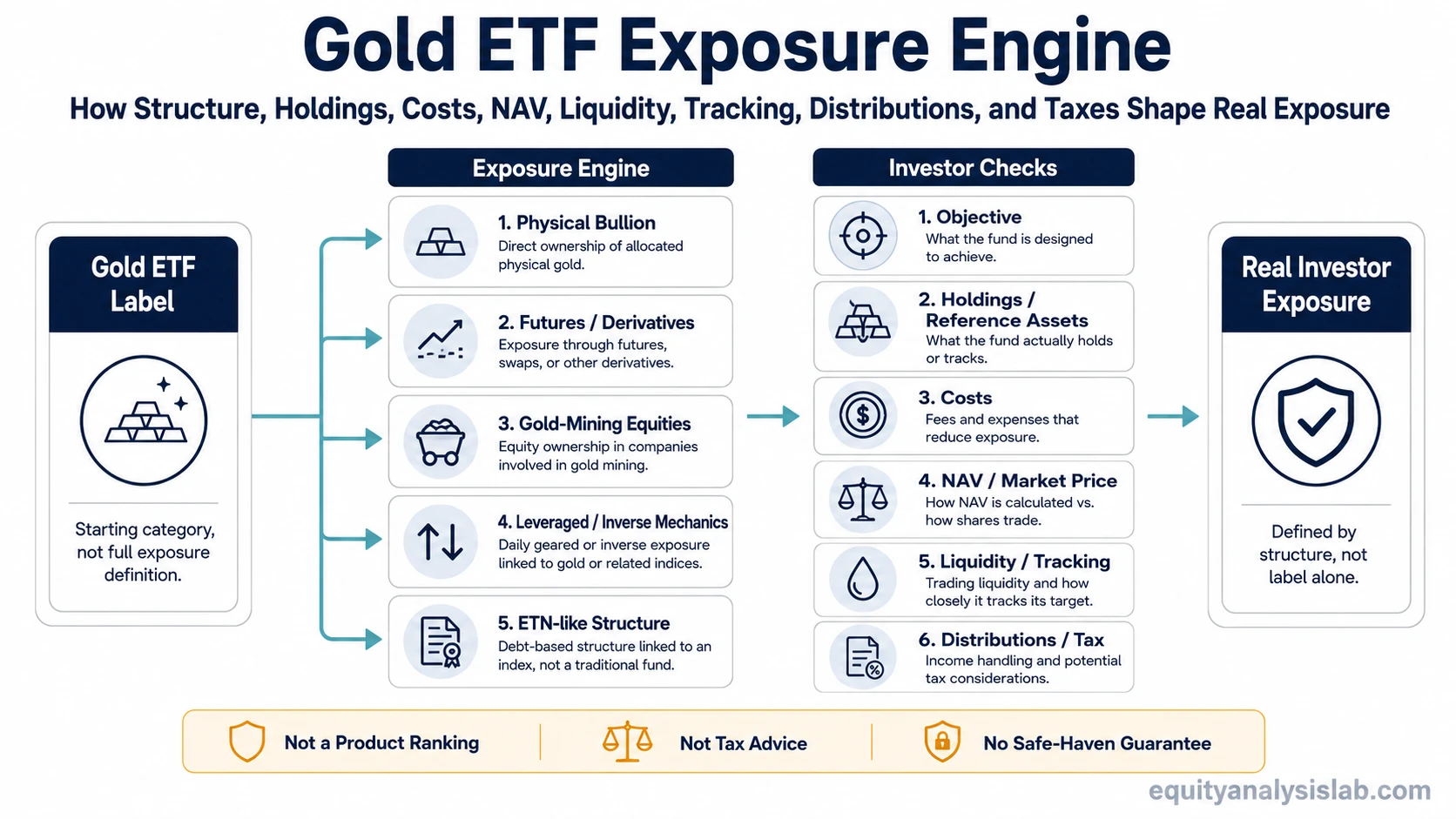

A gold ETF is an exchange-traded fund or exchange-traded product that gives investors gold-related exposure through a tradable fund wrapper. The exposure may come from physical bullion, futures or derivatives, gold-mining companies, leveraged or inverse mechanics, or note-like structures, so the label alone does not tell an investor what the fund actually owns or tracks.

A gold ETF can make gold exposure easier to access through a brokerage account, but it is not always the same as owning physical gold directly. The investor still has to read the fund objective, holdings, structure, costs, NAV behavior, trading liquidity, tracking pattern, distribution policy, and tax treatment before comparing products.

Key Points About Gold ETFs

- A gold ETF is a fund wrapper for gold-related exposure, not a guarantee of direct bullion ownership.

- Some products hold physical gold or gold-backed assets, while others use futures, derivatives, mining stocks, leverage, inverse exposure, or note-like structures.

- Expense ratios, bid-ask spreads, NAV premiums or discounts, tracking behavior, and tax treatment can make fund returns differ from the gold price.

- A gold ETF should be read through its objective, holdings, strategy, structure, liquidity, and investor-facing documents before any product comparison.

What Is a Gold ETF?

Gold ETF definition: A gold ETF is a listed fund or exchange-traded product designed to provide gold-related exposure through shares that trade on an exchange. The fund may reference physical bullion, gold futures, gold-related securities, or another gold-linked structure depending on its mandate.

The important distinction is between the gold label and the exposure engine. One fund may be designed around bullion backing, another may own shares of mining companies, and another may use derivatives to pursue a gold-linked objective. Those structures can behave differently even when they all appear under the broad gold ETF category.

This makes a gold ETF a more specific member of the broader commodity exposure universe. The category points toward gold, but the fund documents explain whether the investor is getting metal-linked exposure, company equity exposure, or a more complex instrument.

How Gold ETF Exposure Works

Gold ETF exposure usually starts with a fund objective. The objective tells the investor whether the product is trying to reflect the price of gold, hold gold-related assets, track an index, own companies in the gold industry, or pursue a leveraged or inverse result. The objective should be read before the fee, performance, or yield information because it defines what the fund is designed to do.

The next layer is the holdings or reference assets. A physically backed structure may reference bullion or gold-backed assets. A futures-based product may reference contracts and collateral. A mining equity ETF owns companies whose business results can be affected by gold prices, operating costs, reserves, management decisions, financing conditions, and equity-market sentiment.

That is why gold ETF analysis is not only a question of whether the investor wants gold exposure. It is also a question of how the fund converts that exposure into a tradable product. The wrapper, holdings, index, strategy, and trading structure define the real investment exposure more precisely than the label.

Physical Gold, Futures, Mining Stocks, and Other Structures

Gold ETFs and gold-linked exchange-traded products can use several structures. The table below is not a product ranking. It is a structure map for reading what a gold-labeled fund may actually reference.

| Structure | What it usually references | What to check | Main limitation |

|---|---|---|---|

| Physical gold or trust-style exposure | Bullion or gold-backed assets | Custody or backing language, NAV, expenses, creation and redemption structure | Not identical to holding coins or bars directly |

| Futures or derivatives | Contracts, swaps, collateral, or other derivative exposure | Roll mechanics, strategy rules, collateral treatment, costs, and tracking behavior | Can diverge from spot gold because of contract structure and costs |

| Gold-mining equity ETF | Shares of gold-related companies | Company holdings, sector concentration, geography, balance-sheet risk, and operating leverage | Can behave like equity exposure, not pure gold exposure |

| Leveraged or inverse product | Daily leveraged or inverse exposure to a gold-linked benchmark | Daily reset mechanics, objective, compounding effects, holding-period risk, and fees | Not plain gold exposure and not designed like a standard long-only fund |

| ETN-like product | An issuer note or promise linked to a gold-related index or return formula | Issuer credit risk, fees, maturity terms, tracking, and redemption rules | Structure risk differs from fund ownership of underlying assets |

A physically backed gold product and a gold-mining equity fund can both appear in a gold ETF search, but their risk drivers are different. The first is usually closer to metal-price exposure after expenses and trading effects. The second depends on company fundamentals as well as the gold price.

Costs, NAV, Liquidity, Tracking, and Distributions

A gold ETF’s expense ratio or management fee reduces the investor’s return relative to the underlying exposure. Even if a physically backed product closely reflects gold before costs, the fee creates a drag over time. Futures-based or derivative structures may add other costs through roll mechanics, collateral treatment, financing terms, or strategy implementation.

NAV and market price also matter. The net asset value represents the estimated value of the fund’s underlying assets or reference exposure. The market price is the price at which shares trade on an exchange. In normal conditions, ETF creation and redemption mechanics can help keep market price close to NAV, but premiums, discounts, spreads, and trading conditions still matter.

Liquidity should be read through more than one signal. Trading volume, bid-ask spread, fund size, underlying market liquidity, and creation/redemption activity can all affect the investor’s execution experience. A fund with narrow spreads and deep secondary-market trading may be easier to transact than a thinly traded or structurally complex product.

Tracking behavior is the practical result of all these mechanics. A gold ETF can differ from spot gold because of expenses, spreads, premiums or discounts, futures roll effects, derivative rules, mining-equity exposure, leverage, inverse mechanics, or note structure. Tracking difference is not automatically a flaw, but it has to be interpreted against the fund’s actual objective.

Distribution policy is another item to check, not an assumption. Some gold-related products may not produce income in the same way as an income-oriented bond ETF exposure might. Others may have distributions linked to securities holdings, collateral income, or structure-specific mechanics. The fund documents should define the distribution policy rather than the category label.

Distributions and Tax Treatment

Gold ETF tax treatment can depend on the product structure, domicile, investor location, account type, holding period, and local rules. A physically backed gold product, a futures-based product, a mining equity ETF, and an ETN-like product may not be treated the same way for tax purposes.

Tax treatment depends on the product structure, investor location, account type, holding period, and local rules. For exposure review, the important point is that tax mechanics should be checked before comparing gold ETF products. The prospectus, tax section, account context, and applicable local rules matter more than the broad gold ETF label.

When a Gold ETF May Not Match the Label

Key limitation: A gold ETF label is not enough to define the exposure. One product may hold physical bullion, another may own mining companies, another may use futures, and another may use leveraged or note-like mechanics. Costs, liquidity, tracking, distributions, and tax treatment can make the investor experience differ from the gold price itself.

The most common mistake is treating every gold ETF as a direct claim on gold. A bullion-backed product may be designed to reflect gold more closely, but a mining equity ETF introduces company-level risks. A futures-based product introduces contract and roll mechanics. A leveraged or inverse product introduces daily objective and compounding issues.

Another mistake is treating gold ETF exposure as automatically lower-risk because gold is often discussed in portfolio-defense contexts. The fund wrapper does not remove price volatility, tracking differences, structure risk, liquidity risk, or tax complexity. The exposure can still move against the investor, and different structures can respond differently under market stress.

A third mistake is comparing only past returns without reading the exposure route. A gold-mining equity fund may outperform or underperform bullion-linked exposure for reasons that have little to do with the spot gold price alone. Company margins, energy costs, financing conditions, jurisdiction risk, and equity-market sentiment can all affect mining stocks.

How to Read a Gold ETF Before Comparing Products

A gold ETF can be reviewed through a simple structure-first checklist. The goal is not to choose a product from the label, but to understand what the product actually gives the investor.

- Objective: What is the fund designed to track, hold, or deliver?

- Exposure engine: Does it use physical bullion, futures, derivatives, mining equities, leverage, inverse exposure, or a note-like structure?

- Holdings or reference assets: What does the portfolio own or reference?

- Index or strategy: Is the fund passive, rules-based, actively managed, or strategy-driven?

- Costs: What expense ratio, management fee, spread, financing cost, or roll cost may affect returns?

- NAV and market price: Does the product usually trade close to NAV, and what can create premiums or discounts?

- Liquidity: What do trading volume, bid-ask spread, AUM, flows, and underlying market depth suggest?

- Tracking: How closely has the product followed its stated objective, and why might it diverge?

- Distributions: Does the product distribute income or gains, and what drives that policy?

- Tax structure: What does the prospectus or tax section say, and what investor-specific rules may apply?

This checklist also helps separate passive exposure from a more flexible strategy. If the product gives a manager discretion over exposure, contracts, or positioning, the investor may need to read it closer to an actively managed ETF than a plain rules-based gold tracker.

A Practical Gold ETF Scenario

Consider two gold-labeled funds. One is designed to reflect gold through bullion-backed exposure after expenses. The other owns a basket of gold-mining companies. If the gold price rises, both may benefit, but not for the same reasons and not necessarily by the same amount. The mining fund may also react to labor costs, energy prices, balance-sheet leverage, reserve quality, management decisions, and equity-market sentiment.

That difference matters when the funds diverge. A bullion-backed product may track gold after expenses, while a mining equity fund can be pulled by company margins or equity-market conditions. The label points to the theme, but the exposure engine explains why the results can separate.

Gold ETF vs Owning Gold Directly

A gold ETF can be easier to buy and sell through a brokerage account than physical coins or bars, but the tradeoff is that the investor owns a fund share or exchange-traded product interest rather than personally storing the metal. The fund structure introduces expenses, trading spreads, potential NAV differences, custody arrangements, documentation, and tax treatment.

Physical ownership has its own issues, including storage, insurance, dealer spreads, authentication, and transaction logistics. A gold ETF does not remove every friction. It changes the type of friction from physical handling to fund structure, trading, tracking, and legal or tax mechanics.

| Comparison point | Gold ETF | Physical gold |

|---|---|---|

| Access | Trades through an exchange or brokerage platform | Requires physical purchase, storage, and sale process |

| Ownership form | Fund share, trust interest, note, or other exchange-traded wrapper | Coins, bars, or allocated physical metal depending on arrangement |

| Costs | Expense ratio, spreads, and possible structure-specific costs | Dealer spreads, storage, insurance, shipping, and authentication costs |

| Tracking | Depends on objective, structure, fees, NAV behavior, and market price | Direct metal exposure, but transaction prices can differ from quoted spot prices |

| Tax and documentation | Depends on fund structure, account type, investor location, and local rules | Depends on local rules, holding period, documentation, and sale treatment |

FAQ

What is a gold ETF?

A gold ETF is an exchange-traded fund or exchange-traded product that gives investors gold-related exposure through a fund wrapper. The exposure may come from physical bullion, futures, derivatives, mining-company shares, leverage, inverse mechanics, or note-like structures depending on the product.

Does a gold ETF own physical gold?

Some gold ETFs or trust-style products hold physical bullion or gold-backed assets, but not all gold ETFs do. Some use futures, derivatives, mining stocks, leveraged or inverse exposure, or note-like structures. The holdings and fund objective define the actual exposure.

Is a gold ETF the same as owning gold?

No. A gold ETF can provide gold-related exposure, but it is not always the same as owning physical coins or bars directly. The fund wrapper may introduce expense ratios, trading spreads, NAV premiums or discounts, tracking differences, custody arrangements, and tax rules.

What can make a gold ETF behave differently from gold?

A gold ETF can behave differently from gold because of expenses, futures roll mechanics, derivative exposure, mining-company holdings, leverage, inverse objectives, note structure, bid-ask spreads, premiums or discounts to NAV, distributions, and tax treatment.