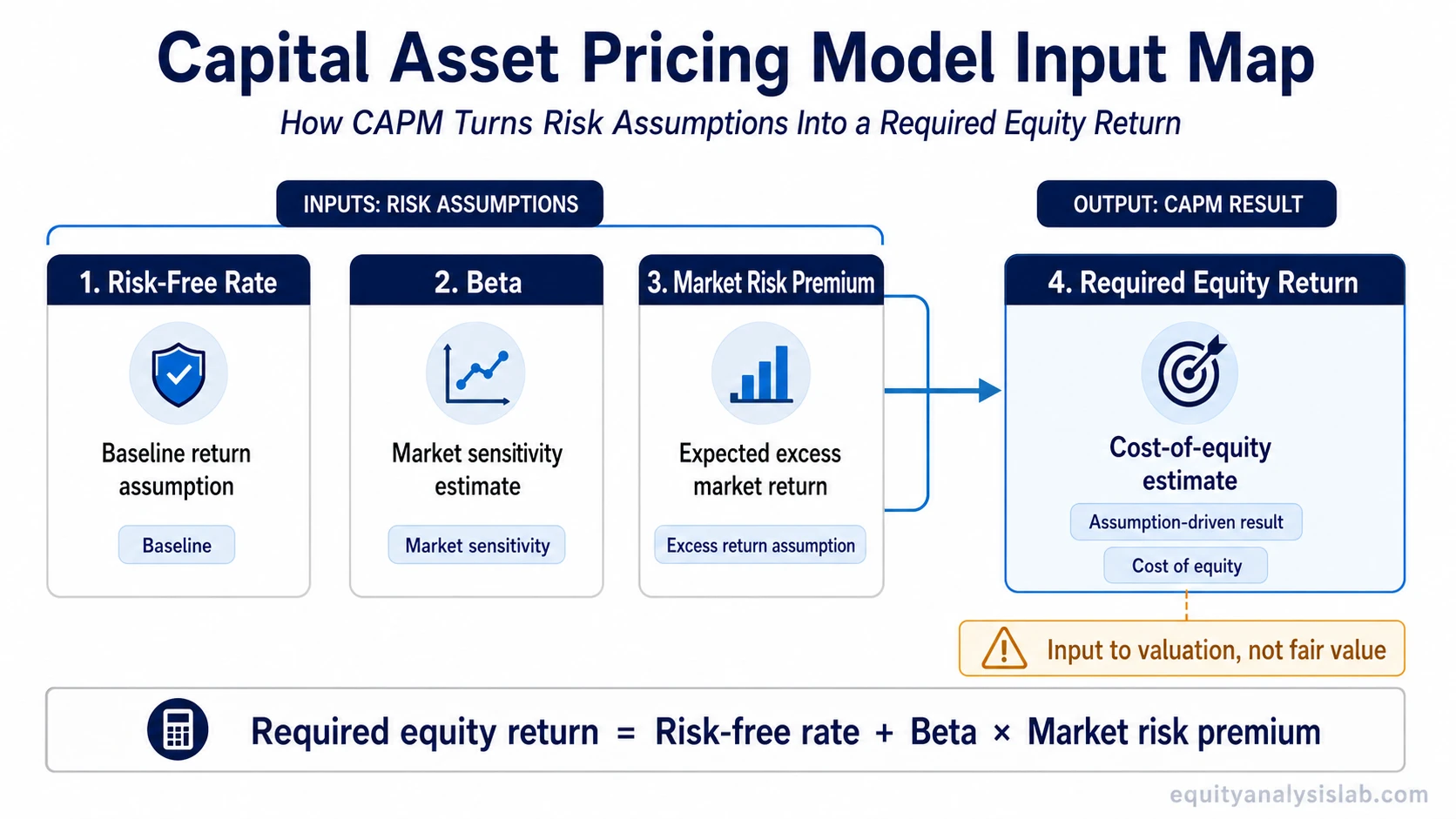

The capital asset pricing model (CAPM) estimates the required return on equity by linking systematic market risk to the risk-free rate, beta, and the market risk premium.

In valuation work, the result is usually used as a cost-of-equity input or discount-rate component, not as proof that a stock is fairly valued. The model is useful because it can force the analyst to separate the return required for bearing equity risk from the valuation conclusion that may come later.

Definition: The capital asset pricing model is an asset pricing model that estimates required equity return from systematic risk. It does not measure all business risk, forecast realized return, or calculate intrinsic value by itself.

Key Points

- CAPM estimates required return on equity from the risk-free rate, beta, and the market risk premium.

- The output is often used as a cost-of-equity estimate in valuation work.

- The model is sensitive to input choices, especially beta, the market proxy, and the market risk premium.

- A precise CAPM result should be treated as an assumption-driven input, not as a final valuation answer.

What Is the Capital Asset Pricing Model?

The capital asset pricing model connects expected equity return to systematic market risk. The basic idea is that an investor should require more return from an equity investment when that investment is more sensitive to broad market movement.

The model focuses on systematic risk because that risk cannot be removed simply by holding more companies in a diversified portfolio. In CAPM, beta is the input used to represent that market sensitivity.

For company analysis, CAPM is usually not the end of the valuation process. It is one way to estimate the return required by equity investors before that rate is used inside a broader valuation model or compared with other required-return assumptions.

Capital Asset Pricing Model Formula

The standard CAPM formula is:

Required return on equity = Risk-free rate + Beta × (Expected market return − Risk-free rate)

The term in parentheses is the market risk premium. It represents the expected excess return of the selected market portfolio or proxy above the risk-free rate. In many valuation models, the CAPM result is then used as a cost-of-equity estimate or as part of an equity discount-rate assumption.

| Formula item | Meaning | Valuation role |

|---|---|---|

| Risk-free rate | Baseline return assumption before equity risk is added | Sets the starting point for required return |

| Beta | Estimate of sensitivity to broad market movement | Adjusts required return for systematic risk |

| Expected market return | Expected return from the selected market portfolio or proxy | Defines the market-return assumption used to estimate the market risk premium |

| Market risk premium | Expected market return minus the risk-free rate | Measures the extra return assumed for bearing equity-market risk |

CAPM Inputs and Assumptions

CAPM looks simple because the formula has only a few variables. The hard part is that each variable contains an assumption. A different risk-free rate, beta period, market index, or market risk premium can change the output even when the company being analyzed has not changed.

| CAPM input | What it changes | Why it can be fragile |

|---|---|---|

| Risk-free rate | Baseline required return | Changes with rates, currency, and horizon choice |

| Beta | Systematic risk adjustment | Often backward-looking and unstable across measurement windows |

| Market risk premium | Excess return assumption | No single estimate is universally correct |

| Equity return output | Cost-of-equity estimate | Input to valuation, not a valuation conclusion |

This is why CAPM is best read as an assumption framework. It can make the required-return logic explicit, but it cannot remove uncertainty from the valuation process.

How CAPM Fits Into Valuation

CAPM is closely related to cost of capital, but the two concepts are not identical. CAPM estimates the cost of equity. Cost of capital is broader because it may also include debt financing and capital structure.

CAPM can also feed an equity discount-rate input. That does not mean the model calculates the value of the business. It only helps define one required-return assumption that may be used in a valuation framework.

Investor-use boundary: A lower CAPM output does not prove that a stock is attractive, and a higher CAPM output does not prove that a stock is unattractive. The result must still be compared with cash-flow assumptions, business quality, balance-sheet risk, growth durability, and valuation uncertainty.

Example CAPM Calculation

Consider a purely illustrative setup with a 4% risk-free rate, a beta of 1.2, and an expected market return of 9%.

Step 1: Market risk premium = 9% − 4% = 5%.

Step 2: Required return on equity = 4% + 1.2 × 5% = 10%.

In this example, CAPM produces a 10% required equity return. That number should be read as an assumption-driven cost-of-equity estimate. It is not a prediction that the stock will return 10%, and it does not prove that any specific company is fairly valued.

| Changed assumption | Illustrative CAPM output | What changed |

|---|---|---|

| Base case: 4% risk-free rate, 1.2 beta, 9% expected market return | 10.0% | Baseline illustrative estimate |

| Beta rises to 1.5 | 11.5% | Higher systematic risk assumption raises required return |

| Expected market return rises to 10% | 11.2% | Higher market return assumption raises the market risk premium |

The calculation shows why small input changes can move the output. The model looks exact, but the result depends on assumptions that remain open to judgment.

CAPM Limitations

CAPM is useful because it gives structure to required-return thinking. Its main weakness is that the structure can look more precise than the underlying assumptions deserve.

Beta limitation: Beta is usually estimated from historical price behavior. A company’s future risk can change if its business mix, leverage, industry exposure, or market environment changes. Beta can also miss company-specific risk even when it captures broad market sensitivity.

Market proxy limitation: The expected market return depends on which market proxy is used. Different indexes can produce different assumptions.

Market risk premium limitation: There is no universally agreed market risk premium. Historical averages, forward estimates, and analyst assumptions can differ materially.

Valuation limitation: CAPM does not estimate cash flows, margins, reinvestment needs, terminal value, or competitive position. Those still require separate company analysis.

A common mistake is to treat the CAPM output as a final hurdle rate that settles the investment question. A better use is to test whether the required-return assumption is reasonable, sensitive, and consistent with the rest of the valuation work.

CAPM vs Related Valuation Concepts

CAPM sits near several valuation terms, but it should not absorb their roles. The clean distinction is that CAPM estimates a required return on equity, while other concepts answer broader valuation or capital-structure questions.

| Related concept | How it differs from CAPM |

|---|---|

| Cost of capital | Broader required-return concept; CAPM is one model for estimating the equity portion. |

| Discount rate | Broader valuation input; CAPM may help estimate an equity discount rate. |

| Enterprise value | Measures firm operating value; CAPM does not calculate firm value by itself. |

| Intrinsic value | A valuation conclusion or framework; CAPM may influence one discount-rate assumption inside that work. |

| Fair value | A broader value estimate; CAPM can support an assumption but does not prove fair value. |

FAQ

What is the CAPM formula?

The CAPM formula is required return on equity = risk-free rate + beta × (expected market return − risk-free rate).

Does CAPM calculate fair value?

No. CAPM can help estimate a required return or cost of equity, but it does not calculate fair value by itself. Cash-flow assumptions, business quality, growth, and valuation method still matter.

Why can CAPM be unreliable?

CAPM can be fragile because beta, the market proxy, the risk-free rate, and the market risk premium are all assumptions. A small change in those inputs can change the required-return estimate.