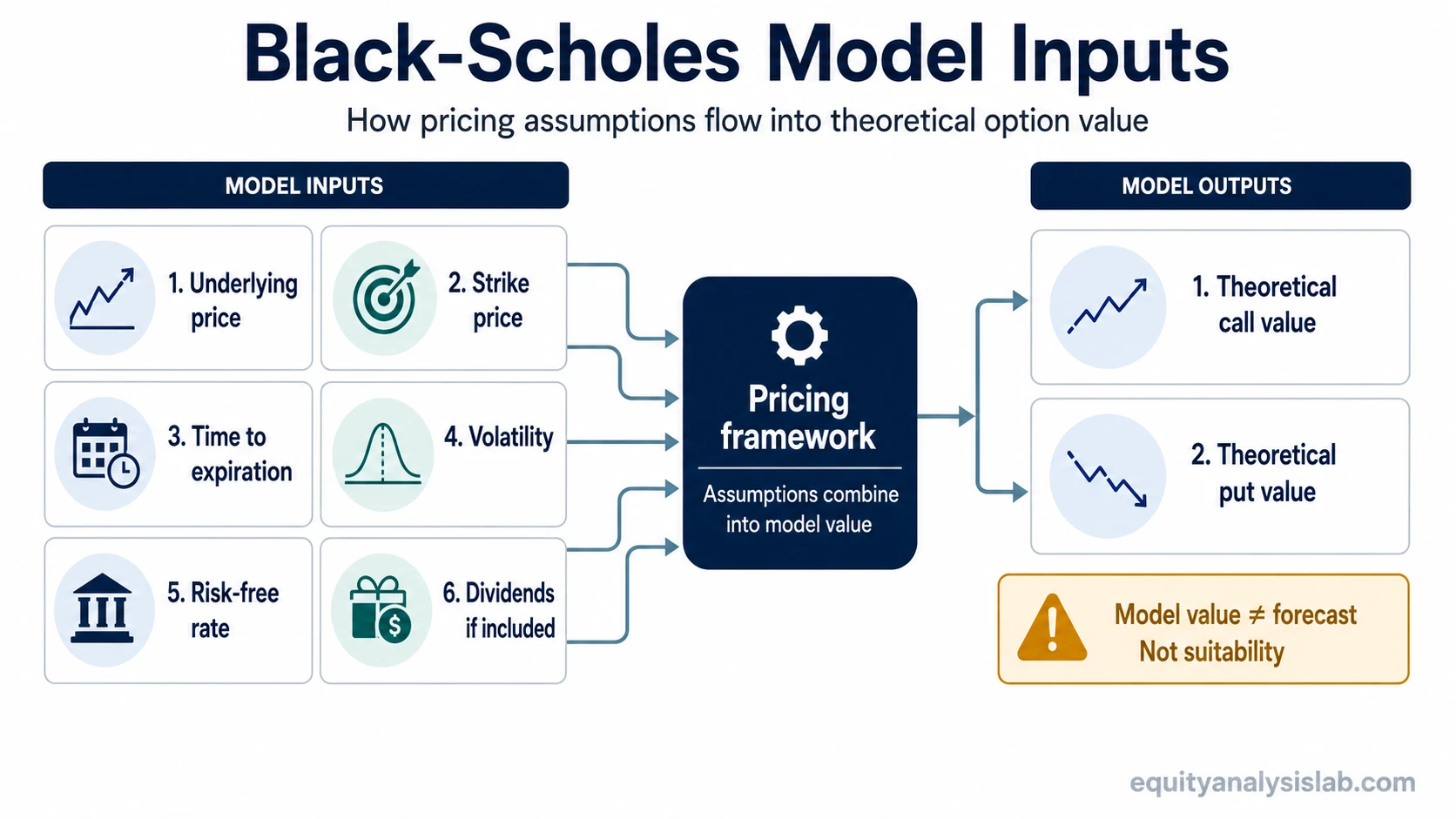

The Black-Scholes model is an options pricing model that estimates the theoretical value of a call or put from inputs such as the underlying price, strike price, time to expiration, volatility, risk-free rate, and, in some versions, dividends.

The model separates option value into measurable drivers. It does not determine whether an option position is suitable, whether the option will be profitable, or how the position may behave before expiration when volatility, liquidity, spreads, and exercise features change.

Definition: The Black-Scholes model estimates a theoretical option premium from a defined set of pricing inputs. For a call option, it estimates the value of the right to buy the underlying at the strike price. For a put option, it estimates the value of the right to sell the underlying at the strike price.

The output is a model value, not a forecast of the underlying price. A quoted market premium can differ from the model estimate because market participants may use different volatility assumptions, because spreads and liquidity matter, or because a contract has features that the simplified model view does not fully capture.

Key Points

- Black-Scholes estimates theoretical option value, not investment suitability.

- The main inputs are underlying price, strike, time, volatility, risk-free rate, and sometimes dividends.

- Volatility is often the most interpretation-sensitive input because implied volatility can move before the underlying reaches expiration.

- The model value is different from an expiration payoff diagram, margin impact, liquidity condition, or realized trading result.

- The estimate is most useful when the assumptions behind the inputs remain visible.

Black-Scholes model inputs

Each input changes the theoretical premium through a different channel. The input table matters more for most investors than memorizing the equation because it identifies what can move the option value before expiration.

| Input | What it represents | How it affects model value | Investor interpretation |

|---|---|---|---|

| Underlying price | The current price of the stock or other underlying asset. | Changes the distance between the market price and the strike price. | Connects the option premium to price movement and option moneyness. |

| Strike price | The exercise price written into the option contract. | Defines whether the option is in the money, at the money, or out of the money. | Creates the contract boundary, but not the full risk picture. |

| Time to expiration | The remaining life of the option contract. | More time usually increases the model value because there is more time for price movement to matter. | A longer expiration may reduce urgency, but it does not remove premium risk or volatility risk. |

| Volatility | The expected movement of the underlying over the option’s life. | Higher volatility generally increases theoretical option value because larger price ranges make optionality more valuable. | Implied volatility can raise or lower model value even when the underlying price has not moved much. |

| Risk-free rate | The interest-rate input used in the model. | Affects the present value of the strike and can influence call and put values differently. | Usually secondary for short-dated equity options, but more relevant when rates or maturities are large. |

| Dividends, if included | Expected cash distributions from the underlying stock. | Dividend-adjusted versions can reflect how expected distributions affect option value. | Most relevant for dividend-paying stocks and contracts where early exercise considerations may matter. |

Black-Scholes formula meaning without heavy derivation

The formula combines the underlying price, strike price, time, volatility, and interest-rate assumptions into a theoretical option value. In simplified terms, it estimates the present value of expected option payoff under a specific probability framework.

The practical value comes from showing which assumptions drive the premium. When the underlying price, time, or volatility changes, the model value changes because the option’s probability-weighted payoff profile has changed inside the pricing framework.

The Greeks connect naturally to Black-Scholes. Delta describes the model’s sensitivity to underlying price movement, while gamma describes how that price sensitivity can change as the underlying moves.

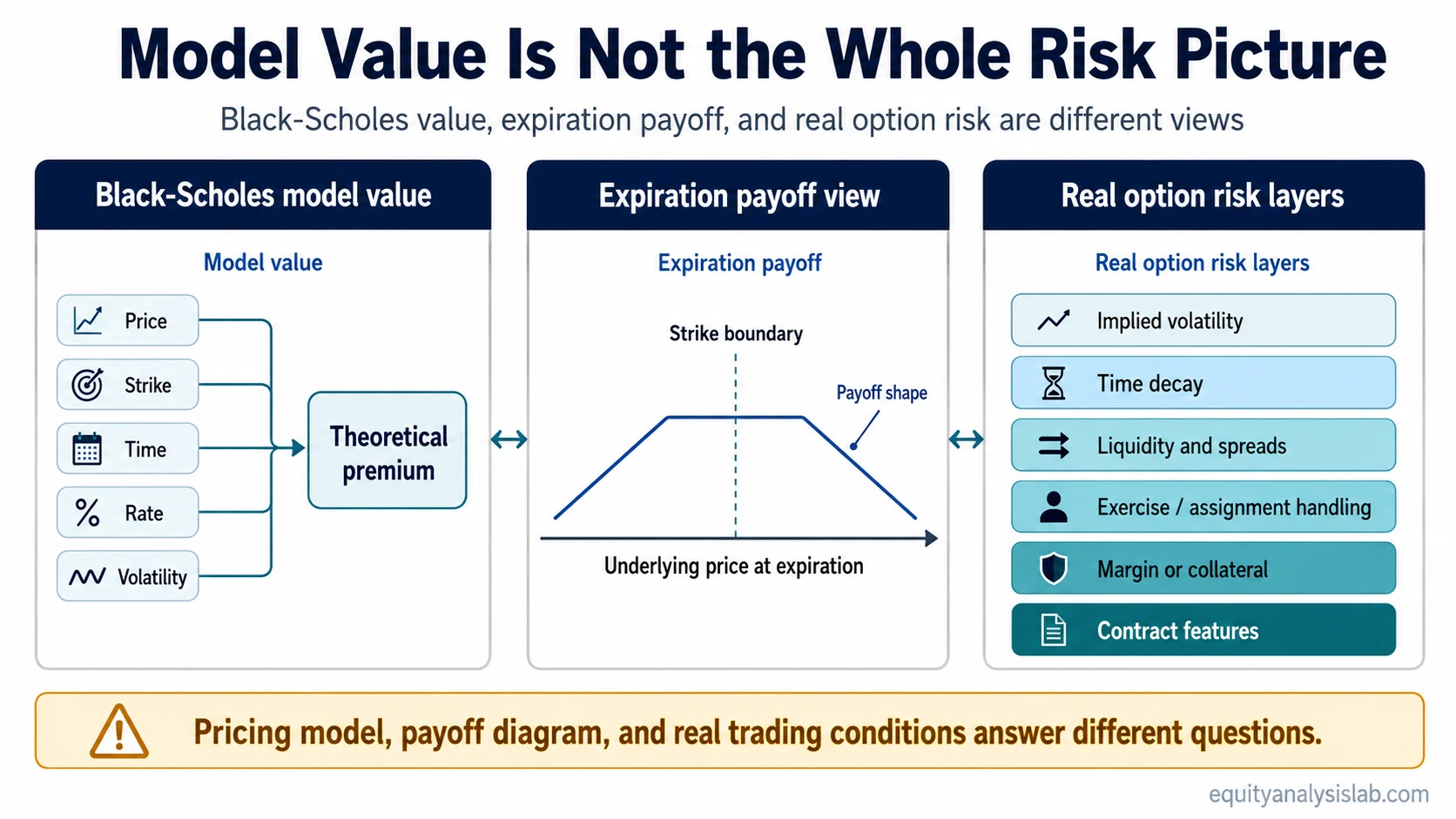

Model value is not the same as payoff or real option risk

A payoff diagram usually shows what the option position is worth at expiration across different underlying prices. Black-Scholes estimates theoretical value before or at expiration under pricing assumptions. Those are related, but they are not the same view of risk.

| Question | Black-Scholes model value | Expiration payoff view | Real option risk layer |

|---|---|---|---|

| What is being measured? | Theoretical option premium under pricing assumptions. | Contract payoff at expiration. | Actual position behavior across price, time, volatility, spreads, liquidity, and exercise handling. |

| Does it show path risk? | Only indirectly through time and volatility inputs. | No. It usually shows the end point only. | Time decay, volatility changes, and changing Greeks still need separate interpretation. |

| Does it show liquidity? | No. | No. | Bid-ask spreads, open interest, and execution quality can change the realized result. |

| Does it show exercise or assignment handling? | Only within the model’s exercise assumptions. | Only at a simplified expiration boundary. | Real contracts may require attention to dividends, early exercise features, expiration procedures, and broker rules. |

| Can it identify a good trade? | No. It estimates a theoretical value. | No. It maps a payoff shape. | Suitability depends on objective, risk capacity, position size, liquidity, assumptions, and alternative exposures. |

Black-Scholes can help explain why an option has value, while real option risk requires more than one model output. A contract can look reasonable in a model and still be fragile if implied volatility falls, time decay accelerates, spreads widen, or the investor misunderstands the exercise boundary.

Why implied volatility matters so much

Volatility is the input that often creates the largest interpretation gap between a clean model estimate and the real market quote. A higher volatility assumption increases the theoretical value of optionality because the model assigns more value to a wider range of possible future prices.

That does not make higher implied volatility automatically good or bad. A buyer may pay more premium when implied volatility is elevated. A lower-volatility assumption may reduce model value even if the directional view has not changed. The estimate can therefore change before the final payoff outcome is known.

This is where gamma risk and volatility exposure become practical interpretation issues. The model can show sensitivities, but the investor still has to understand how those sensitivities can change as price, time, and volatility move together.

Black-Scholes example: same strike, different value

Consider two call options with the same underlying and strike. One has more time to expiration and a higher volatility assumption. The other has less time and a lower volatility assumption. The first option may show a higher theoretical value in Black-Scholes even if both options would have the same intrinsic value at the same underlying price.

The higher model value does not automatically make the first option more attractive. The higher premium may reflect more time value, a richer volatility assumption, or a wider expected price range. A stronger reading compares the model inputs, the market quote, the bid-ask spread, the remaining time, and the contract’s payoff boundary before treating the premium as meaningful.

What the Black-Scholes model does not show

Black-Scholes is useful only inside its assumptions. Real contract terms, market conditions, and investor constraints can change the interpretation of the estimate.

- Changing volatility: the model needs a volatility input, but implied volatility can shift quickly.

- Liquidity and spreads: a theoretical value may not be executable near that level if the option market is wide or thin.

- Exercise features: the classic framework is designed around European-style exercise, while U.S. listed equity options are commonly American-style and may be exercised before expiration.

- Dividends: dividend assumptions can matter for equity options, especially around ex-dividend dates and early exercise decisions.

- Path before expiration: a final payoff view does not capture every mark-to-market change before expiration.

- Investor suitability: a model estimate does not determine whether a position fits an investor’s objective, risk capacity, or portfolio context.

Common mistake: treating model output as a signal

A Black-Scholes value can look precise because it comes from a formula. The precision is conditional on the inputs. If the volatility assumption, dividend assumption, time horizon, or execution price is wrong, the output can be precise without being useful.

The safer interpretation is to treat the model as a diagnostic tool. It helps identify what the option premium is sensitive to. It does not say that the option is underpriced, overpriced, or appropriate for a specific investor.

How to read a Black-Scholes estimate

A clean reading starts with the model output and then checks what created it. If most of the value comes from time and volatility, the option may be more exposed to volatility repricing and time decay than the payoff diagram suggests. If most of the value comes from intrinsic value, the position may behave more like the underlying, but liquidity and exercise details still matter.

| Reading step | Question to ask | Why it matters |

|---|---|---|

| Check moneyness | Is the option in the money, at the money, or out of the money? | Moneyness changes how much of the premium is intrinsic value versus time value. |

| Check time | How much expiration time remains? | Time affects the value of optionality and the pace of time decay. |

| Check volatility | Is the model value being driven mainly by the volatility assumption? | Volatility repricing can change premium even without a large underlying move. |

| Check quote quality | Is the live market close to the theoretical value, or are spreads wide? | A model estimate is less useful when execution is poor or liquidity is thin. |

| Check contract features | Do dividends, early exercise rules, or expiration procedures affect interpretation? | Contract mechanics can matter more than the simplified model view suggests. |

FAQ

Is the Black-Scholes model still used?

Black-Scholes is still commonly used as a reference framework for understanding how inputs affect theoretical option value. Its output still needs interpretation because real option prices reflect market assumptions, liquidity, contract features, and changing volatility.

Is Black-Scholes the same as an option calculator?

No. An option calculator may use Black-Scholes or a related model to produce a value. The model is the pricing framework; the calculator is only a tool interface for entering assumptions and reading the output.

Does Black-Scholes predict whether an option will make money?

No. Black-Scholes estimates theoretical option value under pricing assumptions. It does not predict the future underlying price, guarantee a payoff, or decide whether an option fits a specific investor.

Why does implied volatility matter in Black-Scholes?

Implied volatility affects the value assigned to future price movement. Higher implied volatility generally increases theoretical option value, while lower implied volatility generally reduces it, all else equal.