Options Greeks and pricing belong together because an option’s price is shaped by inputs, while the Greeks describe how sensitive that price may be to changes in those inputs. The topic separates model inputs, price sensitivity, volatility, time decay, liquidity context, and contract-boundary concepts so the reader can choose the correct next route.

Start with the pricing side if the question is about what shapes theoretical option value. Start with the Greeks if the question is about how an option may respond when the underlying price, time, volatility, rates, or other assumptions change. The distinction matters because a pricing model can estimate value from inputs, while a Greek measures sensitivity around a set of assumptions.

What Options Greeks and Pricing Covers

Options pricing concepts are easier to navigate when model inputs, Greek sensitivities, volatility, time decay, liquidity context, and contract mechanics are separated clearly. The starting point depends on whether the question is about theoretical value, sensitivity to one input, or contract-level mechanics.

Core distinction: option pricing inputs describe what goes into the value estimate; Greeks describe how that value may change when one input changes, assuming the rest of the model framework is held in context.

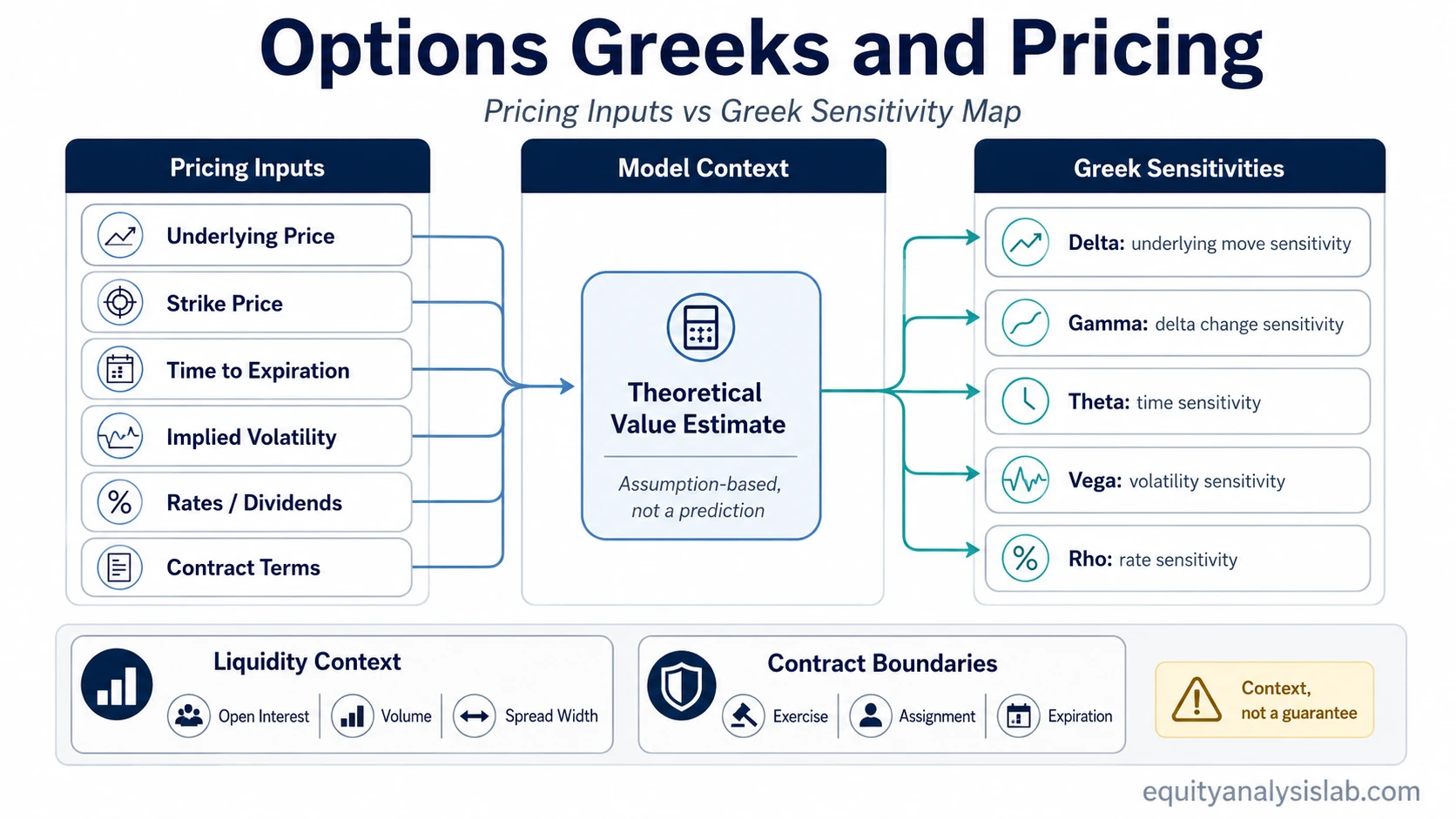

Pricing Inputs vs Greek Sensitivities

Option value is affected by the underlying price, strike price, time to expiration, volatility expectations, interest rates, dividends where relevant, and contract terms. A pricing model organizes those inputs. Greeks then translate parts of that model into sensitivity measures.

| Question | Concept type | Best starting point |

|---|---|---|

| What inputs shape theoretical option value? | Pricing model | Black-Scholes model |

| How does the option respond when the underlying moves? | Directional sensitivity | Delta and gamma |

| How does time affect the option premium? | Time and expiration sensitivity | Theta and time decay |

| How does expected volatility affect option value? | Volatility sensitivity | Vega, implied volatility, and volatility smile |

| How much do rates matter in the model? | Rate sensitivity | Rho |

| How should trading activity and open contracts be interpreted? | Liquidity and participation context | Open interest and volume vs open interest |

Which Options Greek or Pricing Concept to Read First

If the question is how a model estimates theoretical option value, begin with the Black-Scholes model. That page belongs before individual Greeks when the reader needs model inputs, theoretical value, and the relationship between underlying price, strike, time, volatility, rates, and dividends.

If the question is about movement in the underlying, start with delta, then use gamma to understand how delta itself can change. When the confusion is specifically between those two measures, use the delta vs gamma comparison instead of treating both as interchangeable directional labels.

If the question is about time, start with theta. If the reader is trying to understand why an option can lose value as expiration approaches, use the theta decay explained route for a more applied time-decay explanation.

If the question is about volatility, begin with implied volatility and vega. Implied volatility explains the market expectation embedded in option prices, while vega describes sensitivity to changes in that expectation. For event-driven volatility compression, route to IV crush.

If the question is about participation, liquidity context, or whether contract activity is meaningful, open interest is the better starting point. For the common confusion between contract count and trading activity, use the volume-vs-open-interest route rather than treating both as the same liquidity signal.

How Option Price, Greeks, Volatility, and Expiration Fit Together

A simple route example can clarify the sequence. If an option premium changes while the underlying stock barely moves, the explanation may not be delta. The change could come from implied volatility, time decay, spread width, or a shift in the assumptions used by the market. In that case, the better path is implied volatility, vega, and theta before returning to directional Greeks.

If an option premium changes sharply during an underlying move, delta and gamma become more relevant. Delta helps frame the first-order sensitivity to the underlying price. Gamma helps explain why that directional exposure can change as the underlying moves closer to or farther from the strike.

If the question is about contract mechanics rather than sensitivity, route out of the Greeks-and-pricing path. Start with option premium for the paid price of the contract. Use strike price and expiration date as the next core mechanics routes before turning the question into a Greek sensitivity issue.

Comparison Routes for Common Confusion

Some options questions are not solved by reading one definition. They require a distinction between nearby concepts. Use the comparison route when two terms sound similar but answer different questions.

| Confusion | Use this route | Why it helps |

|---|---|---|

| Delta and gamma | Delta vs gamma | Separates directional sensitivity from the rate of change in directional sensitivity. |

| Gamma exposure near important price areas | Gamma risk | Explains why sensitivity can become less stable as price, strike, and expiration interact. |

| Implied volatility and historical volatility | Implied volatility vs historical volatility | Separates forward-looking option pricing expectations from observed past price movement. |

| Options Greeks as a broad overview | Options Greeks explained | Provides a broader starting point when the reader does not yet know which Greek matters. |

Scope Boundaries

The Greeks-and-pricing path does not fully explain complete options strategies, payoff diagrams, position management, rolling decisions, entry timing, exit timing, or option suitability. Those topics require a different page role because they move from concept understanding into strategy, risk management, or broker-specific execution.

Exercise and assignment also sit outside the main Greeks-and-pricing route. When the question is about what it means to use the option contract or receive an assignment outcome, use exercise option or assignment instead of treating the issue as a Greek sensitivity question.

Limitations of Greeks and Pricing Models

Greeks are theoretical sensitivity measures. They do not guarantee exact option premium changes, and they should not be read as predictions. Model values depend on assumptions and inputs, while actual market prices can also reflect liquidity, spread width, volatility expectations, exercise and assignment boundaries, dividend assumptions, rates, and changing conditions.

Open interest and volume can help with tradability and interpretation, but they are not theoretical pricing inputs in the same way as volatility, time, strike, underlying price, rates, and dividends. They belong in the liquidity and participation layer, not in the core model-input layer.

FAQ

Are options Greeks the same as option pricing inputs?

No. Pricing inputs are the variables used to estimate or interpret option value. Greeks describe how sensitive that value may be to changes in those variables.

Which Greek should I learn first?

Delta is often the first Greek introduced because it relates option value to movement in the underlying. After that, gamma, theta, vega, and rho explain how that sensitivity changes through price, time, volatility, and rates.

Do Greeks predict the exact option price?

No. Greeks are model-based sensitivity measures. They can help interpret how option value may respond to changing inputs, but they do not guarantee exact premium changes.

Is open interest an option pricing input?

No. Open interest helps interpret contract participation and liquidity context. It is not a theoretical pricing input in the same way as underlying price, strike, time, volatility, rates, and dividends.