Gold in a portfolio is not a standalone bullish or bearish view on gold. It is a portfolio-construction review of what role gold is meant to play, how the exposure is held, how large it is relative to the rest of the allocation, and what problem it is supposed to solve.

A gold position only becomes useful to evaluate after the investor defines its job. The same exposure can be treated as a diversifier, a real-asset sleeve, a hedge against specific risks, or a source of unwanted concentration depending on the surrounding portfolio. Without that role definition, the discussion usually collapses into a vague question about whether gold is “good” or “bad,” which is not enough for portfolio work.

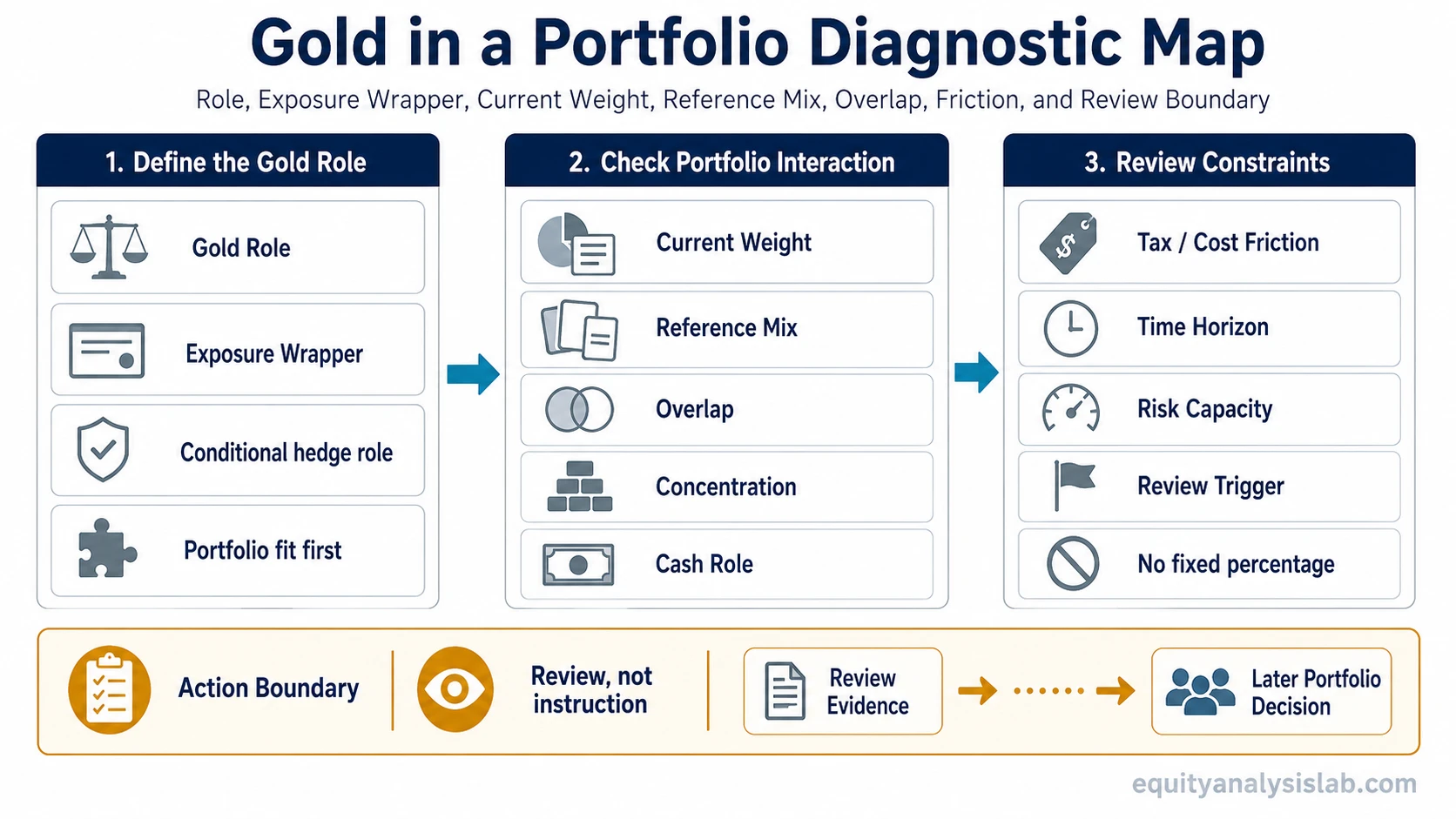

The review should not start with a fixed percentage. It should start with the existing portfolio, the reference allocation, the investor’s time horizon, the acceptable drawdown range, the liquidity need, and the tradeoff between extra resilience and extra complexity.

Key Points

- Gold in a portfolio is a role and exposure question, not a prediction about the gold price.

- Gold may diversify some risks, but it does not automatically protect every portfolio in every market environment.

- The wrapper matters because physical gold, gold ETFs, and gold-related equities do not behave the same way.

- A gold allocation should be reviewed against overlap, concentration, cash needs, friction, time horizon, and risk capacity before any portfolio change.

- There is no universal percentage that fits every investor, portfolio, or objective.

What Gold in a Portfolio Means

Gold in a portfolio means using gold exposure as one part of a broader investment mix. The central question is not whether gold is attractive in isolation, but whether the exposure improves the portfolio’s role balance after considering volatility, liquidity, correlation, costs, and investor constraints.

The starting point is the portfolio’s existing allocation mix. A small gold position inside a highly concentrated equity portfolio has a different meaning from the same position inside a balanced, income-oriented, or cash-heavy portfolio. The position size may look modest as a standalone line item, but its effect depends on what else the investor already owns.

Definition: Gold in a portfolio is a review of gold’s intended role, exposure type, weight, interaction with other holdings, and fit with the investor’s risk and time-horizon constraints.

A useful review separates three questions. First, what role is gold supposed to play? Second, what exact exposure creates that role? Third, does the current weight help the portfolio or create a new source of complexity?

What Gold Can and Cannot Do in a Portfolio

Gold can sometimes behave differently from stocks and bonds, which is why investors often discuss it as a diversifier or risk-offsetting asset. That does not make it a complete hedge. Its behavior can change across inflation regimes, real-rate environments, currency conditions, liquidity stress, and investor positioning.

The portfolio tradeoff belongs inside a broader risk and return review. Gold exposure can reduce one type of portfolio sensitivity while introducing another. It can reduce dependence on corporate earnings, but it can also add an asset that does not produce cash flow. It can help with some stress scenarios, but it can lag or draw down during others.

| Possible Role | What It Can Help Review | Boundary |

|---|---|---|

| Diversifier | Whether portfolio outcomes depend too heavily on stocks, bonds, or one economic regime | Correlation can change, especially during liquidity stress or crowded positioning |

| Inflation-sensitive asset | Whether the portfolio has any exposure that may respond to currency or real-asset concerns | Gold does not track consumer inflation mechanically or consistently over every period |

| Crisis hedge candidate | Whether the portfolio has assets that may behave differently during confidence shocks | A hedge role is scenario-dependent and does not remove drawdown risk |

| Non-cash-flow diversifier | Whether a small non-cash-flow asset changes total volatility or investor behavior | Too large a position can become a source of concentration rather than balance |

The useful question is conditional: what weakness in the current portfolio is gold expected to address, and what new weakness could it introduce?

How to Review Gold Exposure Before Changing Allocation

A gold review works best as a sequence. Skipping directly to a target percentage can hide the real issue: the portfolio may not need gold, may need a different exposure wrapper, or may already contain indirect commodity or real-asset sensitivity through other holdings.

| Review Step | Question to Ask | Why It Matters |

|---|---|---|

| Role | What portfolio problem is gold supposed to address? | Prevents gold from becoming a vague add-on without a defined job |

| Exposure wrapper | Is the exposure physical gold, a fund, futures-linked exposure, or gold-related equities? | Different wrappers can carry different liquidity, cost, tax, tracking, and equity-risk features |

| Current weight | How large is gold exposure as a share of the total portfolio? | Small and large allocations change portfolio behavior differently |

| Reference mix | What is the intended long-term mix before adding or changing gold? | Shows whether the position supports the plan or distracts from it |

| Overlap | Does the portfolio already contain commodity, mining, real-asset, or inflation-sensitive exposure? | Prevents duplicate exposure from being mistaken for new balance |

| Concentration | Would gold become large enough to dominate portfolio behavior? | A hedge can become a concentration risk if the weight grows too large |

| Cash role | Is gold being used for resilience when cash or short-duration assets would serve the need better? | Gold is not the same as liquidity for spending, reserves, or near-term obligations |

| Drift | Has the gold weight moved away from the reference mix? | Separates review discipline from emotional reaction to price movement |

| Friction | What costs, taxes, spreads, storage, or tracking issues apply? | Implementation friction can weaken a theoretically useful role |

| Time horizon | Is the role meant for months, years, or a full investment cycle? | A short horizon can make long-term diversifier logic less reliable |

| Risk capacity | Can the investor tolerate periods when gold does not help? | A hedge that disappoints in the wrong period can still create behavioral risk |

| Review trigger | What event justifies review: drift, portfolio change, liquidity need, or changed objective? | Prevents constant adjustment based only on headlines |

| Action boundary | Does the evidence justify review, or does it justify an actual change? | A review trigger is not automatically an instruction to trade |

Use the sequence as a filter rather than a checklist that forces action. Role comes first, the exposure wrapper comes second, and weight, overlap, friction, time horizon, and risk capacity come after that. A portfolio change belongs only after the evidence shows that the current exposure no longer matches the role.

This sequence keeps the decision tied to portfolio evidence. It also makes clear that reviewing gold exposure is not the same as deciding to increase, reduce, or remove it.

Gold, Diversification, and Hidden Concentration

Gold is often described as a diversifier, but diversification depends on what the position is diversifying away from. A portfolio already exposed to commodity producers, cyclical materials businesses, inflation-sensitive assets, or currency-sensitive holdings may not become as balanced as expected by adding another gold-related position. Gold exposure is not automatically diversifying if the portfolio already has miners, commodity producers, real-asset funds, inflation-sensitive equities, or similar macro sensitivity.

The distinction matters because true portfolio balance is about how holdings interact, not simply how many asset labels appear on the statement. A separate review of how holdings behave together can show whether gold is adding a genuinely different exposure or only repeating an existing risk.

Physical gold, gold ETFs, and gold mining equities can all create gold-related exposure, but they do not carry the same portfolio mechanics. Physical gold brings custody, storage, access, spread, and liquidity considerations. A gold ETF adds fund-wrapper questions such as tracking, expense ratio, trading liquidity, structure, and tax treatment. Gold mining equities add company-level and equity-market risk because the investor owns businesses affected by margins, costs, balance sheets, management, and operating conditions.

| Exposure Type | What the Investor Owns | Main Review Issue |

|---|---|---|

| Physical gold | Direct ownership or stored metal exposure | Storage, insurance, liquidity, spreads, custody, and practical access |

| Gold ETF | A fund structure designed to provide gold exposure through tradable shares | Expense ratio, tracking, liquidity, structure, taxation, and fund-specific mechanics |

| Gold mining equities | Operating businesses linked to gold prices but also affected by company risk | Equity-market beta, margins, management, reserves, costs, jurisdiction, and balance sheet risk |

A Gold ETF may be a convenient exposure wrapper, but it is not the same decision as deciding whether gold belongs in the portfolio at all. The portfolio role comes first; wrapper selection comes after the role is clear.

Gold-related equities require extra caution. A mining stock can rise or fall for reasons that have little to do with the portfolio role an investor expected from gold. That makes mining exposure closer to an equity and business-quality decision than a pure gold-allocation substitute.

A Simple Gold Allocation Review Scenario

Consider a generic investor who holds mostly broad equity funds, a smaller bond sleeve, and a cash reserve. The investor is considering gold because the portfolio feels too dependent on corporate earnings and interest-rate conditions. That concern may be reasonable, but it is not enough to define an allocation.

The review would first ask what role gold is expected to play. If the goal is crisis resilience, the investor should examine how the current portfolio behaved during stress and whether cash needs are already covered. If the goal is inflation sensitivity, the investor should check whether existing holdings already include real-asset or commodity-linked exposure. If the goal is behavioral comfort, the investor should consider whether a gold position would actually reduce the chance of panic decisions or simply add another volatile line item to monitor.

The scenario does not produce a universal percentage. It produces a clearer boundary: gold may be relevant only if it solves a defined portfolio problem without creating a larger overlap, concentration, liquidity, or friction problem.

When Gold in a Portfolio Can Fail as a Framework

Gold becomes a weak portfolio decision when the label sounds diversified but the mechanics do not support the role. The failure is often not that gold is inherently wrong; the failure is that the position was added without a clear job, a size discipline, or a review boundary.

| Failure Condition | How It Shows Up | Review Response |

|---|---|---|

| No defined role | Gold is added because of headlines, fear, or recent price movement | Define the portfolio problem before reviewing size or wrapper |

| Hidden concentration | Gold exposure overlaps with miners, commodity producers, real assets, or inflation-sensitive holdings | Review total exposure, not only the line labeled gold |

| Wrapper mismatch | The investor expects bullion-like behavior but owns equity-like mining exposure | Separate physical, fund, and company-level exposure before evaluating role |

| Oversized allocation | The hedge becomes large enough to drive portfolio results | Check whether gold still reduces portfolio fragility or has become a new risk center |

| Cost or tax friction | Theoretical diversification is weakened by spreads, storage, taxes, expense ratios, or trading costs | Include implementation friction before treating the role as useful |

| Rebalancing conflict | The investor reacts to every move instead of using a review discipline | Separate review triggers from action triggers |

| Time-horizon mismatch | A long-term hedge argument is applied to a short-term liquidity need | Use the actual time horizon, not the asset’s reputation |

| Misunderstood hedge role | Gold is expected to protect against every drawdown or every inflation period | Treat hedge behavior as conditional, not guaranteed |

The strongest version of a gold review is conservative. It does not assume that gold must be included, and it does not assume that gold must be avoided. It asks whether the role is clear, the exposure is understood, the weight is controlled, and the rest of the portfolio still works if gold disappoints.

Related Concepts to Review Next

Gold exposure is easier to judge after the investor defines the role first, then reviews asset allocation, diversification, risk and return, and Gold ETF mechanics in that order. The next useful step is usually not a product search. It is a clearer review of how gold is supposed to interact with the portfolio that already exists.

Asset mix, diversification, and risk tolerance all matter because gold changes the portfolio only through its interaction with other holdings. A position that looks sensible in isolation may be unnecessary, redundant, or too large once the full portfolio is reviewed.

| Concept | Why It Matters for Gold |

|---|---|

| Asset allocation | Shows whether gold supports the intended portfolio mix or distracts from it |

| Diversification | Tests whether gold adds a different exposure or repeats an existing risk |

| Risk and return | Frames the tradeoff between potential resilience, volatility, friction, and opportunity cost |

| Gold ETF | Clarifies fund wrapper mechanics after the portfolio role has been defined |

FAQ

Should you have gold in your portfolio?

Gold may belong in a portfolio when it has a defined role, the exposure type is understood, and the position fits the broader allocation. It should not be added only because of headlines, recent price movement, or a universal allocation rule.

What percentage of a portfolio should be in gold?

There is no fixed percentage that fits every investor. The appropriate review depends on the portfolio’s current mix, existing overlap, time horizon, risk capacity, liquidity needs, costs, taxes, and the specific role gold is expected to play.

Does gold always diversify a portfolio?

No. Gold can diversify some portfolios in some environments, but its correlation and usefulness can change. It may also duplicate existing exposure if the portfolio already includes commodity, mining, real-asset, or inflation-sensitive holdings.

Is a gold ETF the same as owning gold in a portfolio?

No. A gold ETF is one possible exposure wrapper. The portfolio decision is whether gold exposure has a useful role; the wrapper decision is how that exposure is held, with its own liquidity, cost, tracking, tax, and structure considerations.