Enterprise value is a capital-structure-adjusted measure of company value. It starts with market capitalization, then adjusts for debt-like claims, preferred stock, minority interest, and cash to estimate the value of the operating business before separating financing choices from business scale.

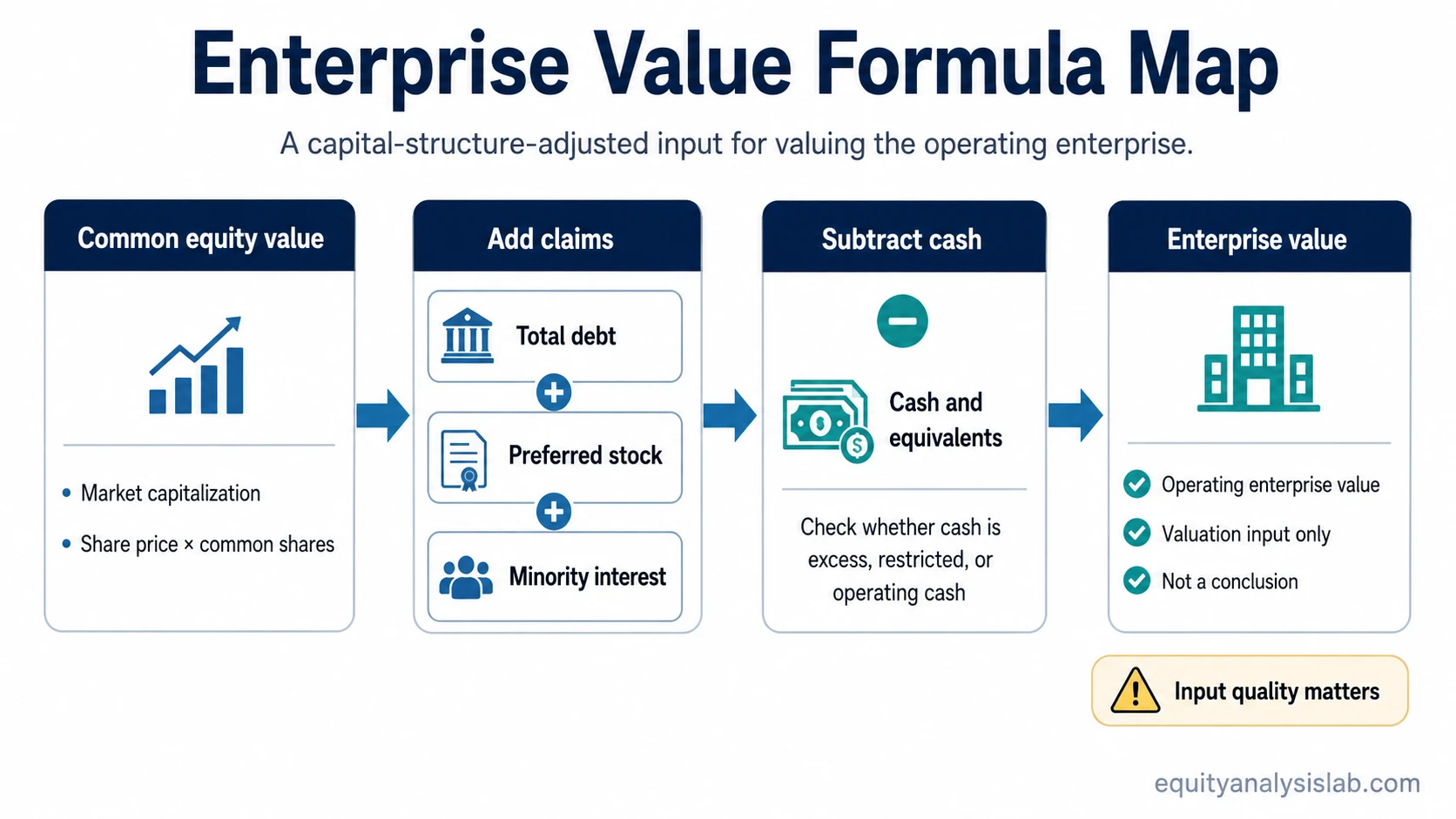

Definition: Enterprise value, often shortened to EV, measures the total value of a company’s operating enterprise by combining the value of common equity with other capital claims and subtracting cash and cash equivalents. It is a valuation input, not a fair value estimate, stock conclusion, or investment recommendation by itself.

EV is useful because two companies with similar market capitalizations can have very different balance sheets. A highly levered company and a cash-rich company may look similar through equity value alone, but enterprise value changes the comparison by bringing financing structure into the analysis.

Key Points

- Enterprise value adjusts market capitalization for debt, cash, preferred stock, minority interest, and other capital claims.

- EV can help compare companies with different capital structures, especially when paired with operating metrics such as revenue, EBITDA, EBIT, or free cash flow.

- The number can become misleading when debt values, cash classification, minority interests, or sector capital intensity are not interpreted carefully.

What Is Enterprise Value?

Enterprise value represents the value of the operating company from the perspective of all capital providers, not only common shareholders. Market capitalization looks only at common equity. Enterprise value adds debt-like claims and subtracts cash-like resources because a buyer, lender, or valuation analyst usually needs to understand the whole capital stack.

The practical distinction is that EV tries to answer a different question than a share price or market cap. It asks what the operating enterprise is being valued at after considering claims that sit above or beside common equity. That makes it especially useful when comparing companies that fund similar businesses in different ways.

Enterprise Value Formula

Formula: Enterprise value = market capitalization + total debt + preferred stock + minority interest – cash and cash equivalents.

The formula is simple, but the interpretation is not automatic. Each input changes what the EV number means. Debt increases EV because debt holders have a claim on the enterprise. Cash reduces EV because cash can offset part of the cost of acquiring or valuing the operating business, depending on whether the cash is truly excess or needed for operations.

What Each Enterprise Value Component Means

Enterprise value is strongest when each component is treated as a valuation assumption rather than a mechanical spreadsheet line. The same formula can produce a less useful result if the inputs are stale, incomplete, or mismatched to the company’s capital structure.

| Formula component | How it affects EV | Why it matters for valuation |

|---|---|---|

| Market capitalization | Added as the market value of common equity. | It anchors EV to the current market value of common shareholders’ claim, but it can move quickly with the share price. |

| Total debt | Added because debt holders have a claim on the enterprise. | Debt changes the value available to equity holders and affects comparison quality across companies with different leverage. |

| Preferred stock | Added when preferred shares represent a claim senior to common equity. | Preferred stock can make equity-only comparisons incomplete because it sits outside common market capitalization. |

| Minority interest | Added when consolidated financials include subsidiaries not fully owned by common shareholders. | It helps align enterprise value with the operating metrics that include the subsidiary’s results. |

| Cash and cash equivalents | Subtracted because cash can offset part of the enterprise purchase or valuation burden. | The key judgment is whether cash is excess, restricted, or needed to run the business. |

Simple Enterprise Value Calculation Example

Simplified hypothetical example: A company has a market capitalization of $900 million, total debt of $250 million, preferred stock of $50 million, minority interest of $25 million, and cash and equivalents of $175 million.

Enterprise value: $900 million + $250 million + $50 million + $25 million – $175 million = $1.05 billion.

The $1.05 billion result does not mean the company is cheap, expensive, fairly valued, or likely to be acquired. It only gives a capital-structure-adjusted value that can be compared with operating measures when the inputs and business context are appropriate.

Why Enterprise Value Is Used in Valuation

Enterprise value is commonly used when the valuation question concerns the whole operating business rather than only common equity. That is why EV often appears in valuation multiples such as EV/revenue, EV/EBITDA, EV/EBIT, and EV/free cash flow.

EV can improve comparison quality when companies use different mixes of debt and equity. A company with more debt may have a lower market capitalization than a less levered peer, but that does not necessarily mean the operating enterprise is cheaper. Enterprise value brings the debt claim into the comparison.

The multiple is only as useful as the match between EV in the numerator and the operating measure in the denominator. A mismatch between enterprise value and the metric being compared can make a valuation multiple look cleaner than the analysis really is.

EV can also be useful in acquisition-style thinking because a buyer would normally consider cash, debt, preferred stock, and other claims alongside the equity purchase price. That does not mean EV predicts an acquisition outcome. It only explains why the whole capital stack matters when valuing the operating business.

Enterprise Value vs Market Cap and Equity Value

Enterprise value: Measures the value of the operating enterprise after adjusting common equity value for debt-like and cash-like items.

Market capitalization: Measures only the market value of common equity, calculated as share price multiplied by common shares outstanding.

Equity value: Focuses on the value attributable to shareholders after considering the claims that sit ahead of common equity.

The concepts overlap, but they should not be used interchangeably. Market cap is an equity-market measure. Enterprise value is a whole-enterprise valuation input. Equity value is the shareholder-focused result that becomes especially important when moving from enterprise valuation to per-share interpretation.

Enterprise Value Assumption Stack

Enterprise value can look precise because the formula produces a clean number. The quality of that number depends on assumptions behind the inputs. A small classification difference can change both EV and the valuation multiple built from it.

| Input or assumption | Why it matters | How it can distort interpretation |

|---|---|---|

| Debt value | Debt is added to EV because lenders have a claim on the enterprise. | Book debt and market value of debt may not tell the same story when rates, credit quality, or refinancing risk change. |

| Excess vs operating cash | Cash is subtracted only when it can reasonably offset enterprise value. | Subtracting cash that is needed for daily operations can make EV look too low. |

| Preferred stock or minority interest | These claims help align EV with consolidated operating measures. | Ignoring them can make EV multiples look cleaner than the real capital structure allows. |

| Sector capital intensity | Some industries require more debt, working capital, leases, or reinvestment than others. | A low EV multiple may reflect business structure or reinvestment burden rather than undervaluation. |

| Market capitalization date | Market cap changes as the share price changes. | Mixing a current market cap with stale debt, cash, or share-count data can create a mismatched EV estimate. |

When Enterprise Value Can Mislead

Input quality risk: EV becomes less reliable when debt, cash, preferred stock, minority interest, or share count data are stale or incomplete.

Cash classification risk: Cash may be excess, restricted, seasonal, or needed for operations. Treating all cash as freely available can overstate the usefulness of the subtraction.

Debt interpretation risk: Debt can differ in maturity, interest rate, refinancing exposure, covenant pressure, and market value. A simple debt add-back does not explain those risks by itself.

Sector comparison risk: EV multiples can differ across industries because capital intensity, margins, growth, reinvestment needs, and accounting conventions differ.

Multiple misuse risk: A low EV multiple does not automatically prove value. A high EV multiple does not automatically prove overvaluation.

How Enterprise Value Fits Into Investor Analysis

Enterprise value is best used as an input in a broader valuation process. It can help frame what the market is assigning to the operating business, but it does not replace analysis of cash flow, margins, growth durability, balance-sheet risk, reinvestment needs, or competitive position.

EV also should not be confused with fair value. Fair value requires an analytical framework for what a business or security is reasonably worth under stated assumptions. EV supplies one capital-structure-adjusted value measure that may feed into that work.

The same boundary applies to intrinsic value estimates. Intrinsic value depends on expected future cash flows, required return, growth assumptions, and risk. Enterprise value can support the analysis, but it is not the conclusion.

Related Valuation Concepts

Enterprise value connects most directly to shareholder value, operating-value multiples, and model-based valuation work. The most important adjacent concepts are equity value, fair value, and intrinsic value because each one answers a different valuation question.

| Concept | Primary question | Relationship to enterprise value |

|---|---|---|

| Equity value | What value belongs to common shareholders? | Equity value is the shareholder-focused side of the capital structure distinction. |

| Fair value | What is a reasonable value under a stated analytical framework? | EV may be one input, but fair value requires assumptions and judgment beyond the EV formula. |

| Intrinsic value | What is the business worth based on expected future economics? | Intrinsic value analysis may use EV-related outputs, but it depends on forecasts and discount-rate assumptions. |

FAQ

What does enterprise value include?

Enterprise value includes market capitalization, total debt, preferred stock, and minority interest, then subtracts cash and cash equivalents.

Is enterprise value the same as market capitalization?

No. Market capitalization measures the value of common equity only. Enterprise value adjusts that equity value for debt-like and cash-like items to estimate the value of the operating enterprise.

Does enterprise value show whether a stock is cheap?

No. Enterprise value is a valuation input. It must be interpreted with earnings quality, cash flow, growth, risk, balance-sheet structure, and the valuation method being used.