A commodity ETF is an exchange-traded fund or exchange-traded product that gives investors exposure to commodities or commodity-linked instruments, such as physical metals, futures contracts, swaps, or commodity producer equities.

The commodity name in the fund label is only the starting point. The actual exposure depends on holdings, contracts, benchmark rules, costs, liquidity, distributions, tracking behavior, and tax structure.

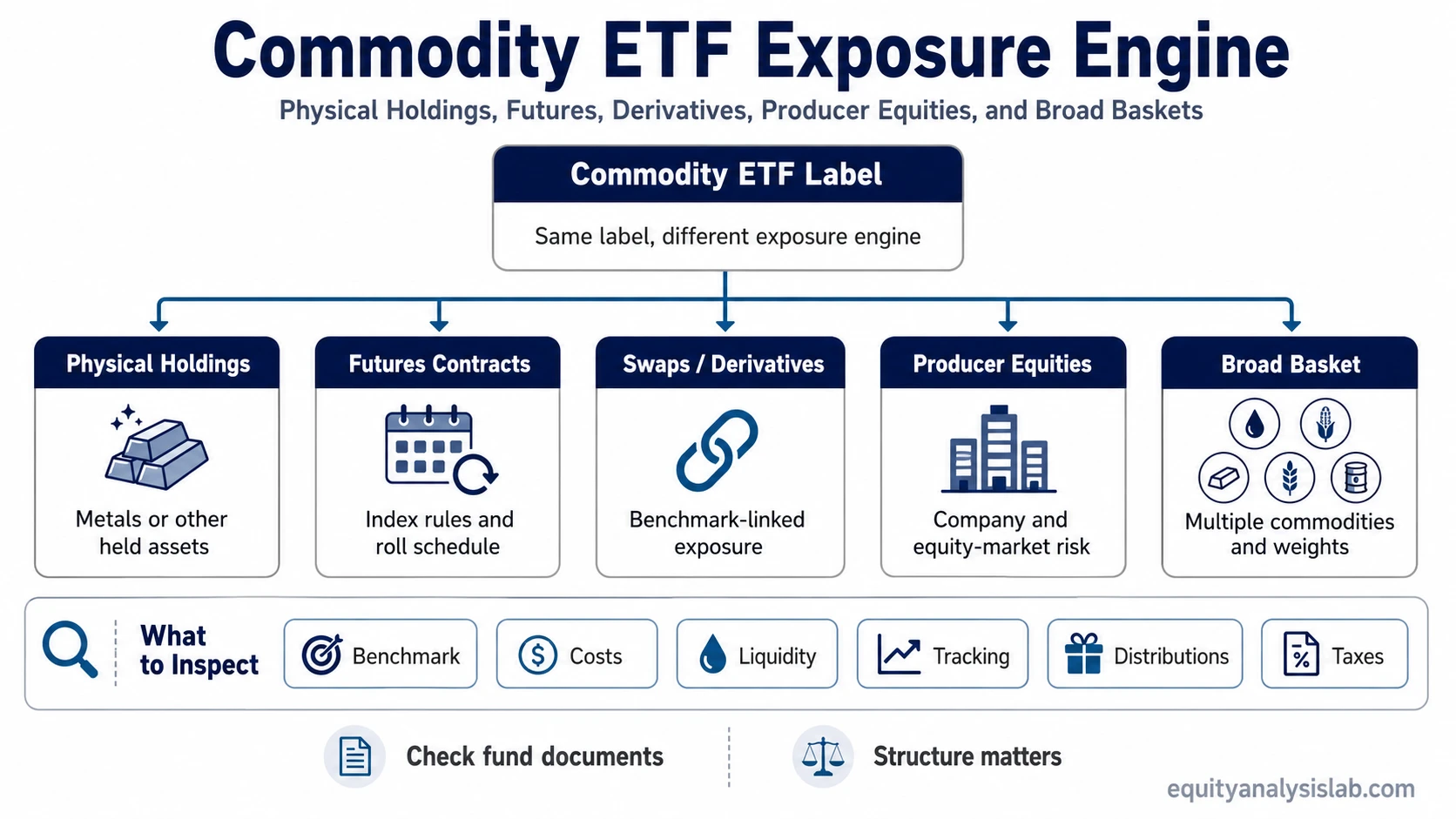

What Is a Commodity ETF?

A commodity ETF is a listed fund or exchange-traded product designed to track, hold, or reference a commodity exposure. That exposure may come from a physical asset, a futures index, a derivative contract, a basket of commodities, or shares of companies connected to commodity production.

The useful distinction is that “commodity ETF” describes the exposure category, not the exact engine underneath it. Two funds can both carry a commodity label while behaving differently because one holds metal, another rolls futures contracts, and another owns producer equities.

Key Points

- A commodity ETF can use physical holdings, futures, swaps, producer equities, or a mix of structures.

- The benchmark, weighting method, roll process, and rebalancing rules affect how exposure behaves.

- ETF returns may differ from spot commodity price moves because of roll costs, fees, collateral treatment, liquidity, and market price versus NAV.

- Expense ratio, bid-ask spread, trading volume, and premium or discount can affect the investor’s realized result.

- Distributions and tax reporting can vary by structure, so they should not be assumed from the commodity label alone.

How Commodity ETFs Create Exposure

Commodity ETFs do not all reach commodities through the same path. Some are closer to direct commodity exposure, while others are linked to contracts, indexes, derivatives, or companies whose business results depend partly on commodity markets.

| Exposure route | What it usually means | What to inspect |

|---|---|---|

| Physical commodity exposure | The product holds or is backed by a physical commodity, most commonly in precious-metal structures. | Custody, storage, trust structure, fees, share mechanics, and tax treatment. |

| Futures-based exposure | The fund tracks commodity futures contracts rather than the spot commodity price directly. | Contract maturity, roll schedule, index methodology, collateral treatment, and curve shape. |

| Swaps or derivatives | The fund uses derivative exposure to reference a commodity index or return stream. | Counterparty exposure, benchmark rules, collateral, and disclosure language. |

| Producer-equity exposure | The fund owns shares of companies tied to commodity production, mining, processing, or transportation. | Company fundamentals, margins, operating leverage, balance-sheet risk, and equity-market behavior. |

| Broad basket exposure | The fund references multiple commodities instead of one commodity. | Weighting method, sector concentration, rebalancing rules, and single-commodity influence. |

A commodity ETF can therefore behave more like a commodity wrapper, a futures-index product, a derivative-linked vehicle, or an equity-sector fund depending on what it actually holds or references.

Why Commodity ETFs May Not Track Spot Commodity Prices

A commodity ETF does not always move one-for-one with the spot commodity price. The reason is usually structural, not mysterious. The fund may own futures contracts with different expiration dates, pay fees, roll contracts over time, trade at a market price that differs from NAV, or hold equities that respond to business fundamentals as well as commodity prices.

The main distinction is whether the return driver is the spot commodity, a futures index, a derivative-linked benchmark, or the operating results of commodity-related companies.

A futures-based commodity ETF can move differently from the spot commodity because the fund may hold contracts with different maturities and must replace expiring contracts over time. If later-dated futures are more expensive than near-term contracts, the roll process can create a drag. If later-dated futures are cheaper, the roll process can help. Fees, index rules, collateral income, and bid-ask spreads can also affect the final investor experience.

Exposure Engine Checklist

A commodity ETF is easier to analyze when the label is separated from the exposure engine. The label says the category. The checklist shows which structural details should be inspected before two commodity ETF structures are treated as comparable.

| Question | Why it matters |

|---|---|

| What does the fund actually hold or reference? | The answer separates physical, futures, derivative, equity, and basket structures. |

| Is the benchmark based on spot prices, futures, or company equities? | The benchmark explains why the ETF may not match a headline commodity price. |

| How are contracts rolled or holdings rebalanced? | Roll rules and rebalancing can change tracking behavior over time. |

| What are the expense ratio and trading costs? | Expense ratio, bid-ask spread, and trading liquidity all affect the final result. |

| Does the market price stay close to NAV? | Premiums and discounts can appear when trading conditions, liquidity, or underlying markets are stressed. |

| How are distributions and taxes handled? | Income, reporting, and tax treatment depend on structure and should be checked in fund documents. |

Commodity ETF Risks and Limitations

A commodity ETF does not remove commodity risk. It changes how the exposure is packaged. The main limitations usually come from structure, not only from the commodity itself.

- Tracking difference: ETF returns can differ from the spot commodity because of fees, roll mechanics, index rules, collateral, spreads, and market price versus NAV.

- Liquidity risk: Thin trading, wider bid-ask spreads, or stressed underlying markets can make entry and exit prices less efficient.

- Concentration risk: Single-commodity products can be highly exposed to one market, while broad baskets can still be dominated by a few heavily weighted commodities.

- Equity risk: Producer-equity exposure can be affected by management, leverage, costs, regulation, earnings, and stock-market conditions.

- Tax and reporting complexity: Legal structure and holdings can change reporting requirements and after-tax results.

Do Commodity ETFs Pay Dividends?

Some commodity ETFs may make distributions, but dividends should not be assumed. A physically backed commodity product may not generate operating income in the same way a stock fund does. A futures-based structure may have collateral or other distribution mechanics. A producer-equity fund may receive dividends from underlying companies if those companies pay them.

This is why a commodity ETF should be separated from an income-focused ETF structure. The commodity label describes exposure, while distribution behavior depends on holdings, fund structure, and policy.

Commodity ETF Tax Treatment Can Vary

Commodity ETF tax treatment can vary by legal structure, holdings, account type, and reporting format. A futures-based product, a physically backed commodity product, a trust-style structure, a partnership-style structure, and an equity ETF holding commodity producers may not create the same reporting profile.

This is why a commodity ETF should not be treated as tax-simple from the fund label alone. Fund documents should be checked for structure-specific reporting details, and qualified tax guidance may be needed when questions involve K-1 forms, Form 1099 reporting, collectibles treatment, or other tax categories.

Commodity ETF vs Related ETF Structures

A commodity ETF differs from an actively managed ETF because the main question is usually the exposure engine, not whether a manager is making discretionary portfolio choices.

It also differs from bond ETFs, where the exposure is tied to fixed-income instruments, interest-rate sensitivity, credit quality, maturity, and yield mechanics rather than commodity-linked assets.

The comparison matters because similar ETF wrappers can hide very different sources of risk. Commodity ETFs should be read through holdings, benchmark rules, structure, liquidity, costs, distributions, and tax treatment instead of the category label alone.

FAQ

What does a commodity ETF invest in?

A commodity ETF may invest in physical commodities, futures contracts, swaps, commodity indexes, or producer equities. The exact structure depends on the fund documents, not just the commodity label.

Why can a commodity ETF perform differently from the commodity price?

Performance can differ because of fees, futures roll mechanics, benchmark rules, collateral treatment, bid-ask spreads, premiums or discounts to NAV, and whether the fund owns physical commodities, contracts, or producer stocks.

Are commodity ETFs the same as commodity stocks?

No. A commodity ETF may hold direct or derivative commodity exposure, while commodity stocks are shares of companies connected to production, mining, processing, or transportation. Producer-equity funds can add company-specific risk that is separate from the commodity price itself.

Do commodity ETFs have the same tax treatment?

No. Tax treatment can vary by legal structure, holdings, account type, and reporting format. Fund documents and qualified tax guidance are needed for structure-specific answers.