Gamma is an options Greek that measures how much an option’s delta changes when the underlying price changes. It helps show how quickly an option’s directional exposure can accelerate, especially near the strike or near expiration. Gamma does not predict profit, show liquidity conditions, or replace analysis of premium, volatility, exercise or assignment handling, and position risk.

Key Points About Option Gamma

- Gamma measures the rate of change in delta, not the option’s total profit or loss.

- A higher gamma value means delta can change faster as the underlying price moves.

- Gamma is often most sensitive when an option is near the strike price and when expiration is approaching.

- Long gamma and short gamma describe different exposure behavior, but neither label is automatically good or bad.

- Gamma is a model-based exposure measure; it does not fully capture liquidity, bid-ask spreads, implied volatility changes, time decay, margin, collateral, or contract handling.

What Gamma Means in Options

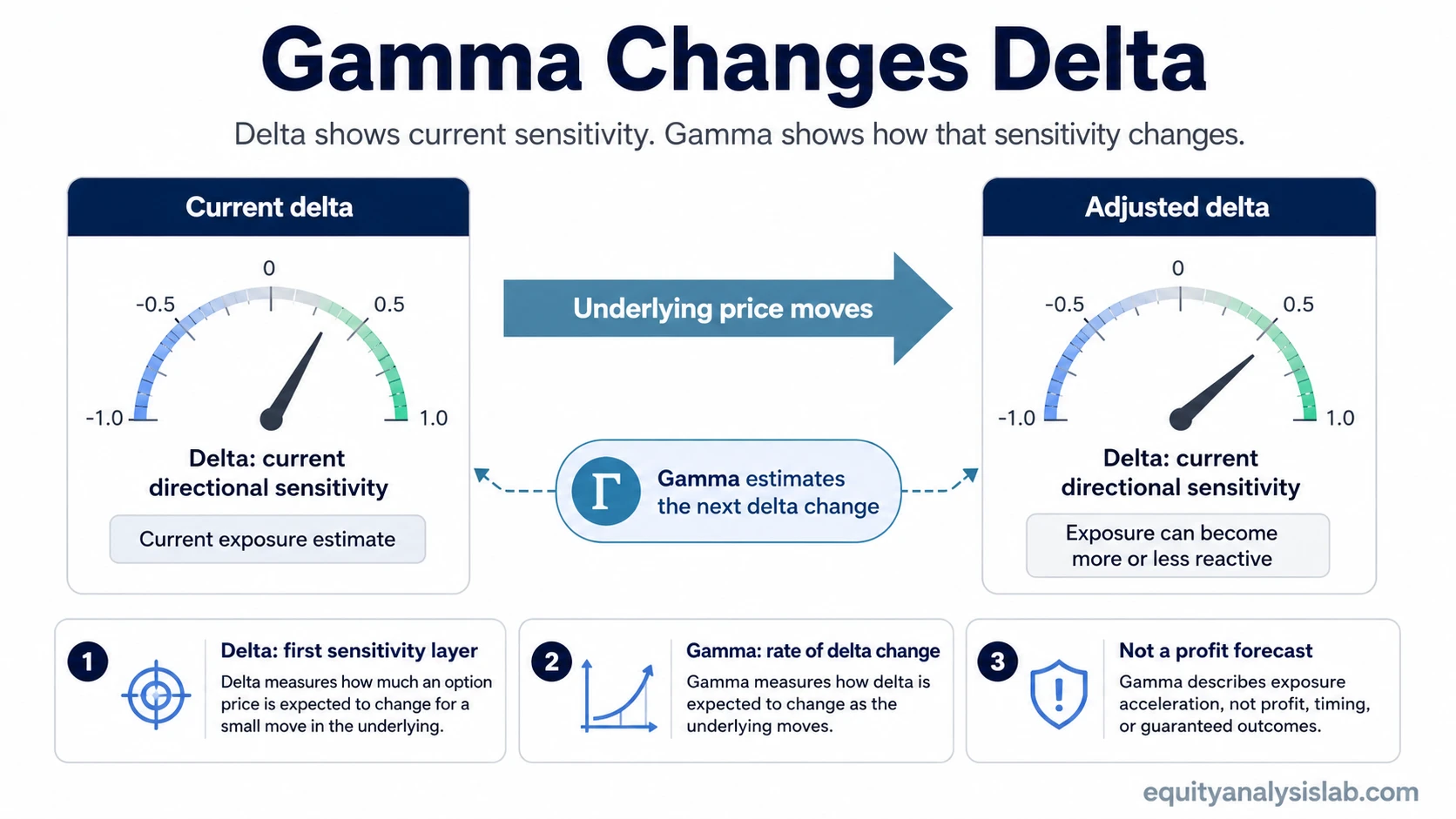

Gamma measures how quickly an option’s delta changes as the underlying price changes. If delta describes the option’s first layer of directional sensitivity, gamma describes how that sensitivity can speed up or slow down.

An option with low gamma may have a delta that changes gradually. An option with high gamma may have a delta that changes more quickly, so the position’s exposure to the underlying can shift over a shorter price move.

That makes gamma most useful as an exposure-acceleration measure. It does not say that the underlying will move, that the option will be profitable, or that a position is suitable for a specific investor.

How Gamma Relates to Delta

Delta estimates how much an option’s price may change for a small move in the underlying price, before other variables are considered. Gamma estimates how much that delta may change after the underlying moves.

The useful distinction is simple: delta measures current directional sensitivity, while gamma measures how unstable or reactive that sensitivity may become. A call option with a delta of 0.40 does not necessarily keep that same delta if the underlying price rises or falls. Gamma helps estimate the next change in delta.

This relationship is why gamma matters most when exposure is changing quickly. It is less about the current delta number and more about how fast that number may adjust as price moves.

Simple Gamma Example

Assume an option has a delta of 0.40 and a gamma of 0.05. If the underlying price rises by $1, the estimated delta may move toward about 0.45, before other variables are considered.

The simplified calculation is:

- Starting delta: 0.40

- Gamma: 0.05

- Underlying move: +$1

- Estimated new delta: about 0.45

This isolates gamma only. Real option value can also change because of implied volatility, time decay, bid-ask spreads, liquidity, interest-rate assumptions, dividends where relevant, and exercise or assignment handling.

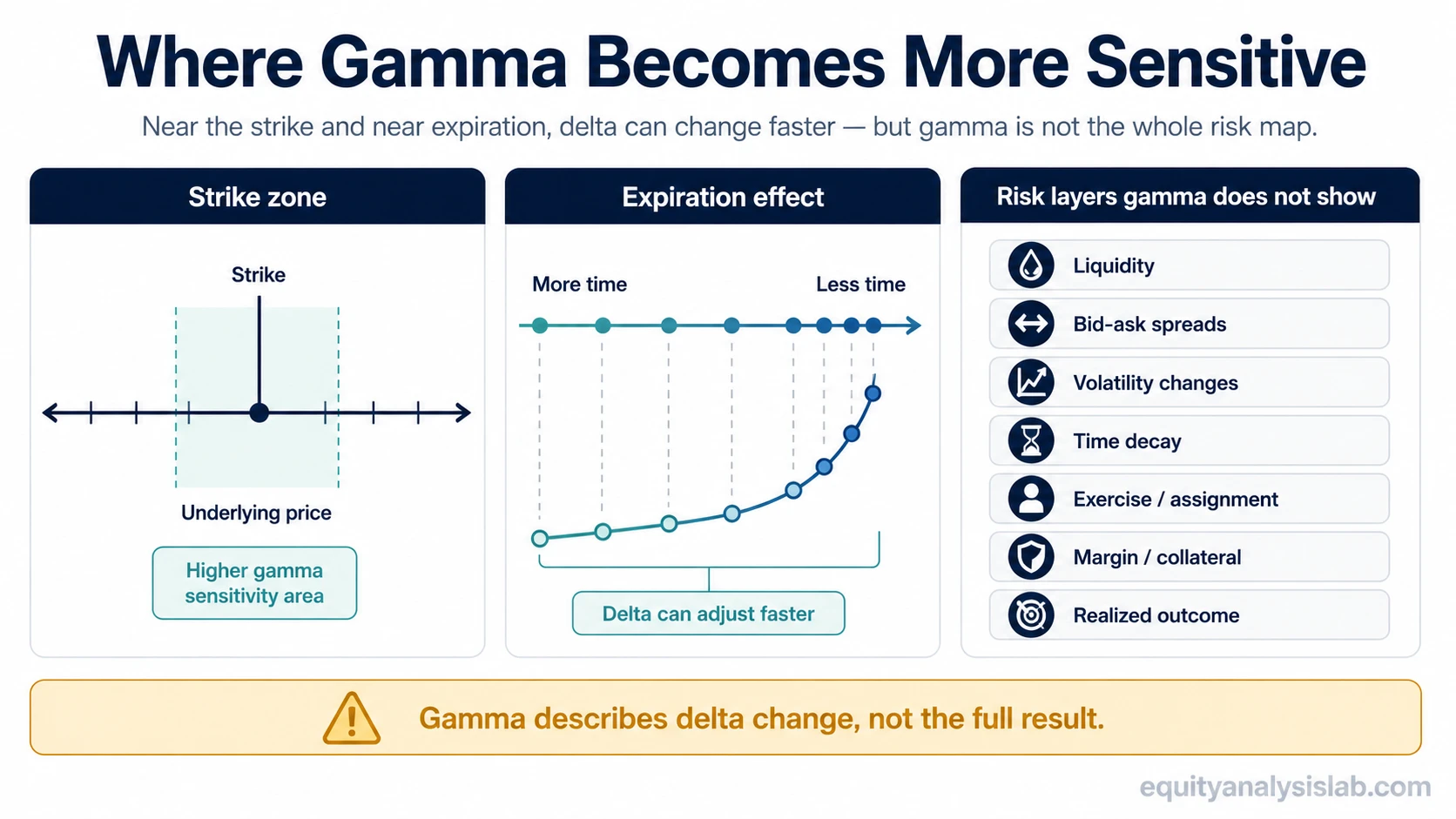

Where Gamma Is Usually Most Sensitive

Gamma often becomes more sensitive when an option is near the money. Near the strike price, a small move in the underlying can meaningfully change whether the option behaves more like an in-the-money contract or an out-of-the-money contract.

Expiration also affects gamma. As expiration approaches, especially in short-dated options, delta can become more reactive around the strike. A small price move near expiration may cause a larger delta adjustment than the same move would have caused earlier in the contract’s life.

That does not mean a near-expiration option is better or worse. It means the exposure can change faster, and the Greek alone does not show the full contract risk.

Long Gamma and Short Gamma

Long gamma generally means the position has positive gamma exposure. When the underlying moves, delta tends to adjust in a way that can increase responsiveness to the direction of the move. Long calls and long puts typically carry positive gamma.

Short gamma generally means the position has negative gamma exposure. Delta can adjust in a way that increases exposure pressure as the underlying moves against the position. Short calls and short puts typically carry negative gamma.

The sign of gamma describes exposure behavior, not a complete position judgment. Premium paid or received, volatility changes, time decay, margin, liquidity, and contract terms can still dominate the realized result.

How to Interpret Gamma Without Overreading It

Gamma is useful because it shows where delta may become unstable. The mistake is treating that instability as a forecast, signal, or complete risk answer.

| Gamma element | What it helps interpret | What it does not prove |

|---|---|---|

| Gamma value | How fast delta may change as the underlying moves | Whether the option position will be profitable |

| Near-the-money gamma | Why exposure can shift quickly near the strike | That price will move through the strike |

| Expiration sensitivity | Why short-dated options can become more reactive | That a short-dated option is suitable for a specific objective |

| Long or short gamma sign | Whether delta change may help or hurt the position as price moves | Whether the position should be opened, held, adjusted, or closed |

| Model Greek output | A structured estimate of exposure under model assumptions | Real liquidity, spread cost, assignment or exercise handling, margin, collateral, or realized outcome |

What Gamma Does Not Show

Gamma is not a complete option-risk map. It isolates one part of the option’s exposure profile: the change in delta as the underlying price changes.

Gamma does not fully show liquidity, bid-ask spreads, order execution, margin or collateral requirements, implied-volatility changes, time decay effects in isolation, early exercise or assignment handling, tax effects, or the final result of a real position.

This is especially important when gamma is read near expiration. A contract may show high gamma, but the position can still be affected by fast theta decay, changing volatility, wide spreads, poor liquidity, or contract-specific settlement and exercise rules.

Gamma Versus Gamma Exposure

Option gamma and gamma exposure are related terms, but they describe different levels of options analysis. Gamma is the Greek attached to an option contract. Gamma exposure, often shortened to GEX, usually refers to broader positioning analysis built from options market data.

At the contract level, gamma describes how delta changes as the underlying moves. GEX, gamma flip, call wall, and put wall analysis belong to a different trading-application layer and should not replace the contract-level meaning of gamma.

Gamma in Pricing Models

Gamma can be estimated inside option-pricing models. In that context, it is part of a theoretical framework rather than a direct trading outcome. A model can organize assumptions, but it cannot remove the uncertainty created by market prices, liquidity, volatility changes, or contract handling.

The Black-Scholes model is one common framework for theoretical option pricing, but gamma should still be read as a sensitivity estimate rather than as a complete explanation of future profit or loss.

Related Concepts

Gamma is easiest to understand after delta because gamma measures how delta changes. Gamma risk is the position-level problem created when fast delta changes affect option exposure. Implied volatility and pricing models also matter because gamma does not isolate every force that changes an option’s market value.

Gamma Option FAQ

Is high gamma good or bad?

High gamma is neither good nor bad by itself. It means delta can change faster. Whether that helps or hurts depends on the position structure, premium, volatility, liquidity, time to expiration, and contract handling.

How is gamma different from delta?

Delta estimates an option’s price sensitivity to a move in the underlying. Gamma estimates how that delta changes as the underlying moves.

Does gamma predict profit?

No. Gamma describes exposure change. Realized results still depend on premium, liquidity, bid-ask spread cost, volatility changes, execution, and contract handling.

When is gamma usually most noticeable?

Gamma is often most noticeable near the strike price and near expiration. The interpretation still depends on the contract, implied volatility, liquidity, and position structure.