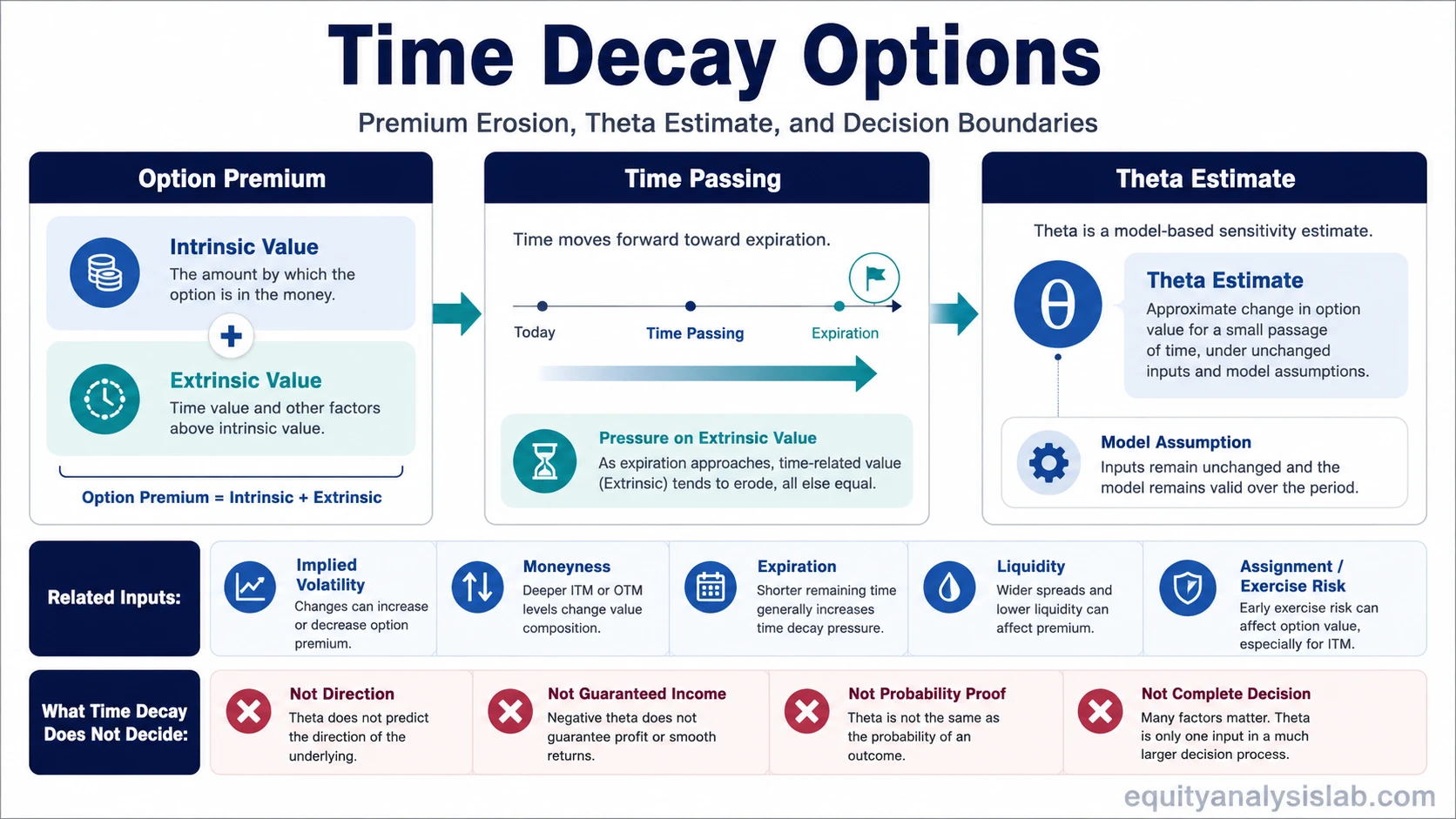

Time decay options describe how the passage of time can reduce an option’s premium, mainly through the extrinsic value portion of the contract. Theta is the model-based estimate of that time sensitivity, but it is not the same as a guaranteed daily change in premium or a full position-quality test.

Definition: Time decay in options is the loss of time-related value as an option moves closer to expiration, assuming other pricing inputs remain unchanged. It affects the part of premium connected to time, uncertainty, volatility expectations, and remaining optionality.

The practical distinction is that time decay describes the pressure from time passing, while theta estimates that pressure inside a pricing model. Actual option premium can still change because the underlying price moves, implied volatility changes, bid-ask spreads widen, or exercise and assignment risks become more relevant.

Key Points

- Time decay describes how time passing can reduce an option’s extrinsic value.

- Theta estimates that sensitivity under model assumptions, not as a fixed cash amount.

- Decay usually becomes more noticeable as expiration approaches, especially around at-the-money strikes.

- Implied volatility, price movement, liquidity, and assignment or exercise risk can change the actual premium outcome.

- Time decay is useful context, not a direction forecast or a complete options decision.

What Time Decay Means in Options

An option has value because it may finish with economic value before or at expiration. Part of that value may come from intrinsic value, and part may come from extrinsic value. Time decay focuses on the extrinsic portion because the right to wait becomes less valuable as the expiration date gets closer.

A call or put can lose time value even if the underlying price does not move much. That does not mean the total premium must decline every day in a straight line. The premium still reflects several inputs at once, so time decay is best treated as one pressure inside the contract rather than as a full explanation of the price.

Time decay and theta are closely related but not identical. Time decay is the concept. Theta is the Greek used to estimate how much the option’s theoretical value may change as time passes, usually with other inputs held constant.

How Time Decay Affects Option Premium

Option premium can be separated into components. Time decay mainly works through extrinsic value, while intrinsic value depends on whether the option is already in the money and by how much.

| Premium component | What it represents | How time decay relates |

|---|---|---|

| Intrinsic value | The value that exists when an option is in the money. | Time decay does not directly create intrinsic value or remove it. Intrinsic value changes mainly with the underlying price relative to the strike. |

| Extrinsic value | The additional premium paid for time, uncertainty, volatility expectations, and remaining optionality. | Time decay mainly reduces this component as expiration approaches, all else equal. |

| Total premium | The market price of the option contract. | Total premium may rise, fall, or stay resilient because price movement, implied volatility, rates, dividends, liquidity, and demand can offset or amplify decay pressure. |

The most important boundary is that time decay does not evaluate the whole position. A contract may lose extrinsic value while the underlying price movement still changes the total premium in the opposite direction.

Time Decay, Theta, and Pricing Assumptions

Theta translates time decay into a sensitivity estimate. If an option has a negative theta value, the model is estimating that the option’s theoretical value may decline as one day passes, with other inputs unchanged. Long option positions commonly show negative theta, while short option positions may show positive theta, but that framing can become misleading if it is treated as a guaranteed result.

Pricing models need assumptions. The Black-Scholes model is one important reference point for understanding how time, volatility, price, strike, rates, and expiration can interact in theoretical option pricing.

The “other inputs unchanged” condition matters. If implied volatility rises, it can support extrinsic value even while time passes. If the underlying price moves sharply, directional exposure can dominate the time effect. If liquidity becomes poor, the observable premium may be affected by wider spreads rather than by clean theoretical decay alone.

Why Time Decay Is Not Usually Linear

Time decay is often described as accelerating near expiration. That general idea is useful, but it should not be converted into a precise curve for every contract. The pattern depends on moneyness, implied volatility, remaining time, and the option’s sensitivity profile.

At-the-money options often show the most visible time-value sensitivity because small movements can still change whether the option finishes in or out of the money. Deep in-the-money options may have more intrinsic value and less relative extrinsic value. Far out-of-the-money options may have low premium, but the remaining extrinsic value can still change quickly if volatility expectations or price movement shift.

Near expiration, premium behavior can also become harder to interpret because exposure can change rapidly. Time decay describes premium erosion, while near-expiration gamma risk concerns how quickly directional exposure can change as the underlying price moves.

What Time Decay Can Estimate vs What It Cannot Decide

A useful time decay reading separates sensitivity from decision quality. Time decay can help estimate how premium may respond to time passing, but it cannot decide whether the full option position is attractive, properly sized, liquid, or aligned with the investor’s risk constraints.

| Time decay can help estimate | Time decay cannot decide |

|---|---|

| How the extrinsic value portion may decline as expiration gets closer. | Whether the underlying price will rise, fall, or stay range-bound. |

| How theta may approximate time sensitivity under model assumptions. | Whether the option position has favorable total risk and reward. |

| Why shorter-dated options may behave differently from longer-dated options. | Whether implied volatility, spread width, or liquidity conditions make the contract usable. |

| Why at-the-money contracts may show visible time-value pressure. | Whether assignment, exercise, payoff shape, or portfolio exposure has been reviewed. |

This boundary prevents a common mistake: treating theta as if it were a fixed income stream or a guaranteed daily cost. It is a sensitivity estimate inside a moving set of pricing inputs.

A Simple Time Decay Scenario

Example: Two call options have the same underlying, the same strike, and similar moneyness, but one expires in two weeks while the other expires in three months. The longer-dated option usually carries more extrinsic value because there is more time for the underlying price, volatility expectations, and market conditions to change.

As expiration approaches, the shorter-dated option may lose extrinsic value faster if the underlying price remains near the same area and implied volatility does not rise. The longer-dated option may still lose time value, but the effect may be less concentrated because more optionality remains.

The scenario remains incomplete without the other inputs. A rise in implied volatility could support premium. A strong underlying price move could overwhelm the time effect. A wide bid-ask spread could make the observed mark less reliable. For short options, assignment and exercise conditions may matter before expiration, not only at the final date.

Related Options Pricing Concepts

Time decay sits inside a wider options pricing map. It should be separated from Greeks and risk concepts that describe different sensitivities.

| Concept | Main question it answers | Relationship to time decay |

|---|---|---|

| Time decay | How does time passing pressure extrinsic value? | The core concept for this contract feature. |

| Theta | How does the model estimate time sensitivity? | The Greek estimate associated with time decay. |

| delta sensitivity | How does premium respond to a change in the underlying price? | Price sensitivity can offset or dominate time decay. |

| how delta can change as price moves | How quickly can directional exposure change? | Near expiration, changing exposure can interact with time decay but remains a separate risk dimension. |

| Implied volatility | How much expected movement is being priced into the option? | Rising volatility expectations can support extrinsic value even while time passes. |

| Payoff and exercise mechanics | What happens if the option is held, exercised, assigned, or expires? | Time decay does not replace payoff review or contract-mechanics review. |

Common Mistakes and Limitations

Limitation: Time decay does not forecast direction, prove probability of profit, guarantee income, guarantee loss, or remove the need to review payoff shape, liquidity, volatility, assignment, exercise, and portfolio exposure.

A common mistake is reading positive theta as if it automatically means a safer or superior position. A short option can appear to benefit from time passing while still carrying large adverse movement risk, early assignment risk, spread risk, or volatility risk.

Another mistake is ignoring implied volatility. If volatility expectations rise enough, the option’s extrinsic value may hold up or increase despite time passing. The result can look confusing when time decay is treated as the only input.

Liquidity also matters. A theoretical theta estimate may look precise, but a wide bid-ask spread can make real execution and valuation less clean. Time decay is most useful when it is interpreted with the option chain, moneyness, expiration, volatility, and the full payoff profile.

FAQ

What is time decay in options?

Time decay is the reduction in an option’s time-related value as expiration approaches. It mainly affects extrinsic value, assuming other pricing inputs remain unchanged.

Is time decay the same as theta?

No. Time decay is the concept of time-related premium erosion. Theta is the Greek that estimates how much theoretical option value may change as time passes under model assumptions.

Does time decay always help option sellers?

No. Positive theta can be favorable to a short option only in a narrow sense. Price movement, volatility changes, liquidity, assignment, exercise, and payoff risk can still dominate the outcome.

Why can an option gain value even when time passes?

An option can gain value if other inputs move enough to offset time decay. A favorable underlying price move or a rise in implied volatility can support premium despite less time remaining.