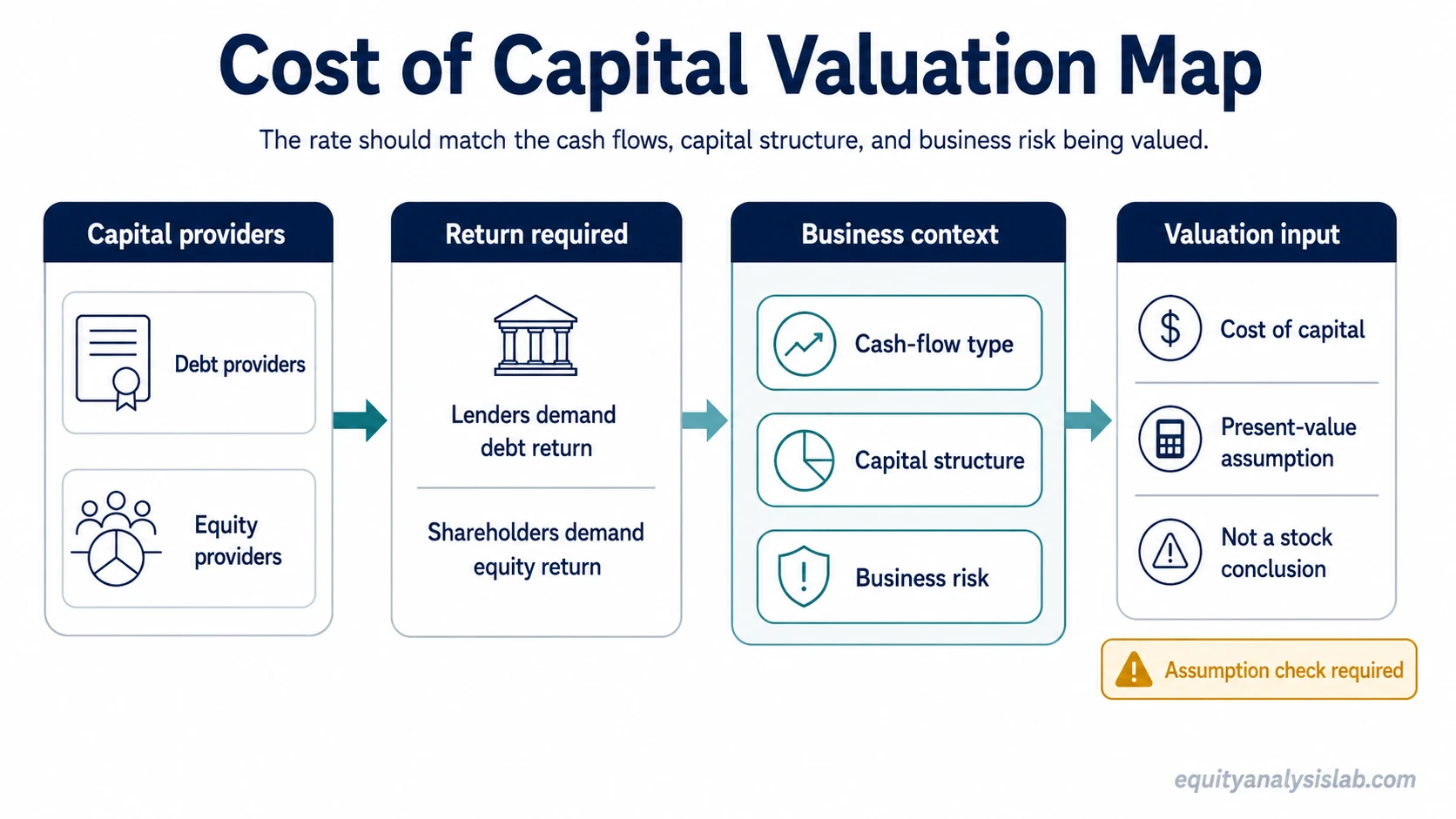

Cost of capital is the return a company’s debt and equity providers demand for supplying funding. In valuation, it is often used as a hurdle rate or present-value input for judging whether expected future cash flows are being discounted with enough regard for risk.

Definition: Cost of capital is the required return attached to the money a business uses to fund its assets, operations, acquisitions, and growth. For investors, the estimate matters because a higher rate reduces the present value of future cash flows, while a lower rate increases it, all else equal.

Key points

- Cost of capital combines the return demanded by lenders and shareholders.

- The blended version is often expressed through WACC, but cost of capital is not always identical to one formula.

- Valuation use depends on matching the rate to the cash flows being valued.

- A precise-looking percentage can still be fragile if the cash-flow forecast, business risk, or capital structure changes.

What cost of capital means

A company usually receives capital from two broad groups: lenders and equity owners. Lenders expect interest and principal protection. Equity owners accept more uncertainty and usually demand a higher expected return because they are paid after creditors.

Cost of capital converts those return expectations into a rate that can be compared with expected business returns. If a company invests in a project, acquisition, or operating asset, the return from that use of capital must be judged against the return capital providers expect for taking the risk.

For equity investors, cost of capital is not a stock rating by itself. It is an assumption inside valuation. The same business can look more or less valuable depending on the rate used, the durability of cash flows, the balance-sheet structure, and the risk built into the forecast.

How cost of capital works in valuation

Valuation uses cost of capital by connecting risk to present value. Future cash flows are worth less than current cash flows because investors require compensation for time, uncertainty, and opportunity cost. A discount rate applies that return threshold to future cash flows.

The rate should match the cash-flow stream. Cash flows available to all capital providers are usually paired with a blended firm-level rate. Cash flows available only to common shareholders are usually paired with an equity return threshold. A mismatch can make the valuation look mathematically clean while the economic comparison is wrong.

| Valuation input | What it should match | Why the match matters |

|---|---|---|

| Firm cash flows | Capital available to both debt and equity providers | The rate should reflect the blended risk of financing the whole business. |

| Equity cash flows | Cash flows left for common shareholders | The rate should reflect equity risk rather than total capital risk. |

| Project cash flows | The specific risk of the project or asset | A company-wide rate can understate or overstate risk when the project differs from the existing business. |

Cost of capital formula and main components

The common blended expression is weighted average cost of capital, or WACC. In simplified form, WACC weights the cost of equity and the after-tax cost of debt by their share of total capital.

Simplified WACC expression: WACC = (equity weight × cost of equity) + (debt weight × after-tax cost of debt).

| Component | Meaning | Investor interpretation |

|---|---|---|

| Cost of debt | The return lenders demand for providing debt capital. | Usually influenced by credit risk, interest-rate conditions, debt maturity, and the company’s ability to service obligations. |

| Cost of equity | The return shareholders demand for owning the residual claim on the business. | Often estimated with models such as the capital asset pricing model, but the model output still depends on assumptions. |

| Capital weights | The relative mix of debt and equity in the capital structure. | A business with more leverage may have a different blended risk profile than a business funded mostly by equity. |

| Tax treatment of debt | Interest expense may reduce taxable income in many settings. | The tax adjustment should not be copied mechanically without checking the actual valuation context. |

The formula is useful only when the inputs describe the business being valued. A stale cost of debt, an unrealistic cost of equity, or capital weights that no longer match the company can make the final percentage misleading.

Cost of capital is not the same as every related term

Cost of capital sits near several valuation concepts, but each one answers a different question. Keeping the boundaries clear helps prevent a single rate from being treated as a complete valuation verdict.

| Concept | What it means | What it is not |

|---|---|---|

| Cost of capital | The required return attached to the capital used by a business. | Not a final decision on whether a stock is attractive. |

| WACC | A blended estimate of debt and equity capital costs. | Not always the right rate for every cash-flow stream. |

| Discount rate | The rate used to convert future cash flows into present value. | Not always a company-wide capital cost if the cash flows have a different risk profile. |

| Required return | The return threshold an investor or capital provider demands. | Not automatically the same for every investor, asset, or business risk. |

| Cost of equity | The shareholder return threshold on equity capital. | Not the full capital cost when debt is also part of the financing structure. |

The assumption stack behind cost of capital

A cost-of-capital estimate can look like one number, but it usually sits on top of several assumptions. The rate becomes more useful when those assumptions are checked against the cash-flow forecast and the business risk being valued.

| Assumption area | Question to test | Risk if ignored |

|---|---|---|

| Cash-flow quality | Are the projected cash flows recurring, cash-backed, and supported by the business model? | A low rate can overstate value if the cash-flow forecast is weak. |

| Growth durability | Can the business sustain growth without requiring excessive reinvestment or dilution? | The valuation may depend on growth that the business cannot fund efficiently. |

| Risk-free rate | Does the base rate reflect the currency and time horizon of the cash flows? | The discount rate may mix mismatched markets or maturities. |

| Equity risk premium | Does the equity premium reflect the uncertainty shareholders are taking? | The cost of equity may look precise while understating residual risk. |

| Business sensitivity | How exposed are margins, revenue, and cash flows to cyclicality or competition? | A stable-looking rate can become stale when forward risk changes. |

| Debt cost | Can the company refinance debt at similar terms? | Old interest costs may not reflect current financing risk. |

| Capital structure | Are debt and equity weights based on the structure being valued? | The blended rate may not match the business after leverage changes. |

| Terminal value | How much of the valuation depends on long-term assumptions? | Small rate changes can dominate the estimate when terminal value is large. |

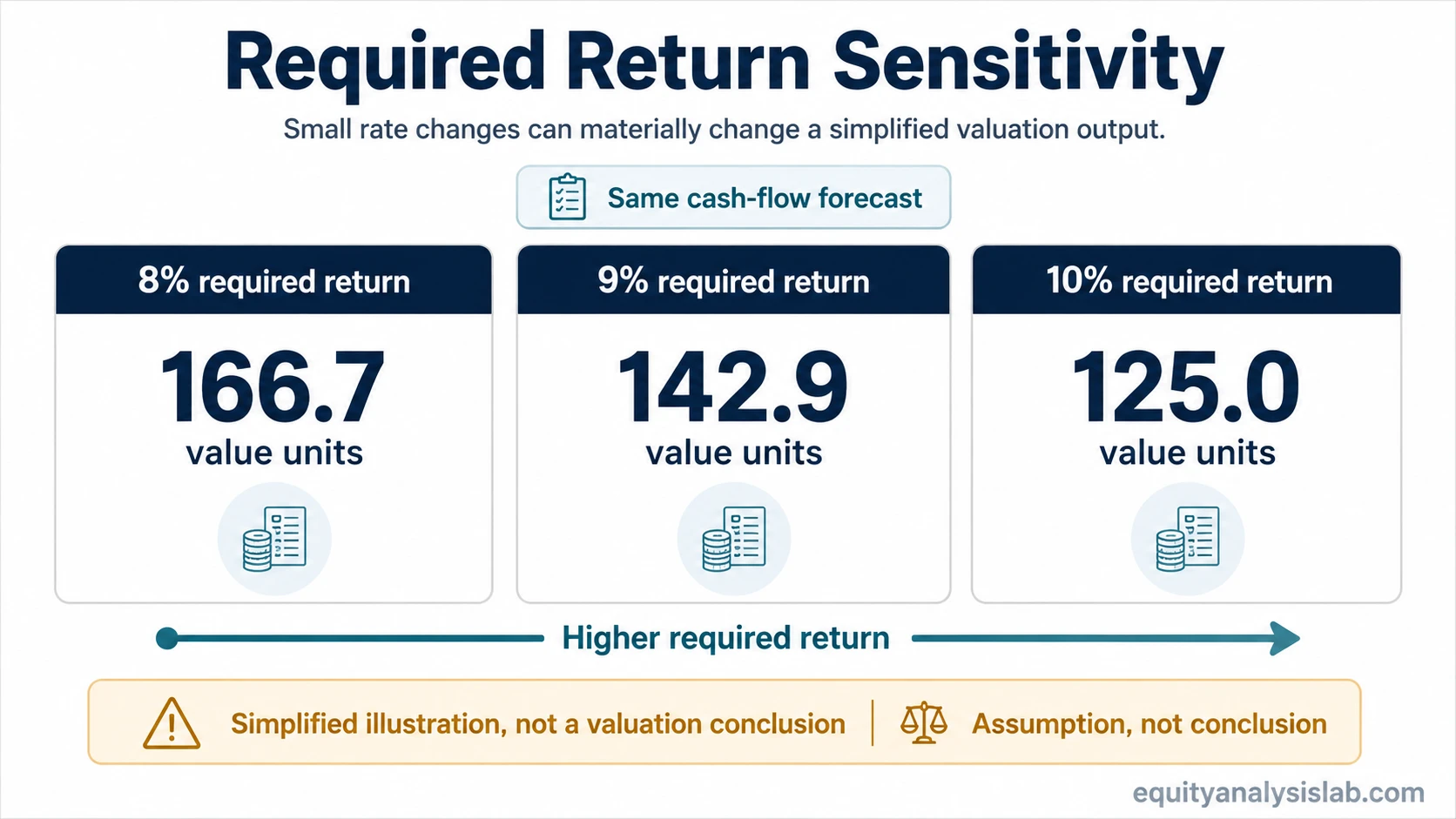

Why small rate changes can change valuation interpretation

Cost of capital is powerful because it affects the present value of many future cash flows at once. The effect is especially large when a valuation depends heavily on long-duration cash flows or terminal value.

Hypothetical example: Assume a business is expected to produce 10 units of free cash flow next year and grow at 2% in a stable perpetuity-style model. At an 8% required return, the simplified value is 166.7 units. At 9%, it falls to 142.9 units. At 10%, it falls to 125.0 units. The business forecast did not change, but the rate changed the valuation output materially.

| Assumed required return | Growth assumption | Simplified value using cash flow / (rate – growth) | Interpretation boundary |

|---|---|---|---|

| 8% | 2% | 166.7 | Lower required return gives more value to future cash flows. |

| 9% | 2% | 142.9 | A one-point increase reduces the valuation output. |

| 10% | 2% | 125.0 | The same cash-flow forecast can support a much lower estimate. |

The example is only a simplified illustration. Real valuation work also has to consider reinvestment needs, cyclicality, leverage, margin durability, competitive pressure, and whether the cash-flow forecast is realistic.

How cost of capital connects with enterprise value

Firm-level valuation often focuses on the value of the operating business before separating claims between debt and equity holders. That is why cost of capital often appears beside enterprise value, free cash flow to the firm, and capital-structure analysis.

The link is practical: a firm-level cash-flow forecast needs a firm-level required return. After the business value is estimated, debt, cash, and other claims affect what may be left for common equity. A low cost of capital does not remove the need to analyze the balance sheet.

Common mistakes when using cost of capital

- Using one rate for every situation: A mature regulated utility, a cyclical manufacturer, and a high-growth software company may not deserve the same required return.

- Treating WACC as a universal discount rate: WACC can be useful for firm-level cash flows, but it can be the wrong rate for equity-only cash flows or project cash flows with different risk.

- Ignoring cash-flow quality: A lower rate cannot fix a forecast built on weak margins, aggressive growth, or poor conversion of earnings into cash.

- Using stale financing inputs: Debt cost, leverage, refinancing risk, and market rates can change faster than a model template.

- Letting terminal value carry the whole model: When most of the estimate comes from terminal value, small changes in the required return can dominate the result.

- Turning the rate into a stock conclusion: Cost of capital supports valuation judgment, but it does not prove that a stock should be bought, sold, or avoided.

When the estimate becomes less reliable

Cost of capital becomes less reliable when the risk of the business changes faster than the model inputs. A company may look stable based on past financing costs while forward risk is rising through weaker demand, margin pressure, leverage, refinancing needs, or lower cash-flow visibility.

The estimate also weakens when the rate is chosen to justify a preferred valuation outcome. A sound valuation process starts with the business, cash-flow durability, balance-sheet risk, and capital-provider return requirements, then tests how sensitive the result is to reasonable alternatives.

Limitation: Cost of capital is an assumption, not an observed fact. It can organize valuation thinking, but it cannot remove uncertainty from the cash-flow forecast or guarantee that market price will move toward a modeled value.

Related valuation concepts

Cost of capital becomes clearer when it is separated from the mechanics around it. Discount-rate analysis explains how future cash flows are converted into present value. CAPM is one common way to estimate the equity portion of the required return. Enterprise value helps connect firm-level valuation with debt, cash, and equity claims.

The source endpoint for this topic remains cost of capital itself: WACC, CAPM, discount rate, and enterprise value support the estimate, but none of them replaces the broader question of what return the company’s capital providers demand for the risk being valued.

FAQ

Is cost of capital the same as WACC?

Not always. WACC is a common blended estimate of cost of capital that weights debt and equity. Cost of capital is the broader idea of the return demanded by capital providers, and the right expression depends on the cash flows being valued.

Why does cost of capital matter in valuation?

Cost of capital matters because it affects how future cash flows are converted into present value. A higher rate lowers the value assigned to future cash flows, while a lower rate raises it, assuming the forecast is unchanged.

Can cost of capital prove that a stock is undervalued?

No. Cost of capital is one valuation assumption. A stock conclusion also depends on cash-flow quality, growth durability, balance-sheet risk, current price, uncertainty, and the margin between estimate and market value.

What makes a cost-of-capital estimate unreliable?

The estimate becomes unreliable when inputs are stale, capital structure changes, business risk changes, or the cash-flow forecast is weak. A precise percentage does not make the valuation precise if the assumptions underneath it are unstable.