Gamma risk is the risk that an option’s delta exposure can change as the underlying security moves, especially when the option is near the strike price and close to expiration.

A high gamma reading can make a starting delta less stable. That does not make gamma risk a direction forecast, a guaranteed option price change, or a complete measure of position risk.

Core limitation: static delta, premium paid or received, and expiration payoff diagrams can miss how exposure changes before expiration. Gamma risk is mainly about path sensitivity, not just the final expiration line.

Key Points

- Gamma risk describes changing options delta exposure as the underlying price moves.

- The effect can become more important near the strike and closer to expiration.

- Starting delta is an estimate, not a fixed exposure map.

- Payoff charts can simplify expiration outcomes while hiding pre-expiration path risk.

- Greek readings are theoretical estimates, not guarantees of option price behavior.

What Gamma Risk Means in Options

Gamma risk begins with the relationship between gamma and option delta. Delta estimates how much an option’s theoretical price may change for a $1 move in the underlying security, all else equal. Gamma estimates how much that delta may change after the underlying moves, all else equal.

The risk appears when the starting delta is treated as though it will stay stable. If gamma is high, the option’s exposure can adjust quickly as the underlying moves, so the same contract can behave differently after a relatively small price change.

For an investor learning options mechanics, the practical issue is not whether gamma is good or bad. The issue is whether a current exposure estimate can become stale before expiration.

Why Gamma Risk Can Increase Near Strike and Expiration

Gamma risk is often more noticeable when an option is near the strike price. Around that area, small moves in the underlying can have a larger effect on whether the option behaves more like an in-the-money or out-of-the-money contract.

Time to expiration also matters. As expiration approaches, especially in very short-dated contracts such as 0DTE options, the option’s sensitivity can change faster. That does not make a short-dated option a better or worse instrument by itself. It only means that a static reading may become less reliable more quickly.

Implied volatility, liquidity, bid-ask spreads, and contract activity can also affect how theoretical Greek readings translate into real option pricing and execution conditions. Gamma risk should therefore be read as one part of an options-risk picture, not as a complete answer.

How Delta Exposure Can Change After a Price Move

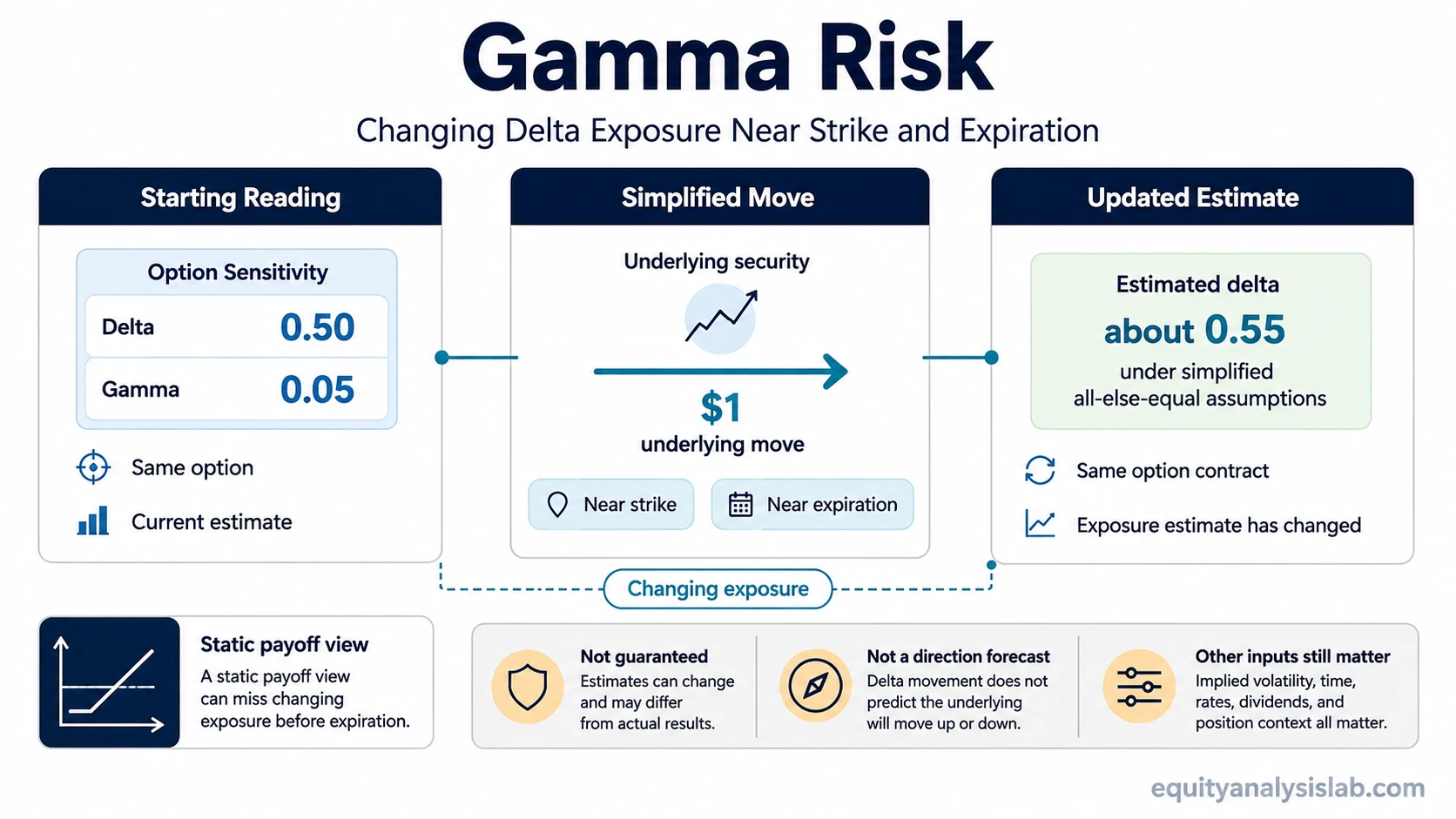

Consider a simplified same-option reading. Suppose an option has a starting delta of 0.50 and a gamma of 0.05. Under simplified all-else-equal assumptions, a $1 move in the underlying security could move the estimated delta toward about 0.55.

That does not mean the option price is guaranteed to move by a fixed amount. Other inputs can change at the same time, including implied volatility, time decay, bid-ask spreads, and liquidity. The example only isolates the gamma-to-delta relationship.

Simple gamma risk example: an option that begins with 0.50 delta may look like roughly half-dollar sensitivity to a $1 underlying move. If gamma is 0.05, the next delta estimate may move toward 0.55 after that $1 move, under simplified all-else-equal assumptions. The exposure estimate has changed before expiration, even though the contract is the same.

Gamma Risk Inputs and Boundaries

Gamma risk becomes easier to read when the moving parts are separated into the conditions that change exposure interpretation rather than trade decisions.

| Condition | What Can Change | Why It Matters |

|---|---|---|

| Underlying price move | Delta can adjust after the move | A starting delta may no longer describe the current exposure estimate. |

| Strike proximity | Near-the-money options can show larger sensitivity shifts | Small underlying moves may change how the contract behaves relative to the strike. |

| Time to expiration | Shorter-dated contracts can become more sensitive | Exposure can change quickly as the final exercise boundary approaches. |

| Implied volatility | Theoretical option value can move even if the underlying move is simple | Greek estimates are model-based and can shift with volatility assumptions. |

| Liquidity and open interest | Practical pricing and transaction conditions can differ from theoretical estimates | Thin markets or wide spreads can make clean model readings harder to apply. |

| Assignment or exercise boundary | Short options and expiring options can face contract-mechanics risk | Expiration payoff diagrams do not capture every pre-expiration path or mechanical outcome. |

Why Payoff Charts and Starting Delta Can Mislead

An expiration payoff chart is useful for showing the final payoff shape at expiration, but it is not a full map of what can happen before expiration. Gamma risk exists because the contract can move through different exposure states before reaching the final payoff line.

Premium received or premium paid also does not fully describe changing exposure. A short option may have a defined premium received, but the exposure path before expiration can still change as delta adjusts. A long option may have premium at risk, but the speed and direction of delta change still depend on price movement, time, volatility, and moneyness.

Common mistake: reading the first delta, the expiration payoff line, or the initial premium as a complete risk map. Those figures are useful, but they can understate how quickly exposure can change when gamma is high.

Gamma Risk vs Gamma

The gamma Greek is the sensitivity measure. It estimates how much delta may change for a $1 move in the underlying security, all else equal. Gamma risk is the interpretation problem created when that changing delta exposure matters for the option holder or option seller.

Gamma explains a model-based rate of change. Gamma risk focuses on the limitation of relying on a static exposure reading when the contract’s sensitivity can shift quickly.

Short distinction: gamma is the Greek. Gamma risk is the exposure instability that can appear when gamma makes delta change faster than a static reading suggests.

Common Mistakes When Reading Gamma Risk

One mistake is treating gamma as a forecast. Gamma does not predict the next direction of the underlying security. It only describes how delta may change if the underlying moves.

Another mistake is treating starting delta as fixed exposure. A 0.50 delta is a current estimate, not a promise that the option will keep behaving like a 0.50-delta contract after price, time, or volatility changes.

A third mistake is reading short option risk only from the expiration payoff diagram. The expiration line may look simple, while the pre-expiration path can become more sensitive as the underlying moves near the strike.

Model Context and Limits

Gamma, delta, and other Greeks are theoretical sensitivity estimates. The Black-Scholes model is one common framework used to explain how option value can relate to inputs such as underlying price, strike, time, volatility, and rates.

Model context matters because gamma risk is not visible from one input alone. A cleaner reading compares the Greek estimate with moneyness, time remaining, volatility assumptions, liquidity conditions, and the contract’s exercise or assignment mechanics.

A narrow interpretation is more accurate: gamma risk warns that option exposure can change before expiration. It does not decide whether an option is suitable, attractive, or worth using.

FAQ

What is gamma risk in options?

Gamma risk is the risk that an option’s delta exposure changes as the underlying security moves. It is most relevant when gamma is high, often near the strike price and closer to expiration.

Is gamma risk the same as gamma?

No. Gamma is the Greek that estimates the change in delta after a $1 move in the underlying security, all else equal. Gamma risk is the practical issue created when that changing delta exposure matters before expiration.

Why can gamma risk be higher near expiration?

Near expiration, an option has less time for the final payoff boundary to change. When the contract is also near the strike, small underlying moves can cause faster changes in estimated delta exposure.

Does gamma risk predict the direction of the underlying security?

No. Gamma risk does not predict direction. It describes how option exposure can change if the underlying moves, while other inputs such as volatility, time, and liquidity may also affect the option’s price.