A bond ETF is an exchange-traded fund that holds fixed-income exposure inside an ETF wrapper. The portfolio may own government bonds, corporate bonds, municipal bonds, international bonds, or other debt instruments, while the ETF shares trade on an exchange during the trading day.

Definition: A bond ETF gives investors exposure to a basket of bonds through shares of an exchange-traded fund. The bond exposure shapes income, duration, credit risk, and tracking behavior, while the ETF wrapper affects trading, liquidity, market price, and potential premium or discount to net asset value.

The label is only the starting category. Two bond ETFs can behave very differently if one holds short-term government bonds and another holds longer-maturity or lower-credit-quality bonds. Real evaluation depends on what the fund owns, how the portfolio is built, how the ETF trades, what it costs, how it distributes income, and how the investor’s account context affects the after-tax result.

Bond ETF key points

- A bond ETF combines fixed-income exposure with exchange-traded ETF shares.

- Holdings, duration, maturity, and credit quality drive much of the fund’s behavior.

- The ETF market price can move away from the fund’s net asset value, creating a premium or discount.

- Distributions may reflect income from the underlying bonds, but the amount and tax treatment can vary.

- Expense ratio, bid-ask spread, tracking difference, liquidity, and tax context all affect investor experience.

- A bond ETF can still lose value and does not remove interest-rate risk, credit risk, liquidity risk, or tracking risk.

How bond ETFs work

A bond ETF starts with a fixed-income portfolio. The fund may track a bond index, sample part of a larger bond universe, or use manager discretion if it is structured as an actively managed ETF. Investors do not usually buy each underlying bond directly through the ETF. They buy ETF shares that represent exposure to the fund’s portfolio.

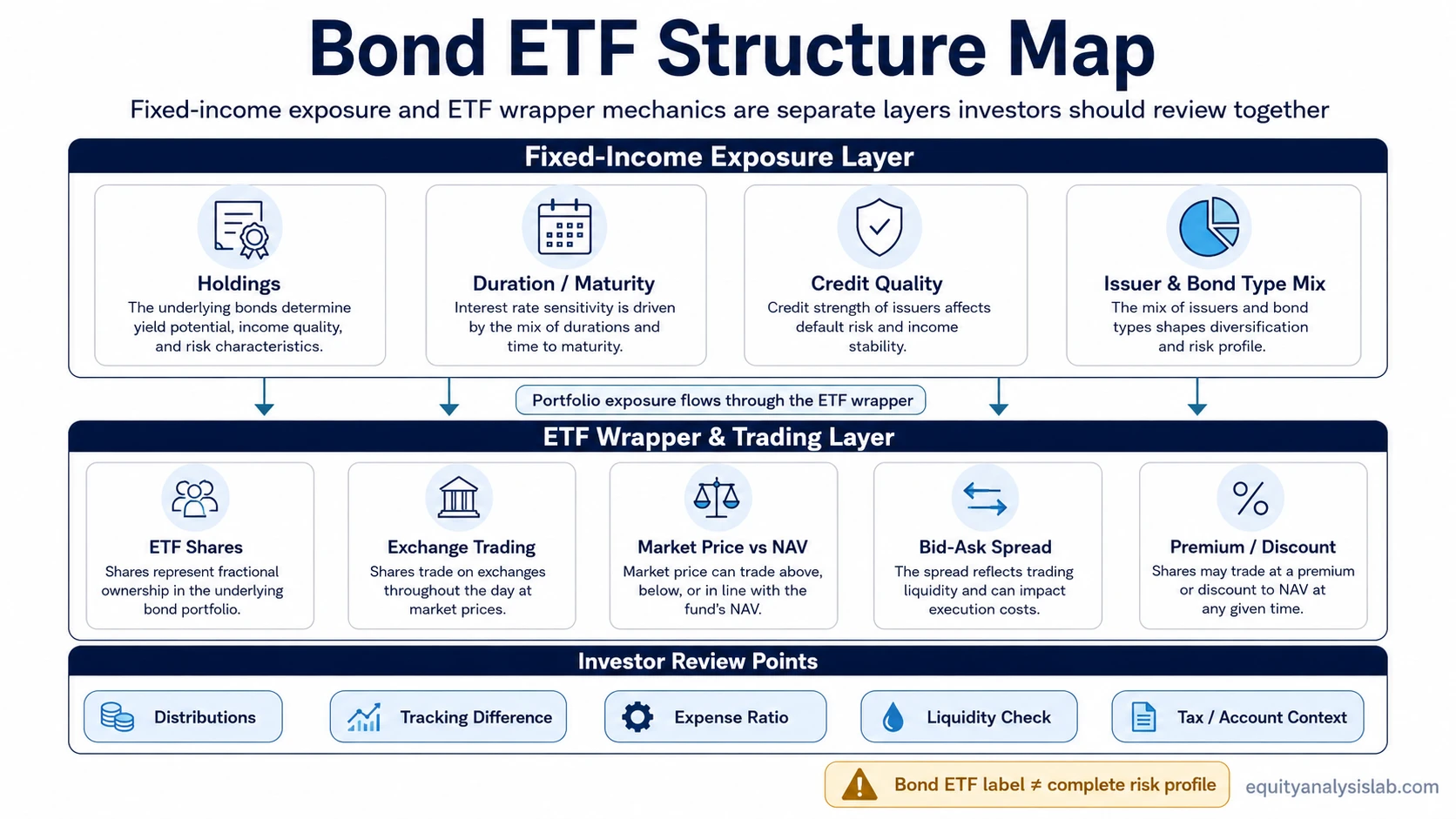

The ETF wrapper creates two layers to inspect. The first layer is the bond exposure: issuer type, maturity, duration, coupon profile, credit quality, geography, currency, and index or strategy design. The second layer is the trading wrapper: exchange trading, bid-ask spread, market price, net asset value, creation/redemption mechanics, and potential premium or discount.

Mechanism route: underlying bonds → fund portfolio or strategy → ETF shares → exchange trading price → distributions, tracking behavior, and investor account outcome.

Net asset value is the fund’s calculated value based on its holdings. The ETF market price is the price at which shares trade on the exchange. Those two values are usually connected, but they are not identical. During stressed or less liquid conditions, a bond ETF can trade at a premium or discount to net asset value, especially when underlying bonds are harder to price or trade.

What bond ETF exposure actually depends on

Bond ETF behavior depends less on the category label and more on the portfolio’s fixed-income characteristics. A short-duration Treasury bond ETF and a long-duration corporate bond ETF are both bond ETFs, but they can respond differently to interest-rate changes, credit-spread changes, liquidity conditions, and investor demand.

| Exposure variable | What it shows | Why it matters |

|---|---|---|

| Holdings | The issuers and bond types inside the fund | Shows whether exposure comes from government, corporate, municipal, international, securitized, or mixed fixed-income markets. |

| Duration and maturity | The fund’s sensitivity to interest-rate changes and bond repayment timing | Longer duration usually increases sensitivity to rate moves, while shorter duration may reduce that sensitivity but can change income profile. |

| Credit quality | The portfolio’s issuer-risk profile | Lower credit quality can increase sensitivity to default risk, downgrade risk, and credit-spread changes. |

| Index or strategy | How the portfolio is selected and maintained | Some bond ETFs track an index closely, while others may sample the index or use active judgment. |

| Currency and geography | Whether the fund includes domestic, international, or currency-exposed bonds | Currency and market structure can affect return, volatility, taxation, and interpretation. |

Index sampling is common in fixed income because some bond markets contain many individual securities and not every bond trades with the same frequency. Sampling can help a fund approximate an index, but it also means the ETF may not hold every bond in the benchmark. That can contribute to tracking difference between the ETF and the index it is trying to represent.

What to inspect before comparing bond ETFs

A bond ETF comparison should begin with the mechanics that can be observed in the fund’s documents, portfolio data, and trading behavior. A lower expense ratio is useful information, but it is not enough by itself. Cost, exposure, liquidity, distributions, tracking, and account context work together.

| Observable | What it shows | Why it matters |

|---|---|---|

| Expense ratio | The fund’s stated annual operating cost | Cost can reduce investor return over time, especially when expected bond returns are modest. |

| Distribution policy | How the fund pays income or other distributions | Distributions can vary by holdings, rate environment, fund policy, and tax classification. |

| Yield figures | Different ways of measuring income or expected income | Yield is not a guarantee and should be read with the calculation method and portfolio risk in mind. |

| Duration | Interest-rate sensitivity | Helps explain why some bond ETFs move more when rates change. |

| Credit quality | Issuer-risk and credit-spread exposure | Helps separate higher-quality bond exposure from funds taking more credit risk. |

| Bid-ask spread | The trading cost between buying and selling ETF shares | A wider spread can increase transaction cost, especially for less liquid ETFs or stressed markets. |

| Premium or discount | Difference between ETF market price and net asset value | Shows whether ETF shares are trading above or below the estimated value of the underlying portfolio. |

| Tracking difference | How closely the ETF follows its benchmark or stated objective | Can reflect expenses, sampling, trading costs, cash drag, or portfolio differences. |

| Underlying bond liquidity | How easily the bonds inside the ETF may trade | ETF share liquidity and underlying bond liquidity are related but not identical. |

| Tax and account context | How distributions and gains may be treated for the investor | Tax outcome can vary by fund structure, distribution type, investor jurisdiction, and account type. |

Practical scenario: Two funds can both be bond ETFs while carrying different risk profiles. One may hold shorter-maturity, higher-quality bonds, while another may hold longer-maturity or lower-credit-quality bonds. The shared label does not make the funds interchangeable.

Where the bond ETF label can mislead

A bond ETF is not automatically safe, stable, tax-free, or fully diversified. The ETF wrapper changes how the exposure is accessed, but it does not remove the economic risk of the bonds inside the fund.

Common mistake: Treating “bond ETF” as a complete risk description. The label tells you the fund is in the fixed-income ETF category. It does not tell you enough about duration, credit risk, liquidity, currency exposure, distribution stability, tracking behavior, or tax outcome.

Diversification can reduce dependence on a single issuer, but it does not eliminate interest-rate risk or broad credit-market risk. A fund that holds many bonds can still decline if rates rise, spreads widen, liquidity weakens, or the market reprices the type of bonds the ETF owns.

Income expectations also need caution. A bond ETF may distribute income, but distributions are not the same as guaranteed payments to the shareholder. Amounts can change, and the tax classification of distributions can depend on the fund, the underlying bonds, the investor’s account, and applicable tax rules.

Bond ETF risks and limitations

Bond ETF risk is a combination of fixed-income risk and ETF wrapper risk. The main question is not whether the fund is a bond ETF, but which risks the structure concentrates or reduces.

| Risk or limitation | How it can appear | What to check |

|---|---|---|

| Interest-rate risk | Bond prices can fall when yields rise, especially for longer-duration exposure. | Duration, maturity profile, yield curve exposure, and rate sensitivity. |

| Credit risk | Issuer deterioration, downgrades, or wider credit spreads can pressure lower-quality bond exposure. | Credit ratings, issuer mix, sector exposure, and spread sensitivity. |

| Liquidity risk | The ETF may trade actively while some underlying bonds trade less frequently or with wider spreads. | ETF bid-ask spread, trading volume, premium/discount history, and underlying bond market depth. |

| Tracking risk | The fund may not perfectly match its benchmark or stated exposure. | Tracking difference, sampling approach, expense ratio, cash holdings, and portfolio turnover. |

| Distribution uncertainty | Income payments can change as holdings, rates, and fund policy change. | Distribution history, yield methodology, holdings, and fund documents. |

| Tax uncertainty | Distributions and gains may receive different treatment depending on structure and account context. | Fund tax documents and qualified tax guidance for the investor’s jurisdiction and account type. |

| Currency risk | International bond exposure can add currency movement to bond-market movement. | Currency exposure, hedging policy, and geographic allocation. |

Limitation: A bond ETF can improve access and transparency relative to buying many individual bonds directly, but it does not guarantee stable value, stable income, tax efficiency, or easy trading in every market condition.

Bond ETF versus related ETF types

A bond ETF is defined by fixed-income exposure. Other ETF types can use the same exchange-traded wrapper while giving investors exposure to different assets, strategies, or income sources.

| Related ETF type | Main distinction | Why the distinction matters |

|---|---|---|

| Actively managed ETF | Describes manager discretion, not a specific asset class. | A bond ETF can be index-based or actively managed; the active label explains portfolio decision style, not fixed-income risk by itself. |

| Commodity ETF | Provides commodity-related exposure rather than bond exposure. | Commodity ETF behavior is usually tied to commodities, futures structures, or commodity-linked holdings, not duration and credit quality. |

| Dividend ETF | Focuses on equity income characteristics rather than bond income. | A dividend ETF and a bond ETF may both distribute cash, but the source, risk profile, tax treatment, and volatility drivers can differ. |

FAQ

How do bond ETFs pay income?

Bond ETFs may distribute income received from the bonds they hold, but the amount, timing, and tax classification can vary by fund, holdings, distribution policy, market conditions, investor account type, and applicable tax rules.

Can a bond ETF lose value?

Yes. A bond ETF can lose value if interest rates rise, credit spreads widen, issuers weaken, liquidity deteriorates, currency exposure moves against the fund, or the ETF trades at a discount to net asset value.

Is ETF liquidity the same as underlying bond liquidity?

No. ETF shares trade on an exchange, but the underlying bonds may have their own liquidity conditions. ETF trading liquidity, bid-ask spread, premium or discount, and the liquidity of the bonds inside the fund should be inspected separately.