Options are derivative contracts that give the buyer the right, not the obligation, to buy or sell an underlying asset at a strike price before or at expiration, depending on the contract style.

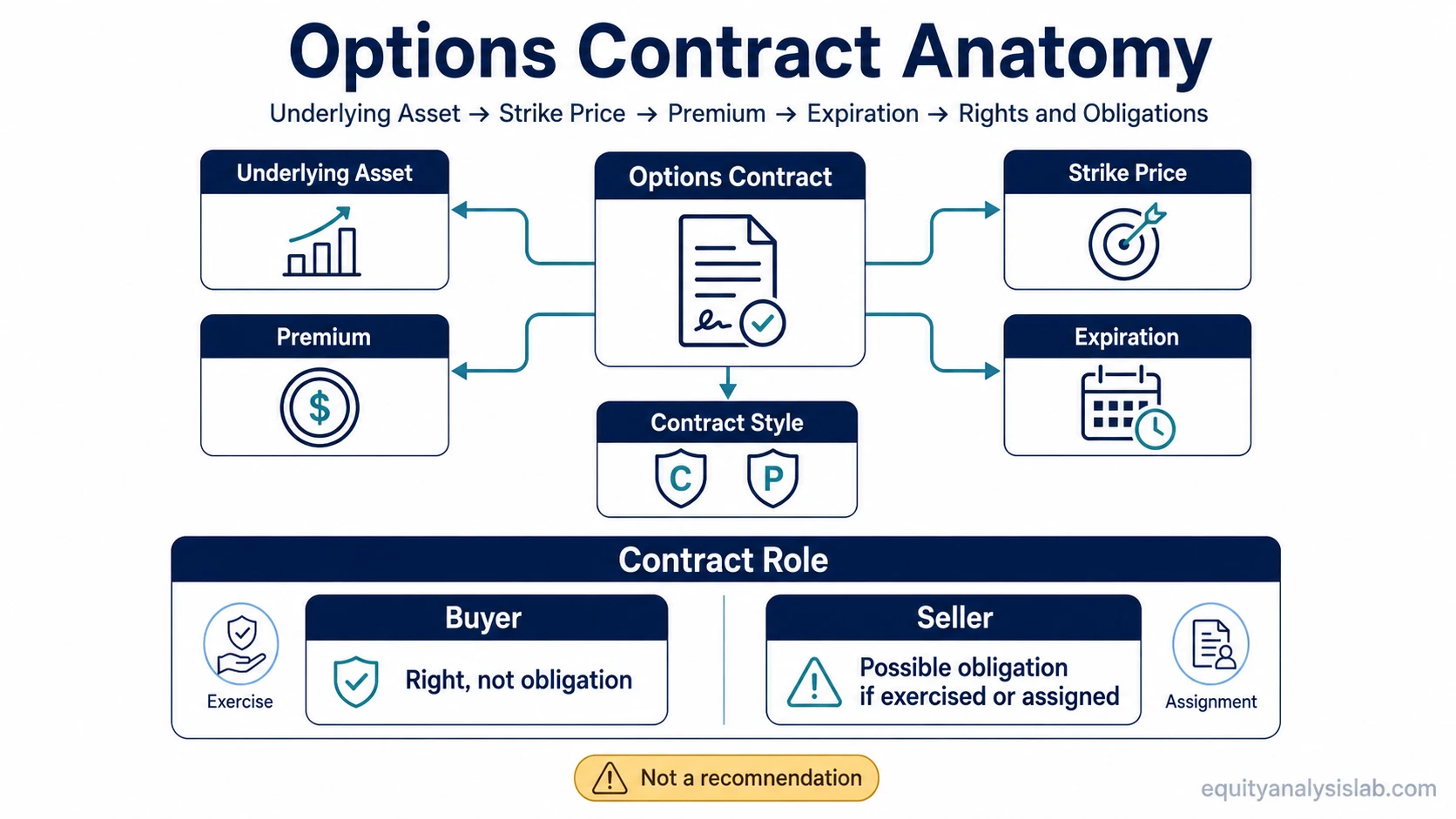

An options contract separates exposure from direct ownership. A stock investor owns shares, but an options buyer owns a contract right tied to an underlying asset, a strike price, an expiration date and a premium paid for that right.

The risk profile depends on the contract role. Buyers, sellers, call holders, put holders and spread users can face very different outcomes even when they are looking at the same underlying security.

Key Points About Options

- Options are derivative contracts, not direct ownership of the underlying asset.

- A call gives contract exposure to buying at a strike price; a put gives contract exposure to selling at a strike price.

- The buyer pays a premium for a right, while the seller or writer accepts an obligation if the contract is exercised or assigned.

- Expiration, implied volatility, liquidity and assignment risk can change how the same contract behaves.

- Strategy labels are only useful after the contract mechanics and risk boundaries are understood.

What Are Options?

Options are financial contracts linked to an underlying asset such as a stock, ETF or index. The contract defines a strike price, an expiration date, a premium and whether the right is structured as a call or a put.

The basic distinction is simple, but the risk is not always simple. A buyer can lose the premium paid if the contract does not become useful before expiration, while a seller may face obligations that extend beyond the premium received.

The first learning step is contract terminology: calls, puts, strike price, premium, expiration, exercise and assignment. Pricing, position management and spread structures become easier to evaluate after those terms are clear.

How an Options Contract Works

An options contract has several moving parts. Each part changes how the contract behaves before expiration and how risk is distributed between buyer and seller.

| Contract element | What it means | Why it changes interpretation |

|---|---|---|

| Underlying asset | The stock, ETF, index or other asset the option references. | The contract value is linked to this asset, but the contract is not the same as owning it. |

| Strike price | The price at which the contract right can be exercised. | The strike affects intrinsic value, moneyness and payoff shape. |

| Premium | The price paid by the buyer and received by the seller. | The premium defines the buyer’s upfront cost and part of the seller’s compensation for taking obligation risk. |

| Expiration | The date when the contract right ends. | Time remaining affects pricing, exercise decisions and position risk. |

| Contract style | The rules that define when exercise may occur. | Exercise timing can affect assignment risk and management decisions. |

A simplified example: if an investor pays a premium for a call option with a strike price above the current stock price, the contract only becomes economically useful if the stock move, time remaining and premium paid leave enough value. The stock can move in the expected direction and the contract can still disappoint if timing, volatility or premium cost work against the position.

Calls, Puts and Contract Roles

A call option gives the buyer the right to buy the underlying asset at the strike price. A put option gives the buyer the right to sell the underlying asset at the strike price.

The seller or writer is on the other side of that right. If the contract is exercised or assigned, the seller may have to deliver shares, buy shares or settle the contract according to its terms.

This role difference is why the same contract can have a limited-risk profile for one side and a much wider obligation profile for the other side.

| Role | Basic right or obligation | Risk boundary to understand |

|---|---|---|

| Call buyer | Right to buy at the strike price. | Can lose the premium paid if the contract does not retain value. |

| Put buyer | Right to sell at the strike price. | Can lose the premium paid if the contract does not retain value. |

| Call seller | May be obligated to sell or deliver the underlying exposure. | Risk depends on whether the position is covered, uncovered or part of a spread. |

| Put seller | May be obligated to buy the underlying exposure. | Risk depends on collateral, assignment terms and the underlying asset move. |

Options Risk Is Not Only Directional

Options are often discussed as bullish or bearish contracts, but direction is only one part of the risk. Time decay, implied volatility, liquidity, early exercise rules and assignment can all affect the final result.

A contract can be directionally correct and still lose value if the premium was too high, the move was too slow, volatility changed unfavorably or the contract expired before the expected scenario developed.

Important limitation: Options strategy names do not remove the need to understand the actual contract terms. A spread, covered call, protective put or cash-secured put can behave differently depending on strikes, expiration, premium, assignment exposure and portfolio role.

Where to Go Next

Options are easier to study when the learning path separates contract mechanics from pricing, strategy structure and position management.

| Learning path | Use it when you need to understand | Start here |

|---|---|---|

| Core concepts | Calls, puts, strike price, expiration, exercise and assignment. | Core options concepts |

| Directional and hedging strategies | How options are combined with directional views, hedging needs or portfolio exposure. | Directional and hedging strategies |

| Greeks and pricing | How delta, gamma, theta, vega, implied volatility and pricing models affect contract value. | Options Greeks and pricing |

| Position management | Assignment, rolling, expiration, liquidity, pin risk and position adjustment questions. | Options position management |

| Volatility and spreads | How spread structures and volatility assumptions change payoff and risk. | Volatility and spread structures |

Common Options Topics

Some options questions are not answered by the contract definition alone. Assignment, pricing models and spread construction each need their own context.

For position risk, start with assignment risk before comparing short-option structures. For income-oriented collateral structures, review the cash-secured put as a separate contract structure rather than as a generic yield label.

For pricing logic, the Black-Scholes model belongs in the pricing layer, not the basic contract definition. For expiration behavior, pin risk shows why settlement and strike proximity can matter near expiration.

For defined-risk bearish structures, a bear put spread is better studied as a spread structure than as a simple put option.

FAQ

Are options the same as owning the underlying stock?

No. Owning a stock means owning shares. Owning an option means holding a contract right linked to an underlying asset, strike price, premium and expiration date.

What is the difference between a call and a put?

A call gives the buyer the right to buy the underlying asset at the strike price. A put gives the buyer the right to sell the underlying asset at the strike price.

Can an options buyer lose more than the premium paid?

For a simple long option, the buyer’s loss is generally limited to the premium paid. More complex positions, exercises, assignments or combined structures can create different exposures, so the full position must be evaluated.

Why does expiration matter in options?

Expiration matters because the contract right exists only for a defined period. Time remaining affects pricing, exercise decisions and whether the contract keeps enough value to justify the premium paid.

How should strategy labels be interpreted?

Strategy names describe structures, not recommendations. A structure still has to be judged by contract terms, risk, portfolio role, liquidity, volatility and assignment exposure.