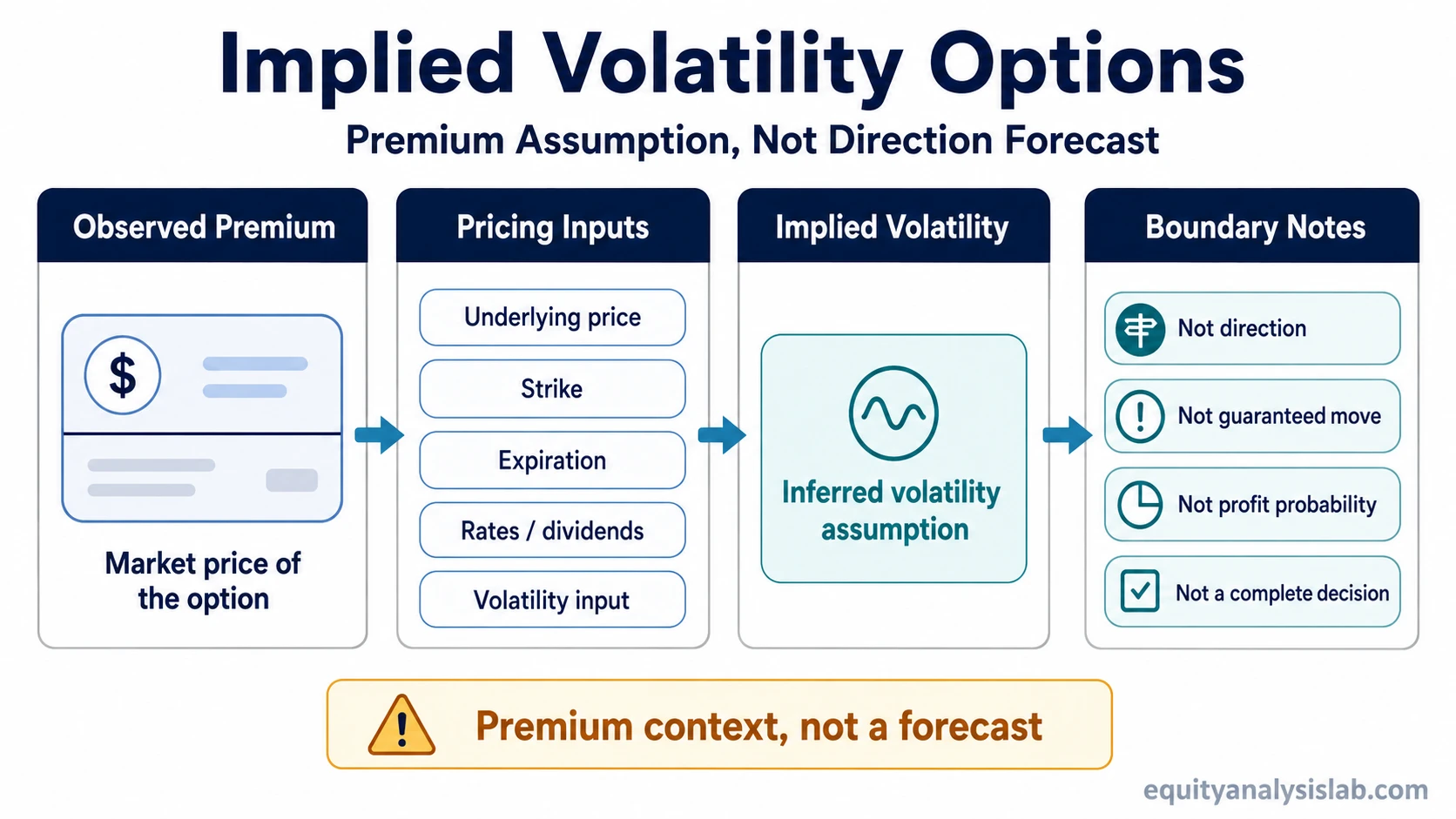

In options, implied volatility is the volatility assumption embedded in an option’s market price. It helps explain why an option premium is higher or lower, but it does not prove market direction, guarantee future movement, or provide a fixed probability of profit.

Definition: Implied volatility is the market-implied volatility input that option pricing models use to connect an observed option premium with the underlying price, strike, expiration, rates, dividends, and other assumptions.

The important point is that implied volatility is not directly observed future volatility. It is inferred from the option price. When buyers and sellers price more uncertainty into an option, implied volatility usually rises. When less uncertainty is priced in, implied volatility usually falls.

That makes implied volatility useful for reading premium and uncertainty, not for making a direction forecast. A call and a put can both reflect higher implied volatility when the market prices a wider range of possible outcomes.

Key Points

- Implied volatility is a pricing input inferred from an option’s market premium.

- Higher implied volatility usually raises option premiums when other pricing inputs are held constant.

- Lower implied volatility usually reduces option premiums when other pricing inputs are held constant.

- Implied volatility differs from historical volatility because it reflects current option pricing, not only past price movement.

- IV does not show direction, guarantee an expected move, or make an option position safe.

What Implied Volatility Means in Options

Implied volatility represents the level of volatility that is being priced into an option. It is called “implied” because the market price of the option is known first, and the volatility assumption is backed out from that price through a pricing model.

If two otherwise similar options have different premiums, implied volatility can help explain part of that difference. The option with the higher premium may reflect a larger volatility assumption, more uncertainty around a future event, a different strike and expiration profile, or market microstructure effects such as wider bid-ask spreads.

IV should be read as an assumption inside the premium, not as a promise that the underlying security will move by a specific amount. The actual realized movement can be lower, higher, or distributed differently than the market-implied assumption suggested at the time the option was priced.

How Implied Volatility Affects Option Premium

When implied volatility rises, option premiums usually rise if the underlying price, strike, expiration, rates, dividends, and other inputs are unchanged. The reason is simple: a larger volatility assumption increases the value of optionality because the option has more possible price paths before expiration.

When implied volatility falls, option premiums usually decline under the same all-else-equal assumption. This can happen even if the underlying stock or ETF has not moved much. The premium can change because the volatility input changed, not because the underlying delivered a large price move.

This relationship must be qualified. Option premiums also respond to moneyness, time to expiration, interest rates, dividends, liquidity, bid-ask spreads, and model assumptions. Implied volatility is a major input, but it is not the only input.

Boundary: A high premium does not automatically mean the option is overpriced, and a low premium does not automatically mean the option is underpriced. The premium has to be interpreted together with expiration, strike, liquidity, event risk, and the reason volatility is being priced into the contract.

Implied Volatility as a Pricing Model Input

In option pricing, implied volatility is the volatility input that makes the model price align with the observed market premium. The model does not discover a certain future outcome. It translates a market premium into a volatility assumption under the model’s structure.

The Black-Scholes model is one common way to explain this logic. Given the underlying price, strike, time to expiration, rates, dividends where relevant, and a volatility input, a model can estimate an option value. In practice, traders and investors often observe the market price first and infer the volatility input that would produce that price.

This is why implied volatility can be useful and limited at the same time. It gives a structured way to read how uncertainty is embedded in premiums, but the model depends on assumptions. Those assumptions can fit some contracts better than others, especially when strikes, expirations, liquidity, and event timing differ.

Implied Volatility vs Historical Volatility

Historical volatility looks backward. It measures how much the underlying security actually moved over a past period. Implied volatility looks through the current option premium and reflects the volatility assumption the market is pricing now.

The two can differ sharply. Historical volatility may be low while implied volatility rises before earnings, a product announcement, a macro event, or another uncertainty window. Historical volatility may also be high after a large move while implied volatility falls if the market believes the uncertainty has passed.

| Measure | What it uses | What it helps explain | Main limitation |

|---|---|---|---|

| Implied volatility | Current option premium and pricing model inputs | How much volatility assumption is embedded in the option price | It is model-dependent and does not guarantee future movement |

| Historical volatility | Past movement in the underlying security | How much the underlying has moved over a prior period | It looks backward and may not reflect current event risk or changing expectations |

| IV rank or IV percentile | Current IV compared with its own prior range or distribution | Whether current IV is high or low relative to its own history | It is context, not a complete option decision or probability of profit |

IV rank and IV percentile can add context by comparing current implied volatility with past implied volatility for the same underlying. They do not replace analysis of the contract, the event, the strategy, liquidity, or the reason the premium is elevated or subdued.

What Implied Volatility Can and Cannot Tell You

Implied volatility can help interpret how much uncertainty is embedded in an option premium. It can also help compare premiums across strikes, expirations, or time periods when other inputs are considered carefully.

It cannot tell you whether a call or put will be profitable. It cannot prove that the stock will move enough to offset time decay, bid-ask spread, or changes in volatility after entry. It also cannot replace position sizing, contract selection, or risk control.

| IV can help with | IV cannot prove |

|---|---|

| Whether a premium reflects more or less priced uncertainty | The future direction of the underlying security |

| Why an option premium may rise even without a large underlying move | That a trade has a positive expected outcome |

| How current option pricing compares with historical volatility context | That expected movement will actually occur |

| How volatility assumptions differ by strike or expiration | That the option is cheap, expensive, safe, or unsafe by itself |

Vega, Expiration, and Event Risk

Implied volatility affects option premium through volatility sensitivity. Option delta focuses on estimated price sensitivity to the underlying price. Vega focuses on how much the option premium may change when implied volatility changes, all else equal.

Expiration also matters. A short-dated option before an event may react strongly to changes in implied volatility because the uncertainty window is concentrated. A longer-dated option may spread uncertainty over more time, so the same IV change can have a different premium effect.

This is where sensitivity can change quickly. Near expiration or near a strike, option behavior can shift as the underlying price moves, time passes, and volatility assumptions reset.

Event risk can raise implied volatility before the event and reduce it after uncertainty is resolved. This post-event volatility decline is often called volatility crush. It can affect calls and puts because the volatility input changes, not because the option suddenly knows direction.

Across strikes, implied volatility can differ across strikes instead of staying flat. That means one IV number should not be treated as a universal description of every contract on the same underlying.

Common Mistakes With Implied Volatility

Mistaking high IV for an instruction: High implied volatility can mean the premium is elevated, but it does not automatically mean the option should be sold. The market may be pricing a real uncertainty, an upcoming event, market microstructure effects, or a wide distribution of possible outcomes.

Mistaking low IV for safety: Low implied volatility can mean less volatility is embedded in the premium, but it does not remove downside, exercise, assignment, liquidity, or expiration risk where those factors apply. A low-IV option can still lose value.

Treating IV as a forecast: Implied volatility reflects the volatility assumption inside market prices. It can be compared with realized volatility later, but it is not the same as knowing future movement in advance.

Ignoring contract structure: The same IV number can have different implications across strikes, expirations, and liquidity conditions. Moneyness, bid-ask spread, event timing, and time remaining all affect how useful the number is.

Simple Example

A call option and a put option can both become more expensive when implied volatility rises, even if the underlying stock has not yet moved. The higher premium reflects a larger volatility assumption in the model, not a guaranteed bullish or bearish outcome.

Suppose two options have the same underlying price, strike, and expiration. If the market starts pricing a wider range of possible outcomes before an event, the option premiums may rise because the implied volatility input rises. The premium change does not mean the market has selected one direction. It means the cost of optionality has changed.

After the event passes, implied volatility may fall if uncertainty is reduced. That decline can pressure option premiums even if the underlying move is smaller than expected, delayed, or partially offset by time decay.

Related Concepts

Pricing model boundary: Black-Scholes helps show how a volatility input fits into a broader option-pricing structure.

Directional sensitivity boundary: Delta is more useful when the question is how much an option premium may change from movement in the underlying price.

Changing sensitivity boundary: Gamma risk matters when option sensitivity can accelerate near a strike or close to expiration.

Strike structure boundary: Volatility smile matters when implied volatility differs across strikes rather than staying constant.

FAQ

What is implied volatility in options?

Implied volatility is the volatility assumption embedded in an option’s market price. It helps explain how much uncertainty is priced into the premium, but it does not guarantee future movement.

Does high implied volatility mean an option will move more?

High implied volatility means the option premium is pricing more expected volatility or uncertainty. The actual move can be smaller, larger, delayed, or different from what the premium implied.

Is implied volatility the same as historical volatility?

No. Historical volatility measures past realized movement. Implied volatility is inferred from current option prices and reflects the volatility assumption being priced now.

Does implied volatility show market direction?

No. Implied volatility shows how much volatility is priced into an option, not whether the underlying security will move up or down.