Equity value is the value attributable to common shareholders in a company valuation after the business value is connected to share count, capital structure, and other claims.

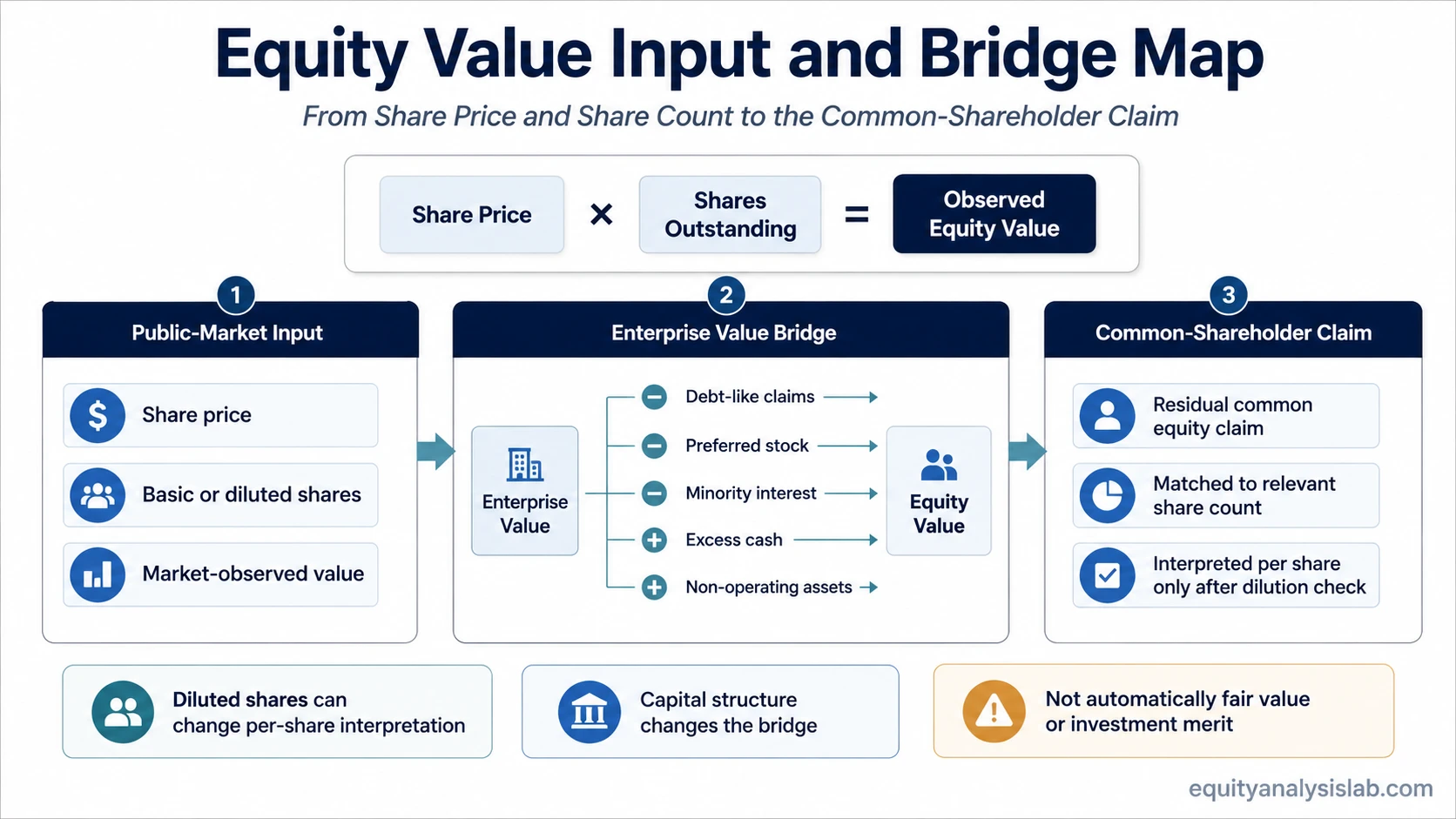

Definition: Equity value represents the common-shareholder claim on a company. In public markets, it is often observed as share price multiplied by shares outstanding. In valuation work, it can also be derived from enterprise value after adjusting for debt-like claims, preferred stock, minority interest, cash, and non-operating assets where relevant.

The simplest public-market expression is share price × shares outstanding, while valuation work may derive equity value from enterprise value after capital-structure adjustments.

The shareholder-claim framing separates the common equity layer from the full operating business value available to all capital providers. That distinction matters when a company has meaningful debt, excess cash, preferred stock, minority interest, or potential dilution.

Equity value can look like a single number, but the number depends on the inputs behind it. Share count, dilution, net debt, cash, valuation multiples, DCF assumptions, and per-share interpretation can all change the result.

Key Points

- Equity value is the common-shareholder claim in a company valuation.

- The public-market formula is usually share price × shares outstanding.

- Diluted shares often give a more conservative view than basic shares when options, RSUs, convertibles, or other dilutive securities are relevant.

- Equity value can also be derived from enterprise value through capital-structure adjustments.

- Equity value is not automatically fair value, intrinsic value, target price, or proof that a stock is attractive.

What Equity Value Means

Equity value measures the value linked to common shareholders rather than the value of the whole operating business. It answers a narrower question: after considering the company’s capital structure and other claims, what value belongs to the common equity layer?

That shareholder-claim framing separates equity value from total firm value. A company can have a high operating business value and still have a much lower common equity claim if debt-like obligations or other senior claims are large. A company with large excess cash can show the opposite effect when the bridge from business value to equity value is adjusted carefully.

For public companies, the observable version of equity value is close to market capitalization when the calculation uses the current share price and the relevant share count. In valuation analysis, the estimated version may differ because the analyst is using model assumptions rather than only the latest traded price.

Equity Value Formula

The simplest public-market formula is:

Equity value = share price × shares outstanding

If a company trades at $40 per share and has 100 million shares outstanding, the observed equity value is $4.0 billion. This is the market’s current common-equity value using those inputs.

The share-count input matters. Basic shares count the current common shares outstanding. Diluted shares include the potential effect of instruments such as options, restricted stock units, warrants, or convertible securities when they can increase the common share base. When the same share price is multiplied by a larger diluted share count, the observed total equity value can be higher, while per-share interpretation in model-based work must be checked against the larger share base.

| Formula input | What it captures | Why it can change the result |

|---|---|---|

| Share price | Observed market price per common share | Moves with market pricing, expectations, risk appetite, and company-specific information |

| Basic shares | Current common shares outstanding | Can understate the future share base if dilution is material |

| Diluted shares | Common shares plus potential dilutive securities | Can reduce per-share interpretation when ownership is spread across more shares |

| Model-implied share price | Estimated per-share value from a valuation model | Depends on assumptions rather than only current market price |

How Equity Value Connects to Enterprise Value

Enterprise value represents the value of the operating business available to all capital providers. Equity value narrows that value to the common-shareholder claim after capital-structure adjustments.

A common bridge starts with enterprise value, subtracts debt-like claims, preferred stock, and minority interest where relevant, then adds cash and non-operating assets that are not required inside the operating business. The result is an estimate of equity value.

Bridge logic: Enterprise value → subtract debt-like and non-common-equity claims → add excess cash or non-operating assets where relevant → equity value.

The direction of the bridge matters: moving from enterprise value to equity value requires capital-structure adjustments, while moving from equity value back to enterprise value reverses those adjustments.

The bridge is not only a mechanical formula. It is also an input-matching check. If the valuation starts with operating cash flows before financing costs, enterprise value is usually the starting point. If the analysis focuses directly on the common equity claim, equity value becomes the endpoint that must be matched to the correct share count.

Inputs That Change Equity Value

Equity value is sensitive to both market inputs and modeling choices. A clean calculation needs more than one headline number because the same company can produce different equity value estimates under different share-count, capital-structure, and valuation assumptions.

| Input | Effect on equity value | Common mistake |

|---|---|---|

| Share price or model output | Sets the observed or estimated value of the common equity layer | Treating the latest price as the same thing as a full valuation conclusion |

| Diluted shares | Changes total equity value and per-share interpretation when potential shares matter | Using basic shares when dilution is material |

| Debt-like claims | Reduce the residual value available to common shareholders when deriving equity value from enterprise value | Ignoring obligations that sit ahead of common equity |

| Cash and non-operating assets | Can increase the residual equity claim if they are not required for operations | Treating all cash as excess without checking operating needs |

| Preferred stock and minority interest | Can reduce common equity value because they represent claims not owned by common shareholders | Assuming all equity-like claims belong to common shareholders |

| Valuation multiple or DCF assumptions | Change the estimated business value that later flows into equity value | Confusing a model output with an intrinsic value estimate that has been stress-tested |

| Per-share interpretation | Translates total equity value into value per common share | Comparing total equity value and per-share value as if they were interchangeable |

Equity Value Sensitivity

Small changes in inputs can produce large changes in the common-shareholder claim. Sensitivity analysis is useful because it shows whether the result is supported by durable assumptions or mainly by a narrow set of optimistic inputs.

| Change in input | Likely direction | Interpretation boundary |

|---|---|---|

| Higher diluted share count | Can lower value per share | Total value may be unchanged while ownership is spread across more shares |

| Higher net debt | Can reduce the equity claim | More value is absorbed by claims ahead of common shareholders |

| More excess cash | Can increase the residual equity claim | The cash must be separable from normal operating requirements |

| Higher valuation multiple | Can raise estimated equity value | The multiple still needs support from growth, margins, durability, and risk |

| Lower discount rate or higher terminal assumptions | Can raise modeled value | The output becomes fragile if assumptions are not matched to risk |

| Lower earnings or cash-flow durability | Can reduce support for the estimate | A high equity value is weaker if the operating base is not durable |

Equity value connects to broader valuation judgment when the total claim is translated into a per-share estimate. A model can produce a precise number, but the interpretation depends on whether the assumptions, share count, and claim structure are internally consistent.

Simple Equity Value Example

A company trades at $25 per share and has 80 million basic shares outstanding. The basic equity value is $2.0 billion.

If potential dilution adds 10 million shares, the diluted share count becomes 90 million. At the same $25 share price, diluted equity value becomes $2.25 billion. The total equity value is higher because more potential common shares are included, but the ownership claim per share must now be interpreted against the larger share base.

If a valuation model instead estimates the operating business at $3.0 billion, and the company has $700 million of net debt and no other material adjustments, the implied equity value is $2.3 billion. That estimate then needs to be divided by the relevant diluted share count to check the implied value per share.

The example separates three things that are often blurred: observed market value, diluted ownership, and model-derived residual claim. The result is not a recommendation. It is a calculation framework that still needs business quality, cash-flow durability, and assumption review.

Equity Value vs Nearby Valuation Concepts

Equity value overlaps with several nearby concepts, but each answers a different question. Keeping the boundaries separate prevents the equity value calculation from becoming a broad valuation conclusion.

| Concept | Main question | Boundary for equity value |

|---|---|---|

| Equity value | What value is attributable to common shareholders? | Focuses on the residual common-equity claim |

| Enterprise value | What is the value of the operating business before financing structure? | Useful as the bridge into equity value, but not the same claim |

| Market capitalization | What is the market price of common equity using share price and shares outstanding? | Often close to observable equity value, but sensitive to share-count choice |

| Book value of equity | What accounting equity appears on the balance sheet? | Accounting value may differ sharply from market or model-implied equity value |

| Fair value | What value estimate is reasonable under a chosen valuation basis? | A fair value estimate may use equity value, but it is not automatically the same thing |

| Intrinsic value | What value is implied by internal assumptions about cash flows, risk, and durability? | Can feed an equity value estimate, but depends on model assumptions |

When Equity Value Can Mislead

Limitation: Equity value is not automatically a measure of investment merit. It does not prove that a stock is cheap, expensive, fairly priced, or mispriced. It is a valuation concept that becomes useful only when the inputs, assumptions, and comparison basis are matched correctly.

Common mistake: A single equity value number can create false precision. The calculation may look exact, but the result can change materially when diluted share count, net debt, cash treatment, preferred claims, minority interest, growth assumptions, discount rate, or terminal assumptions change.

Equity value is strongest when it is treated as a claim-mapping tool. It helps connect a company valuation to common shareholders, but it still needs supporting analysis of revenue durability, margins, cash flow, balance-sheet risk, capital allocation, and dilution.

FAQ

What is equity value?

Equity value is the value attributable to common shareholders. It can be observed as share price multiplied by shares outstanding or derived from enterprise value after capital-structure adjustments.

Is equity value the same as enterprise value?

No. Enterprise value measures the operating business value available to all capital providers, while equity value measures the residual claim available to common shareholders after relevant adjustments.

Is equity value the same as market capitalization?

They can be close when both use share price and shares outstanding, but the result depends on whether basic or diluted shares are used and whether the analysis is market-observed or model-derived.

Does a higher equity value mean a better investment?

No. A higher equity value only describes the size of the common-equity claim under the selected inputs. Investment interpretation still depends on assumptions, business quality, cash-flow durability, risk, and price.