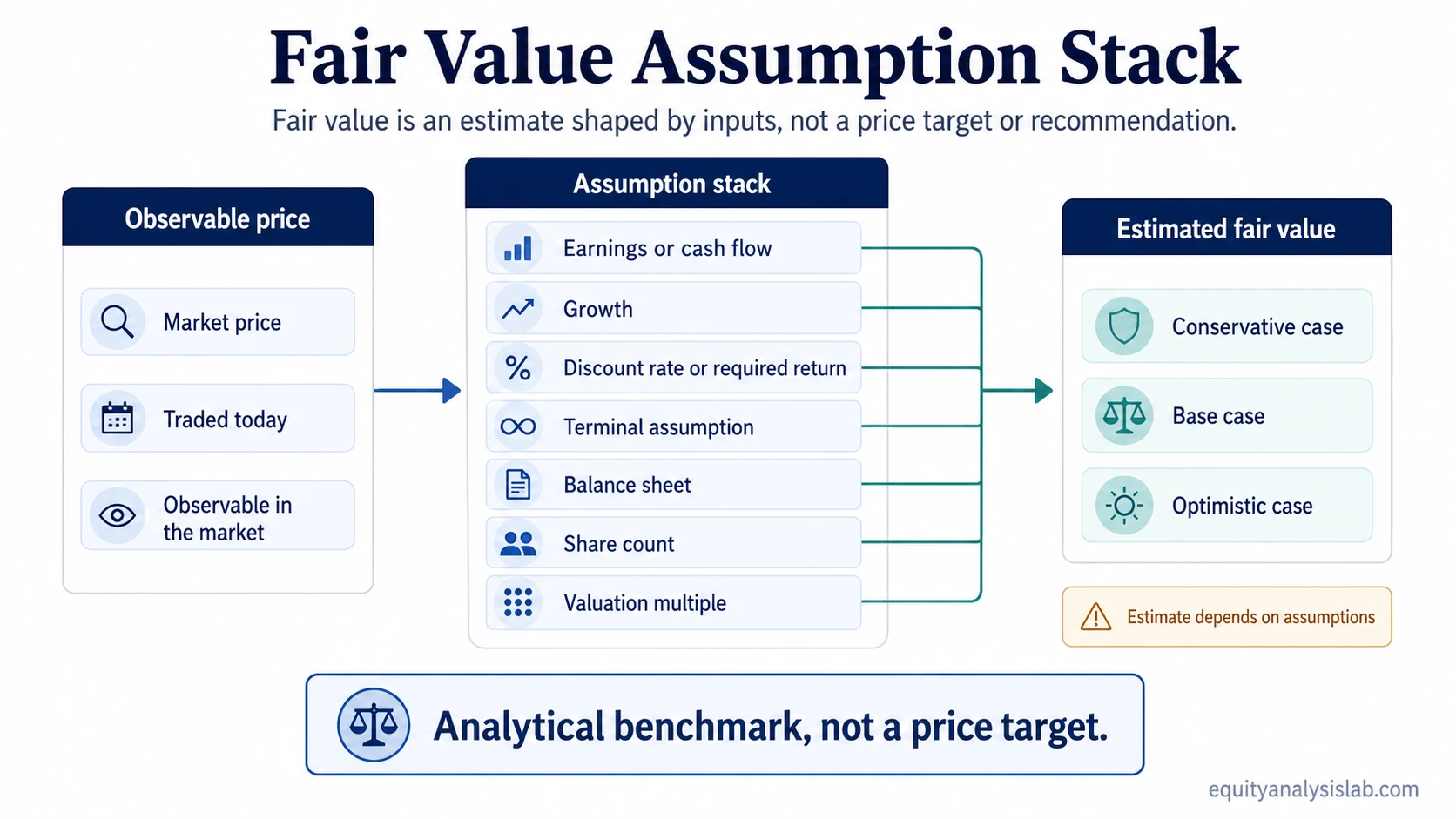

Fair value of a stock is an estimated benchmark for common equity based on assumptions about a company’s earnings, cash flow, growth, risk, balance sheet, share count, and valuation multiple or discount rate.

Investors often compare that estimate with the stock’s market price, but the comparison does not create a price target, forecast, or investment recommendation. The estimate is useful only when the assumptions behind it are clear enough to test.

Definition: Fair value of a stock is an estimate of what common equity may be worth under a specific valuation case. It is an analytical input for comparing value and price, not proof that the market is wrong.

Key points about stock fair value

- Fair value is an estimate, not a fact.

- The estimate changes when earnings, cash flow, growth, risk, discount-rate, balance-sheet, or share-count assumptions change.

- Market price is the traded price today; fair value is an analytical benchmark.

- A gap between market price and fair value requires assumption review before it means anything useful.

- Fair value should be used with business quality, risk, time horizon, and portfolio context.

What fair value means for a stock

For a public stock, fair value means an estimated value for the company’s common equity under a chosen valuation approach. The estimate may come from discounted cash flow, earnings power, comparable multiples, asset value, or a combination of methods.

The important part is the reasoning behind the number: the earnings base, cash-flow durability, growth expectation, risk assumption, dilution risk, and balance-sheet burden that shape the per-share result.

This stock-focused use is different from a compliance appraisal or a private-company valuation exercise. For an investor analyzing a listed company, fair value frames valuation assumptions against the price available in the market.

Fair value vs market price

Fair value and market price are often compared, but they are not the same thing. Market price is observable. Fair value is estimated.

| Concept | What it means | Investor interpretation |

|---|---|---|

| Fair value | An estimated valuation benchmark based on assumptions. | Useful for analysis, but only after the assumptions are reviewed. |

| Market price | The current price at which the stock trades in the market. | Observable, but not automatically correct or incorrect. |

| Gap between them | The difference between the estimate and the traded price. | Possible signal for deeper review, not an automatic conclusion. |

| Investor decision | The broader judgment that includes valuation, business quality, risk, time horizon, and portfolio context. | Fair value can inform the decision, but it does not replace the decision process. |

Inputs that shape a fair value estimate

A fair value estimate is built from inputs. If the inputs are weak, stale, or too optimistic, the output can look precise while being fragile.

| Input | Role in the estimate | Question to test |

|---|---|---|

| Earnings or free cash flow | Provides the base economic output being valued. | Is the company producing durable earnings or cash flow, or is the base year unusual? |

| Growth assumption | Estimates how the company’s economic output may expand or contract. | Is the growth assumption supported by revenue, margins, reinvestment, and competitive position? |

| Discount rate or required return | Converts future value into present value and reflects risk and time. | Does the rate match the risk of the company and the cash-flow stream being valued? |

| Terminal assumption | Captures value beyond the explicit forecast period. | Is the long-term assumption conservative enough for the company’s maturity and industry structure? |

| Balance-sheet context | Adjusts how enterprise claims, cash, debt, and other obligations affect equity value. | Does the estimate account for debt, cash, preferred claims, or other capital-structure items? |

| Share count | Translates total equity value into per-share value. | Could dilution, buybacks, or option issuance change the per-share result? |

| Comparable multiples | Provides a market-based cross-check against similar companies or prior valuation ranges. | Are the comparison group, margins, growth profile, and risk profile actually comparable? |

When fair value is expressed per share, the bridge from company value to common shareholder value matters. That is where equity value becomes relevant, because it focuses on the value attributable to common equity holders.

Why fair value changes when assumptions change

Fair value is sensitive because valuation inputs interact. A higher growth assumption can raise the estimate, but a higher required return can reduce it. A stronger margin outlook can improve cash-flow expectations, while dilution can reduce the per-share result even if total company value rises.

The estimate should therefore be treated as a range or scenario output, not a single permanent answer. A fair value number without assumption sensitivity can make uncertainty look cleaner than it really is.

| Illustrative scenario | Assumption pattern | Likely effect on fair value estimate |

|---|---|---|

| Conservative case | Lower growth, weaker margins, or higher required return | Lower estimate |

| Base case | Middle assumptions that match the analyst’s central view | Midpoint estimate |

| Optimistic case | Higher growth, stronger margins, or lower required return | Higher estimate |

Simple fair value example

This is a simplified illustration, not a valuation of a real company.

Assume a company is expected to generate $5.00 of normalized earnings per share. If an investor applies a 16x earnings multiple, the implied fair value estimate is $80 per share.

| Assumption | Input | Illustrative output |

|---|---|---|

| Normalized earnings per share | $5.00 | Base earnings input |

| Applied multiple | 16x | $80 estimated fair value |

| Lower multiple case | 14x | $70 estimated fair value |

| Higher multiple case | 18x | $90 estimated fair value |

The company did not change in this simplified example. Only the valuation multiple changed. That is why fair value should be read together with the assumptions used to produce it.

Fair value vs intrinsic value

Fair value and intrinsic value can overlap in investor language, but they are not always used with the same emphasis. Fair value is often a practical benchmark for what a stock may be worth under a defined valuation model. Intrinsic value usually points to a deeper estimate of underlying business value based on long-term fundamentals.

The distinction matters because both terms can sound more certain than they are. Each depends on assumptions, evidence quality, and the analyst’s judgment about the company’s future economics.

Where enterprise value fits

Fair value work can focus on the common equity directly, or it can start with the value of the operating enterprise and then bridge to common equity. That second route makes enterprise value relevant because it accounts for capital-structure items such as debt and cash before arriving at equity value.

The route should match the valuation method. A business valued using operating cash flow or EBITDA-style multiples usually needs a cleaner enterprise-to-equity bridge than a simple per-share earnings comparison.

What fair value does not tell you

- It is not a recommendation. A valuation estimate does not tell an investor what action to take.

- It is not a guaranteed future price. A stock can trade above or below an estimate for a long time.

- It is not a standalone signal. Business quality, balance-sheet risk, earnings durability, time horizon, and portfolio context still matter.

- It is not permanent. New information can change the earnings base, cash-flow outlook, risk premium, multiple, or required return.

- It is not proof that the market is wrong. A low market price may reflect risk that the estimate has not captured.

How to use fair value in a valuation process

A useful fair value estimate starts with a clear base case, then tests what would change the result. The investor can compare market price with the estimate, but the next step is assumption review: what has to be true for the estimate to hold?

A low valuation may be a risk premium, not a bargain. The cleaner question is what uncertainty the market may be discounting and whether that uncertainty is temporary, structural, or not yet understood.

Fair value is strongest when it acts as a risk-reference zone. It becomes weaker when it is treated as a hard floor, a certainty, or a shortcut around business analysis.

Related valuation concepts

Fair value is only one part of valuation work. Equity value helps translate company value into common shareholder value. Enterprise value helps when the valuation begins with the operating business and then adjusts for capital structure. Intrinsic value helps frame the deeper question of what the business may be worth under long-term assumptions.

FAQ

Is fair value the same as market price?

No. Market price is the current traded price of the stock. Fair value is an estimated valuation benchmark based on assumptions.

Does fair value mean a stock should trade at that price?

No. A stock can remain above or below a fair value estimate for a long time. The estimate is an analytical input, not a guarantee.

Why do different analysts calculate different fair values?

Different analysts may use different earnings, cash-flow, growth, risk, discount-rate, terminal-value, and multiple assumptions. Small changes in those assumptions can produce different estimates.

Is fair value a price target?

No. A fair value estimate can inform valuation work, but it is not the same as a price target, forecast, or recommendation.