Portfolio strategies are the rules and choices that shape how a portfolio is built, reviewed, and adjusted. The first useful question is not which model allocation looks familiar. It is what remains unresolved: target exposure, implementation style, concentration, cash role, drift, or review discipline.

Definition: A portfolio strategy is a structured approach for deciding how assets, weights, risk limits, cash, and review rules work together inside an investment portfolio.

Portfolio strategies sit between core portfolio construction concepts and specific implementation choices. Asset allocation sets the broad exposure. Diversification checks whether risk is spread across genuinely different drivers. Rebalancing deals with drift after weights move. A strategy connects those pieces into a repeatable portfolio process.

Key Points

- Portfolio strategies should start with the problem being solved, not with a preselected model portfolio.

- Target weights matter, but overlap, concentration, cash, drift, and review rules often decide whether the structure behaves as expected.

- A simple portfolio can still need review if holdings overlap heavily or one position, sector, or asset class dominates the risk.

- Gold, high-conviction positions, ETFs, and simple portfolio templates belong in different strategy paths because they answer different portfolio questions.

Portfolio Strategies Are Not One Model Portfolio

A portfolio strategy should answer how the portfolio will be organized and reviewed. It should not skip directly to a fixed mix of stocks, bonds, funds, cash, or alternative assets.

A model allocation can be useful, but it is only one input. Two investors can both hold a 60% equity and 40% bond target while carrying very different risks if one has broad diversified exposure and the other has overlapping funds, large single-stock positions, unused cash, or frequent drift away from target weights.

Scope note: The strategy choice here is about portfolio structure and review logic. It does not decide which security to buy, when to enter a position, or whether a specific fund is suitable.

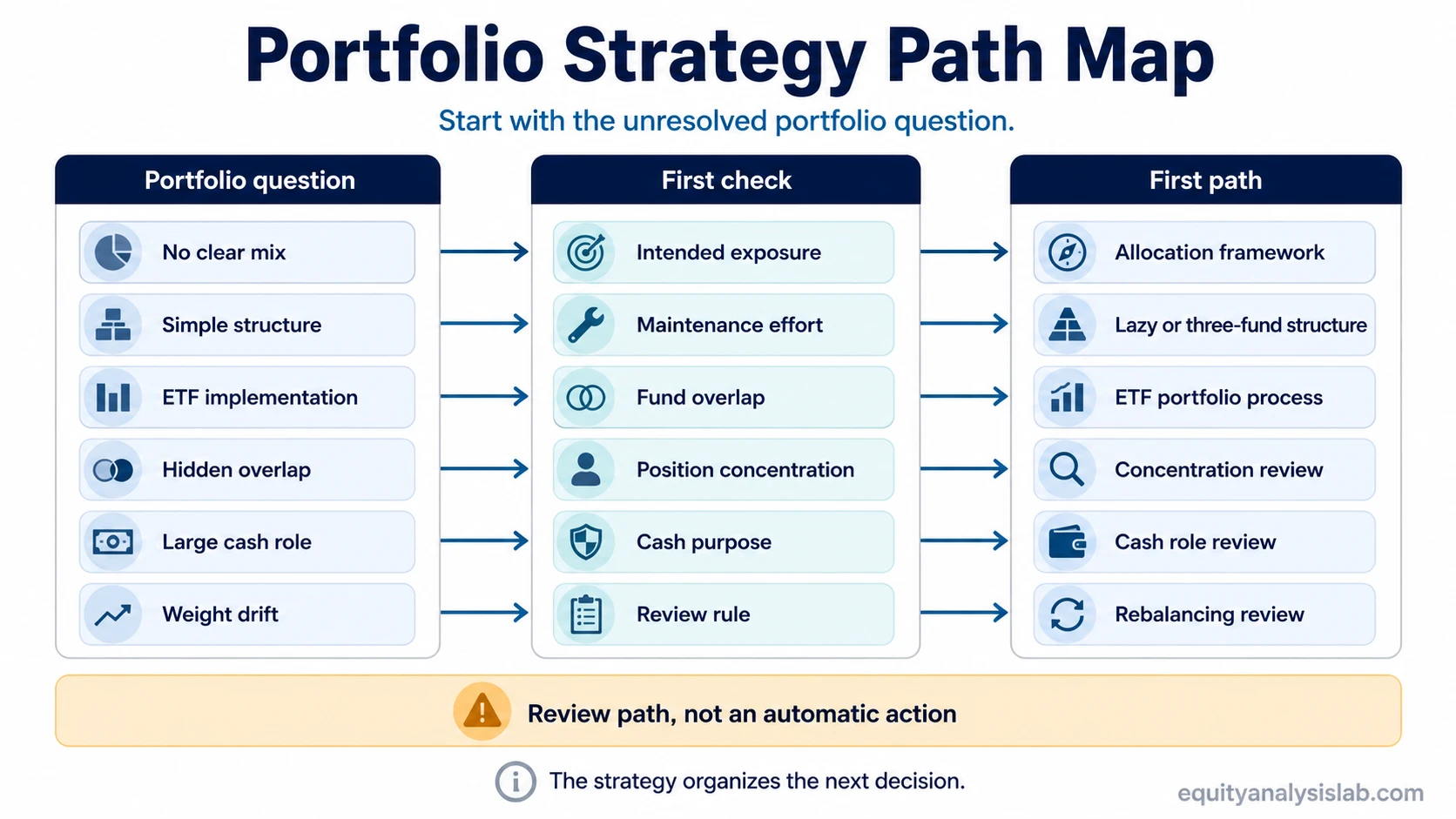

How to Choose the First Portfolio Strategy Path

The first path depends on what is unclear in the current portfolio. A portfolio with no target allocation has a different problem from a portfolio that already has targets but has drifted away from them. A portfolio with many funds can still have a concentration problem if the underlying holdings overlap.

Start with target exposure when the main question is how much belongs in equities, bonds, cash, or other assets.

Move to implementation when target exposure is known but the investor needs a simple fund structure, ETF structure, or long-term template.

Check concentration and overlap when the portfolio looks diversified by number of holdings but risk may still be clustered.

Check drift and review rules when market movement has changed the actual weights away from the intended weights.

Check risk capacity when the strategy could create drawdown, liquidity, or behavioral pressure that the investor may not be able to tolerate.

Portfolio Strategy Decision Table

| Portfolio question | What to inspect first | Possible strategy path | Common mistake |

|---|---|---|---|

| No clear target mix exists | Target allocation, time horizon, and risk capacity | Start with allocation and risk framework concepts before selecting a strategy template | Choosing funds before defining the portfolio role |

| The investor wants a simple long-term structure | Number of funds, asset classes, maintenance effort, and rebalancing needs | Review lazy portfolio, three-fund portfolio, or ETF portfolio construction paths | Assuming simpler means risk-free or maintenance-free |

| The portfolio uses ETFs as the main building blocks | Exposure, overlap, costs, tracking, liquidity, and tax treatment | Use the ETF portfolio construction path | Treating ETF count as diversification without checking underlying exposure |

| The portfolio is concentrated by design | Position size, thesis quality, drawdown tolerance, liquidity, and review rules | Use the high-conviction portfolio path | Confusing conviction with permission to ignore position risk |

| The investor wants a non-stock diversifier | Role of the asset, correlation behavior, inflation sensitivity, volatility, and portfolio size | Use the gold in a portfolio path only for the diversifier question | Adding gold without defining whether it is meant to diversify, hedge, or store value |

| The target weights are known but current weights changed | Portfolio drift, cash flows, transaction costs, taxes, and rebalancing rule | Move into portfolio maintenance and rebalancing review | Treating every drift reading as an automatic transaction |

Where Hidden Portfolio Risk Usually Appears

Hidden risk often appears when a portfolio looks diversified at the surface but the underlying exposures point in the same direction. Several funds can hold the same large companies. Several stocks can depend on the same sector, commodity, currency, interest-rate sensitivity, or earnings cycle. Cash can also change the portfolio if it is large enough to reduce intended exposure or small enough to limit rebalancing flexibility.

Limitation: A portfolio strategy cannot be judged from holdings count alone. The important question is whether the weights, exposures, cash level, and review rules match the intended role of the portfolio.

Overlap and concentration do not automatically make a portfolio wrong. They change what must be monitored. A broad ETF template usually needs exposure and drift review. A high-conviction portfolio usually needs position-size discipline and thesis review. A gold allocation usually needs role clarity because the same holding can be framed as diversification, inflation sensitivity, a potential defensive role, or real-asset exposure.

A Simple Portfolio Strategy Example

An investor holds seven ETFs, so the portfolio appears diversified. A closer look shows that four of the ETFs hold many of the same mega-cap stocks, the cash position has grown after dividends and deposits, and the equity weight is higher than the intended target. The first issue is not whether seven funds are enough. The first issue is exposure overlap, cash role, and drift review.

That situation points toward three questions before choosing a strategy label: whether the target allocation is still valid, whether the holdings create duplicate exposure, and whether the portfolio needs a rebalancing rule. Only after those questions are clear does it make sense to choose between a simple ETF structure, a lazy portfolio approach, a three-fund framework, or a more concentrated strategy.

Which Strategy Fits Each Problem

| Need | Better first path | Why |

|---|---|---|

| A low-maintenance structure | Lazy portfolio | Focuses on simplicity, broad exposure, and periodic review rather than constant adjustment. |

| A compact fund-based structure | Three-fund portfolio | Uses a small number of broad building blocks while still requiring allocation and rebalancing decisions. |

| An ETF-based implementation process | How to build an ETF portfolio | Deals with fund selection, overlap, cost, liquidity, and exposure quality. |

| A concentrated investor thesis | High-conviction portfolio | Requires stronger position-size discipline, thesis monitoring, and downside tolerance. |

| A diversifier outside stocks and bonds | Gold in a portfolio | Requires a defined role before the allocation can be interpreted. |

What Portfolio Strategies Do Not Decide

A portfolio strategy does not determine expected return with certainty, remove downside risk, or prove that a transaction is required. It also does not replace tax review, personal financial planning, security selection, or fund due diligence.

The strategy is a framework for organizing the next decision. A drift reading may start a review. Concentration may require a risk check. Cash may create flexibility or idle exposure. A simple template may reduce complexity but still need maintenance. The useful output is a clearer review sequence, not an automatic instruction.

FAQ

Is a portfolio strategy the same as asset allocation?

No. Asset allocation sets the broad mix of exposures. A portfolio strategy also covers implementation, position size, overlap, cash role, rebalancing discipline, and review rules.

Can a portfolio be diversified if it holds many funds?

Yes, but the number of funds is not enough to prove diversification. The underlying holdings, sector weights, factor exposure, and asset-class behavior matter more than the headline count.

Does a portfolio strategy tell an investor what to buy?

No. A portfolio strategy organizes the decision process. Security selection, fund suitability, tax effects, and personal financial constraints require separate review.