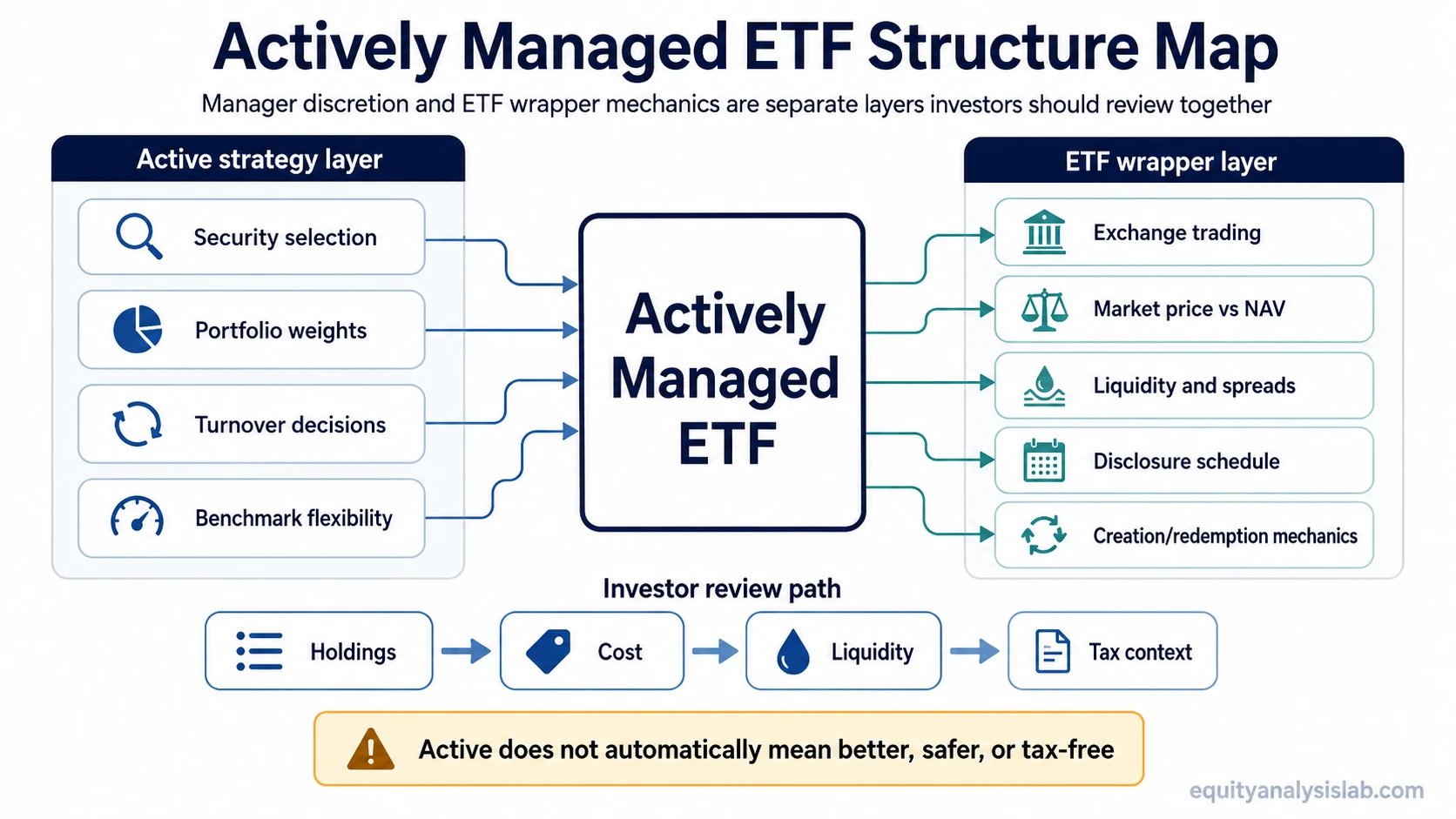

An actively managed ETF is not simply a passive index fund. The active part describes how a manager selects, removes, weights, or adjusts holdings. The ETF part describes the wrapper: exchange trading, market price versus net asset value, liquidity, transparency, creation and redemption mechanics, and the way fund-level tax events may be handled.

Definition: An actively managed ETF is an exchange-traded fund whose portfolio is managed with discretion under a stated investment strategy, rather than being built only to track an index mechanically.

For investors, the useful distinction is practical: active management explains who decides what the fund owns, while the ETF wrapper explains how investors buy and sell shares, how the fund trades, how holdings may be disclosed, and how costs and taxable distributions can appear.

Key Points About Actively Managed ETFs

- An actively managed ETF uses manager discretion instead of purely following an index.

- The ETF wrapper still matters because the fund trades on an exchange at a market price that can differ from net asset value.

- Active management does not guarantee better returns, lower risk, or lower taxes.

- Investors should compare holdings, strategy, cost, liquidity, spread, disclosure, turnover, and distribution history before treating two active ETFs as similar.

What Is an Actively Managed ETF?

An actively managed ETF combines an active portfolio strategy with an ETF trading structure. The manager may choose securities, adjust sector weights, change duration, hold more cash, rotate exposures, or manage risk according to the fund’s objective.

That does not mean the fund has no benchmark. Some active ETFs use a benchmark for comparison, risk control, or performance reporting. The difference is that the manager is not usually trying to replicate the benchmark security by security in the same way a passive ETF normally would.

The active ETF label also does not tell the investor what the fund owns. One active ETF may hold a concentrated equity portfolio. Another may manage fixed income exposure, options income, commodities-related exposure, or a dividend-oriented portfolio. The label describes the management style, not the exposure category by itself.

How Active Management Fits Inside the ETF Wrapper

The strategy layer determines how the portfolio is built. The wrapper determines how fund shares trade and how the fund interacts with the market. Keeping those layers separate prevents the common mistake of treating every ETF as passive or every active ETF as directly comparable.

| Layer | What it controls | What investors should check |

|---|---|---|

| Active strategy | Security selection, portfolio weights, turnover, risk positioning, and benchmark relationship. | Holdings, concentration, stated objective, portfolio changes, and whether the strategy is truly different from a cheaper passive alternative. |

| ETF wrapper | Exchange trading, market price, creation/redemption process, disclosure format, and secondary-market liquidity. | Bid-ask spread, trading volume, premium or discount to NAV, holdings disclosure, and tax-distribution behavior. |

Some active ETFs disclose full holdings frequently, while others may use a semi-transparent structure or a tracking basket. In that case, investors may not see the exact portfolio in the same way they would with a fully transparent ETF. The disclosure schedule should be part of the comparison.

Actively Managed ETF vs Passive ETF

A passive ETF usually tries to track an index. An actively managed ETF gives the manager more discretion to differ from an index or to operate without copying one. That difference affects cost, tracking behavior, portfolio turnover, and the way investors evaluate results.

| Comparison point | Actively managed ETF | Passive ETF |

|---|---|---|

| Portfolio construction | Manager selects and adjusts holdings under a stated strategy. | Portfolio is usually built to track an index. |

| Benchmark relationship | May use a benchmark for comparison but can differ meaningfully from it. | Usually seeks to follow the benchmark closely before fees and tracking effects. |

| Cost profile | Often has a higher expense ratio because research and management are part of the product. | Often has a lower expense ratio, especially for broad market index exposure. |

| Outcome evaluation | Investors judge whether the manager’s choices justify the cost and risk taken. | Investors judge tracking quality, cost, liquidity, and index fit. |

| Main misconception | Active does not automatically mean better. | Passive does not automatically mean risk-free. |

The important question is not whether active or passive is universally better. The practical question is whether the fund’s strategy, costs, portfolio, liquidity, and risk profile fit the investor’s purpose better than the available alternatives.

Actively Managed ETF vs Active Mutual Fund

An actively managed ETF and an active mutual fund can both use manager discretion. The difference is the wrapper. ETF shares trade intraday on an exchange, while traditional mutual fund shares are usually bought or redeemed at end-of-day NAV.

| Feature | Actively managed ETF | Active mutual fund |

|---|---|---|

| Trading | Trades intraday at a market price. | Usually transacts at end-of-day NAV. |

| Market price vs NAV | Can trade at a premium or discount to NAV. | Normally priced directly at NAV for purchases and redemptions. |

| Transparency | Depends on the ETF structure and disclosure schedule. | Usually reports holdings on a less frequent schedule. |

| Tax mechanics | ETF creation/redemption mechanics may reduce some fund-level capital gains distribution pressure. | Shareholder redemptions and portfolio activity may create different distribution dynamics. |

| Trading cost | Investor may face bid-ask spread and brokerage execution effects. | Investor may face fund fees, possible loads, or redemption policies depending on the fund. |

The ETF wrapper can be more tax-efficient in some situations, but it does not make the fund tax-free. Investors can still owe taxes on dividends, capital gains distributions, or gains from selling ETF shares in a taxable account.

What Investors Should Check Before Comparing Active ETFs

Two active ETFs with similar names can behave very differently. The comparison should start with the portfolio and strategy, then move to wrapper mechanics, costs, and account context.

| Check | Why it matters | Question to ask |

|---|---|---|

| Holdings | The fund label may hide major differences in securities, sectors, duration, geography, or factor exposure. | What does the fund actually own? |

| Concentration | A concentrated active ETF can behave very differently from a diversified one. | How much of the portfolio is driven by the largest holdings? |

| Strategy and benchmark relationship | Some active funds stay close to a benchmark, while others make larger active bets. | Is the manager meaningfully different from the benchmark? |

| Expense ratio | A higher fee raises the hurdle the strategy needs to clear for investors. | What is the all-in fund cost relative to passive alternatives? |

| Bid-ask spread and liquidity | Trading costs can matter even when the stated expense ratio looks reasonable. | Can the ETF be traded efficiently at the size the investor needs? |

| Premium or discount to NAV | The market price can move away from the value of the underlying portfolio. | Does the ETF usually trade close to NAV? |

| Disclosure schedule | Not every active ETF shows holdings in the same way. | Can the investor see enough to understand the portfolio? |

| Turnover | Frequent portfolio changes can affect cost, tax behavior, and strategy consistency. | How much does the manager trade inside the fund? |

| Tax account context | The same fund can matter differently in taxable and tax-advantaged accounts. | Where will the ETF be held? |

How Actively Managed ETFs Can Differ From Each Other

The active ETF category is broad. A high-turnover active equity ETF, a bond ETF managed around duration and credit risk, and an options-income ETF can all be active while having very different risk drivers.

That is why the label should be treated as a starting point, not a conclusion. Investors still need to identify the exposure, portfolio process, cost structure, manager discretion, and wrapper mechanics. A fund can be active and still behave much like a benchmark, or it can be active and take concentrated positions that create a very different return path.

Limits and Misconceptions

Active does not mean better. A manager can make useful decisions, but the same discretion can also lead to underperformance, higher turnover, or strategy drift.

ETF does not mean passive. Many ETFs track indexes, but the ETF structure can also hold an actively managed portfolio.

ETF tax efficiency does not mean no taxes. The ETF structure may reduce some fund-level capital gains distribution pressure, but investors can still face taxable dividends, distributions, and gains from selling shares.

Lower expense ratio is not the only cost. Bid-ask spreads, premium/discount behavior, trading size, and portfolio turnover can all affect the investor’s actual experience.

Transparency is not identical across all active ETFs. Some active ETFs disclose holdings more openly than others. Semi-transparent structures can make the holdings review less direct.

Example: Two Active ETFs With the Same Broad Label

Suppose two active equity ETFs both describe themselves as growth-oriented. The first owns a concentrated portfolio of large companies, changes holdings slowly, trades with tight spreads, and publishes holdings frequently. The second owns a wider mix of companies, rotates more often, trades with a wider spread, and discloses a proxy basket rather than the full portfolio each day.

The shared active ETF label is not enough to compare them. An investor would still need to inspect holdings, concentration, turnover, cost, liquidity, transparency, and distributions. If the goal is income rather than growth exposure, the comparison may also need to separate the active strategy from a dividend ETF objective, because distribution focus and active portfolio discretion are different concepts.

How Active ETFs Fit Beside Other ETF Types

“Actively managed” describes how the portfolio is managed. It does not replace the need to identify what the ETF is exposed to. An active ETF can be equity-focused, fixed-income-focused, options-based, commodity-linked, dividend-oriented, or built around another defined mandate.

This is why exposure and management style should be separated. A commodity ETF structure raises different questions about underlying exposure, futures, holdings, and roll behavior than an active equity ETF. The active/passive question is only one part of the ETF review.

FAQ

Are all ETFs passive?

No. Many ETFs are passive index-tracking funds, but an ETF can also be actively managed. The ETF wrapper describes how the fund is structured and traded; it does not automatically determine whether the portfolio is passive or active.

Is an actively managed ETF the same as an active mutual fund?

No. Both can use manager discretion, but the wrapper is different. An actively managed ETF trades on an exchange during the day, while a traditional mutual fund usually transacts at end-of-day NAV.

Do actively managed ETFs outperform passive ETFs?

Not necessarily. Active management creates the possibility of differing from a benchmark, but it does not guarantee better returns. Costs, holdings, risk, turnover, liquidity, and the manager’s decisions all matter.

Are actively managed ETFs tax-free?

No. ETF mechanics can reduce some fund-level capital gains distribution pressure in certain situations, but investors can still owe taxes on dividends, capital gains distributions, or gains from selling ETF shares in taxable accounts.