Sector analysis is the starting layer for deciding which business-model questions matter before evaluating a company inside a specific sector. A bank, a SaaS company, a semiconductor business, a retailer, and a utility can all report revenue, margins, and cash flow, but the evidence behind those numbers is not the same.

A useful sector analysis framework does not rank sectors or replace company analysis. It helps investors choose the right lens before moving into deeper work: credit quality for banks, recurring-revenue durability for software, capacity cycles for semiconductors, demand sensitivity for cyclical businesses, and cash-flow stability for more defensive sectors.

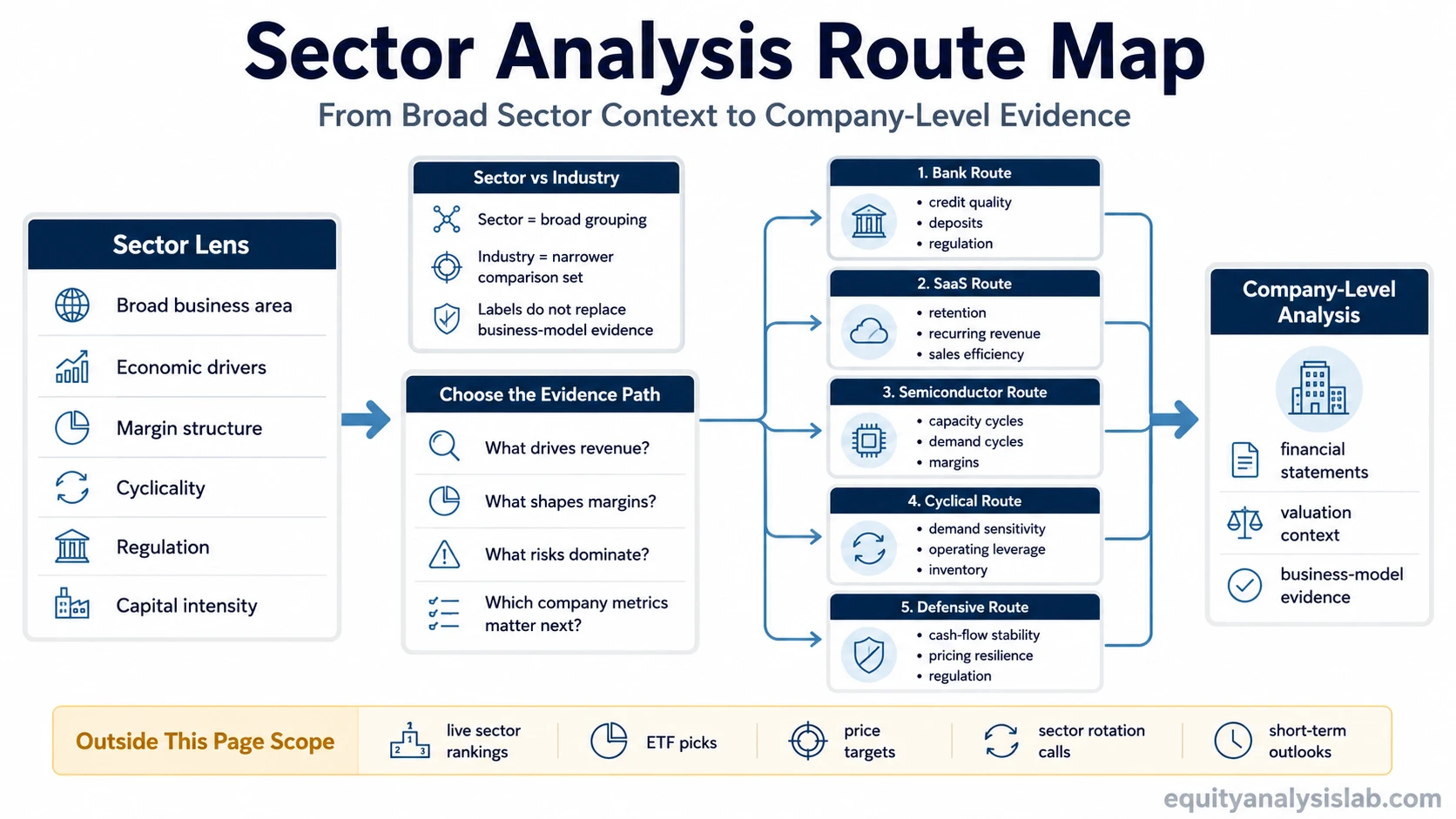

Sector Analysis Routes Company Research

Sector analysis means studying the economic, operating, and financial traits that shape companies within the same broad business area. In stock market research, it helps organize the questions an investor should ask before comparing individual companies.

The main value is separation. Some sectors are driven by credit cycles and regulation. Others depend on subscriptions, production capacity, commodity prices, inventory turns, or capital spending cycles. Treating those businesses with one generic checklist can hide the factors that actually move revenue quality, margins, reinvestment needs, and cash conversion.

Sector vs Industry in Company Analysis

A sector is a broad grouping, such as financials, technology, healthcare, industrials, or consumer staples. An industry is usually narrower and describes a more specific business group inside that sector.

The distinction matters because sector analysis sets the first research lens, while industry analysis can refine the comparison set. For example, a broad technology sector label does not explain the same evidence for a SaaS company, a semiconductor manufacturer, and a hardware distributor. Each business can sit near the same sector universe while requiring different revenue, margin, capital-intensity, and risk checks.

Official sector classifications can help identify labels, but they do not replace business-model evidence. Investors still need to understand how the company earns revenue, how costs behave, what risks dominate the sector, and which company-level metrics deserve the most attention.

What Belongs Inside Sector Analysis

Inside scope: sector-specific business drivers, revenue models, margin structure, cyclicality, regulation, capital intensity, working-capital behavior, and the type of company-level evidence needed after the sector lens is chosen.

Outside scope: live sector rankings, ETF recommendations, price targets, short-term sector rotation signals, stock screener output, and current market-outlook calls.

The boundary matters because sector context can improve the quality of company analysis, but it does not prove that a sector is attractive or that a stock is safe. A sector label is only the first filter. The deeper conclusion still depends on company-specific evidence.

Choose the Right Sector Analysis Path

| Sector-analysis route | Use this path when the main question is about | Evidence to examine next |

|---|---|---|

| bank stock analysis | Deposits, credit quality, interest income, regulation, loan losses, and balance-sheet risk. | Net interest margin, deposit mix, loan book quality, capital ratios, provisions, and sensitivity to rate changes. |

| SaaS company analysis | Recurring revenue, retention, customer acquisition efficiency, expansion revenue, and software gross margins. | ARR or MRR movement, net revenue retention, churn, CAC payback, gross margin, operating leverage, and cash burn. |

| Semiconductor businesses | Chip demand, inventory cycles, capacity, end-market exposure, and capital spending intensity. | Revenue by end market, gross-margin cycle, order visibility, inventory levels, foundry exposure, and capex requirements. |

| Cyclical and defensive sector context | How sensitive a business may be to economic expansion, contraction, rates, or consumer demand. | Revenue volatility, pricing power, cost flexibility, demand elasticity, balance-sheet resilience, and cash-flow stability. |

| Sector-specific margin and cash-flow drivers | Why margins or free cash flow differ across business models even when headline growth looks similar. | Cost structure, working-capital needs, reinvestment intensity, maintenance capex, customer concentration, and operating leverage. |

| Future sector-specific pages | A sector needs a dedicated path because its drivers cannot be covered safely with a generic stock-analysis checklist. | Sector-specific unit economics, reporting conventions, risk factors, and company-comparison metrics. |

How to Do Sectoral Analysis Without Turning It Into an Outlook

Start with the business model. Ask how companies in the sector make money, what inputs they depend on, and which costs move with revenue.

Separate sector drivers from company execution. A favorable sector backdrop can still contain weak companies, and a difficult sector can still contain businesses with stronger balance sheets, better margins, or more durable cash flow.

Identify the evidence that matters most. For banks, that may be credit quality and funding structure. For SaaS companies, it may be retention and customer acquisition efficiency. For semiconductor businesses, it may be inventory, capacity, end-market demand, and margin cyclicality.

Move from sector lens to company proof. The sector lens decides which questions to ask. The company evidence decides whether the individual business deserves deeper valuation work.

Priority Paths for Sector Analysis

- If the question is bank-specific, start with credit quality, deposits, rate sensitivity, and capital adequacy before comparing valuation multiples.

- If the question is recurring-revenue or software-specific, start with retention, churn, ARR movement, sales efficiency, gross margin, and cash burn.

- If the question is semiconductor-cycle-specific, start with demand visibility, inventories, capacity, end-market exposure, and gross-margin cyclicality.

- If the question is broad sector performance, do not treat sector analysis as a live ranking tool or allocation signal.

- If the question is company quality, use sector analysis only as context before reviewing financial statements, business model durability, and valuation assumptions.

Sector Analysis Is Not a Sector Outlook

Sector analysis can help organize company research, but it does not predict returns, identify the best sector to buy, or prove that a stock is safe. It also should not be used as a substitute for company-level evidence.

A current sector outlook asks what may happen next in markets. A sector-analysis route asks which business drivers matter before evaluating an individual company. Those are different jobs. Mixing them can lead to weak conclusions, especially when a sector label is used as a shortcut for earnings quality, balance-sheet strength, or valuation support.

Where to Go Next

Start with the bank route when deposits, credit quality, loan losses, rate sensitivity, and capital strength are the main issues behind the company analysis.

Use the SaaS route when recurring revenue, retention, churn, software margins, sales efficiency, and cash burn are the main evidence areas.

For other sectors, keep the same decision logic: identify the sector-specific driver first, then evaluate the individual company using the evidence that matters for that business model.

Sector Analysis FAQ

What is sector analysis?

Sector analysis is the process of studying the drivers, risks, and financial patterns that shape companies within a business sector. In investor research, it helps decide which company-level evidence matters before comparing individual stocks.

How do you do sectoral analysis in the stock market?

Start by identifying the sector’s business model, revenue drivers, margin structure, cyclicality, regulation, capital intensity, and cash-flow behavior. Then use that context to decide which company metrics and risks deserve closer review.

What is the difference between sector analysis and industry analysis?

Sector analysis starts with a broad business area, while industry analysis usually works at a narrower comparison level inside that sector. Both can be useful, but company analysis still depends on business-model evidence, financial statements, and valuation context.

Is sector analysis the same as sector rotation?

No. Sector rotation focuses on changing market leadership or allocation across sectors. Sector analysis focuses on understanding how sector-specific business drivers affect company research.