An option’s delta is often used as a shortcut for probability or stock-like exposure, but that shortcut is incomplete. A delta option reading estimates how much an option price may change for a one-dollar move in the underlying security, all else equal.

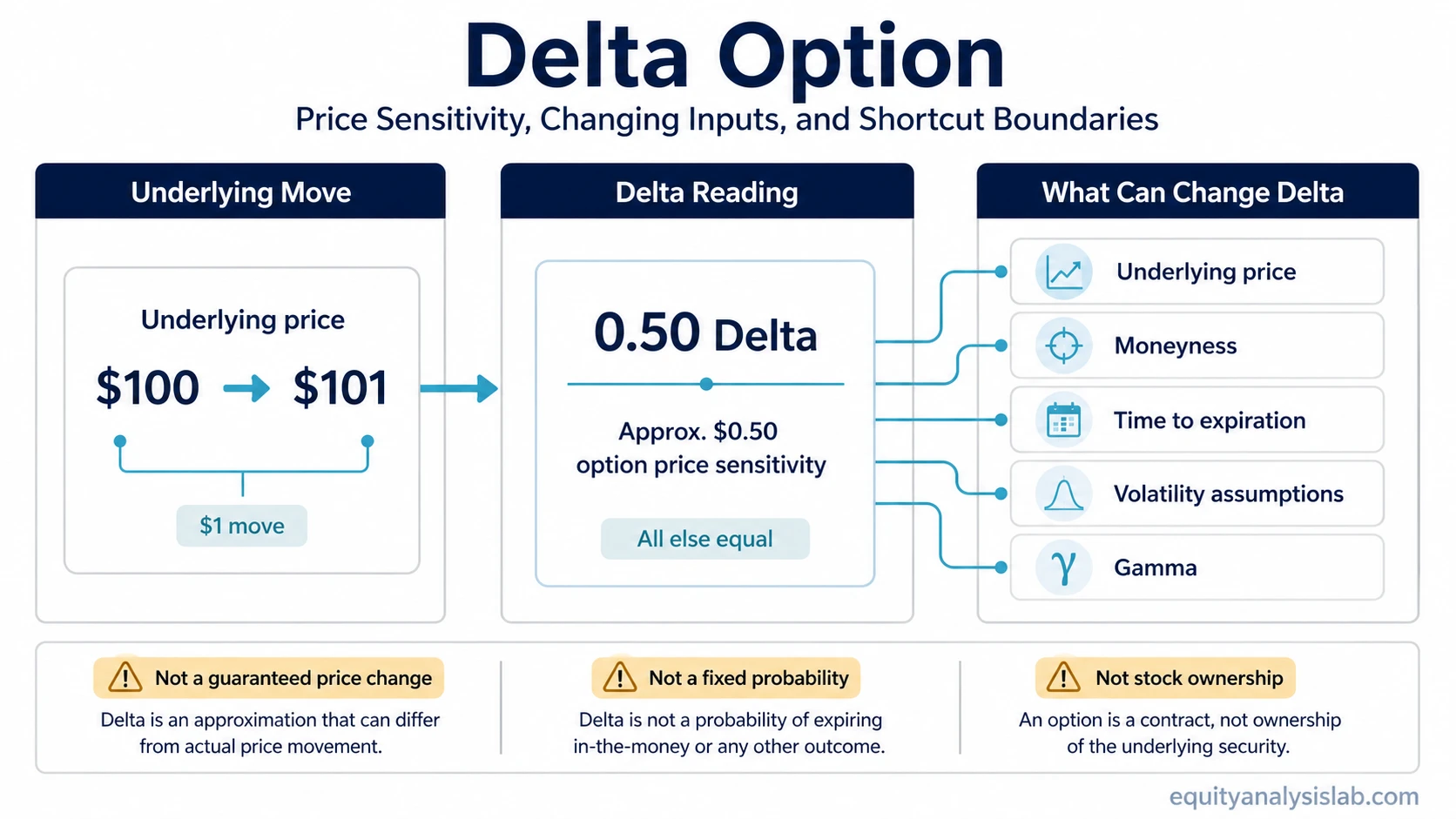

Common misunderstanding: Delta is useful because it compresses directional sensitivity into one number. It is not a recommendation, a guaranteed price change, a fixed probability, or actual ownership of the underlying shares.

A delta reading changes as the underlying price, moneyness, time to expiration, volatility assumptions, and other pricing inputs change. It helps describe sensitivity, but it does not decide whether an option should be bought, sold, held, exercised, or avoided.

Key Points

- Delta estimates theoretical option price sensitivity to a one-dollar move in the underlying security, all else equal.

- Call options usually have positive delta, while put options usually have negative delta.

- Delta can be used as a rough probability shortcut, but it is not a fixed probability of expiring in the money.

- Delta changes as price, moneyness, time, volatility assumptions, and gamma change.

- Delta does not remove contract limits such as premium paid, strike price, expiration, liquidity, or exercise and assignment rules.

What Is Delta in Options?

Definition: Delta is an option Greek that estimates the theoretical change in an option’s price for a one-dollar change in the underlying security, assuming other pricing inputs stay constant.

A call option with a delta of 0.50 would be expected to gain about $0.50 if the underlying rises by $1, before considering changes in volatility, time decay, bid-ask spread, or other inputs. A put option with a delta of -0.50 would be expected to gain about $0.50 if the underlying falls by $1 under the same simplified assumption.

Delta is model-derived, so the reading depends on the pricing framework and assumptions used. In a model-based options workflow, Greeks are often connected to theoretical option value, including inputs used in the Black-Scholes model.

How to Read Positive and Negative Delta

Call options generally have positive delta because their value tends to rise when the underlying price rises. Put options generally have negative delta because their value tends to rise when the underlying price falls.

| Option position | Typical delta sign | Basic interpretation |

|---|---|---|

| Long call | Positive | The option price usually benefits from an upward move in the underlying. |

| Long put | Negative | The option price usually benefits from a downward move in the underlying. |

| Short call | Negative exposure to call delta | The seller has the opposite directional exposure of the long call holder. |

| Short put | Positive exposure to the underlying | The seller has the opposite directional exposure of the long put holder, so the position typically benefits from upward movement and is hurt by downward movement. |

The sign tells the direction of sensitivity, not whether the contract is attractive. Premium, strike, expiration, liquidity, assignment risk, and portfolio context still matter.

Simple Delta Option Example

An option quoted with a 0.50 delta has an approximate sensitivity of $0.50 for a $1 move in the underlying security. If the underlying rises from $100 to $101 and the rest of the pricing inputs remain unchanged, the option price may move from $3.00 to about $3.50.

That example is only a simplified sensitivity reading. The actual quoted option premium can differ because implied volatility may change, time passes, liquidity affects execution, and the option’s moneyness can shift as the underlying moves.

What Changes Delta?

Delta is not fixed. It moves as the option moves through different price zones and as the pricing assumptions around the contract change.

| Input or condition | How it can affect delta | Why the reading can shift |

|---|---|---|

| Underlying price | Delta can rise or fall as the underlying moves toward or away from the strike. | The option becomes more or less sensitive as intrinsic value changes. |

| Moneyness | In-the-money, at-the-money, and out-of-the-money options usually carry different delta profiles. | At-the-money options often have meaningful sensitivity, while deep in-the-money options may behave more stock-like. |

| Time to expiration | Delta can become less stable as expiration approaches, especially near the strike. | Small underlying moves can have a larger effect when little time remains. |

| Volatility assumptions | Changing volatility expectations can alter option value and the usefulness of a simple delta reading. | When volatility assumptions shift, the option premium may move for reasons not explained by delta alone. |

| Gamma | Delta itself can change faster when gamma is higher. | Gamma describes how quickly delta changes as the underlying price moves. |

Delta, Moneyness, and Probability Shortcuts

Delta is sometimes used as a rough market convention for probability. For example, a 0.30 delta call is often loosely described as having a lower chance of expiring in the money than a 0.70 delta call. That shortcut can be useful for orientation, but it should not be treated as a precise forecast.

Moneyness gives the shortcut some context. In-the-money options already have intrinsic value, at-the-money options sit near the current underlying price, and out-of-the-money options need a larger move before intrinsic value appears. Delta tends to reflect those differences, but it also changes with time, volatility assumptions, and price movement.

Boundary: Delta can help compare relative sensitivity between options, but it does not state the true probability of profit, the probability of exercise, or the final payoff of the contract.

Delta Is Not Stock Ownership

Delta is sometimes translated into a share-equivalent analogy. A 0.50 delta option contract may be described as having roughly 50 shares of directional exposure because one standard equity option contract usually represents 100 shares. That analogy can help explain sensitivity, but it is not the same as owning shares.

Stock ownership has no option expiration date, no strike price, and no option premium decay. An option contract is defined by premium, strike, expiration, contract terms, liquidity, and exercise or assignment rules. Delta only describes one part of the contract’s theoretical price sensitivity.

Where the Delta Shortcut Breaks

Delta becomes less reliable as a shortcut when assumptions change. The reading is usually based on a model snapshot, but option prices move through changing time, volatility, liquidity, and moneyness conditions.

- Model assumptions: Greeks depend on theoretical pricing assumptions, so they are not direct guarantees of quoted market movement.

- Path dependence: The route the underlying takes can matter, especially when the option moves near the strike or close to expiration.

- Volatility shifts: An option can move differently from its delta estimate if volatility expectations rise or fall sharply.

- Time decay interaction: Time passing can reduce option value even when the underlying moves in a favorable direction.

- Expiration effects: Delta can change quickly near expiration when the underlying is close to the strike.

- Exercise and assignment: Contract mechanics can matter, especially around expiration, dividends, or short-option exposure.

- Liquidity: Wide bid-ask spreads can make theoretical sensitivity different from practical execution prices.

Related Greeks and Pricing Inputs

Delta is only one part of the options Greeks and pricing framework. The related concepts below help keep the reading inside its proper boundary.

| Related concept | How it relates to delta |

|---|---|

| Change in delta | Gamma measures how delta changes as the underlying price moves. |

| Gamma risk | Rapid delta change can become more important near the strike or close to expiration. |

| Volatility assumptions | Changing volatility expectations can move option value in ways delta alone does not explain. |

| Black-Scholes model | Model-based pricing inputs help produce theoretical option values and Greeks. |

FAQ

Is delta the same as probability?

No. Delta is sometimes used as a rough probability shortcut, but it is not a fixed probability of expiring in the money, a probability of profit, or a guaranteed payoff estimate.

Can option delta be negative?

Yes. Put options usually have negative delta because their value generally rises when the underlying price falls. Position direction also matters because a short option has the opposite exposure of a long option.