity value. Debt, cash, preferred claims, minority interests, and other adjustments can change what common shareholders are left with.

Terminal value can support a fair value estimate, but it is not the fair value conclusion by itself. A model can produce a precise-looking number while still depending on uncertain assumptions.

Common Terminal Value Mistakes

Treating terminal value as true value: Terminal value is an estimate created by a model. It should not be treated as the actual future value of the business.

Using aggressive growth assumptions: A terminal growth rate that is too close to the discount rate can create a large output from a small assumption change.

Ignoring discount-rate sensitivity: A lower required return can lift present value, but the lower rate must be justified by the risk of the business and the uncertainty of the forecast.

Applying a market multiple without context: A multiple taken from peers or recent deals may not fit the company’s growth, margins, reinvestment needs, leverage, or cycle position.

Reading a high terminal value as an investment conclusion: A large terminal value may reflect assumptions rather than a clear valuation edge. The model still needs a reasonableness check.

Related Valuation Concepts

Enterprise value: Enterprise value helps connect terminal value to the value of the operating business before equity-specific adjustments.

Equity value: Equity value helps separate operating-business value from the amount attributable to common shareholders after claims and balance-sheet adjustments.

Fair value: Fair value is the broader valuation estimate that may use terminal value as one input, not as a standalone conclusion.

Exit multiple: Exit multiple is one common way to estimate terminal value by applying a valuation multiple to a terminal-year metric.

FAQ

What is terminal value in a DCF model?

Terminal value is the estimated value of cash flows beyond the explicit forecast period in a DCF model. It is usually calculated with a perpetuity growth method or an exit multiple method, then discounted back to present value.

Why can terminal value dominate a DCF model?

Terminal value can become large because it represents cash flows after the detailed forecast period. The effect becomes stronger when the model assumes durable cash flow, long-term growth, a low discount rate, or a high exit multiple.

Is terminal value the same as fair value?

No. Terminal value is one component inside a valuation model. Fair value is a broader estimate that may include explicit forecast cash flows, terminal value, balance-sheet adjustments, and other valuation assumptions.

Which terminal value method is better?

Neither method is automatically better. The perpetuity growth method depends heavily on long-term growth and discount-rate assumptions, while the exit multiple method depends heavily on the selected multiple and market context.