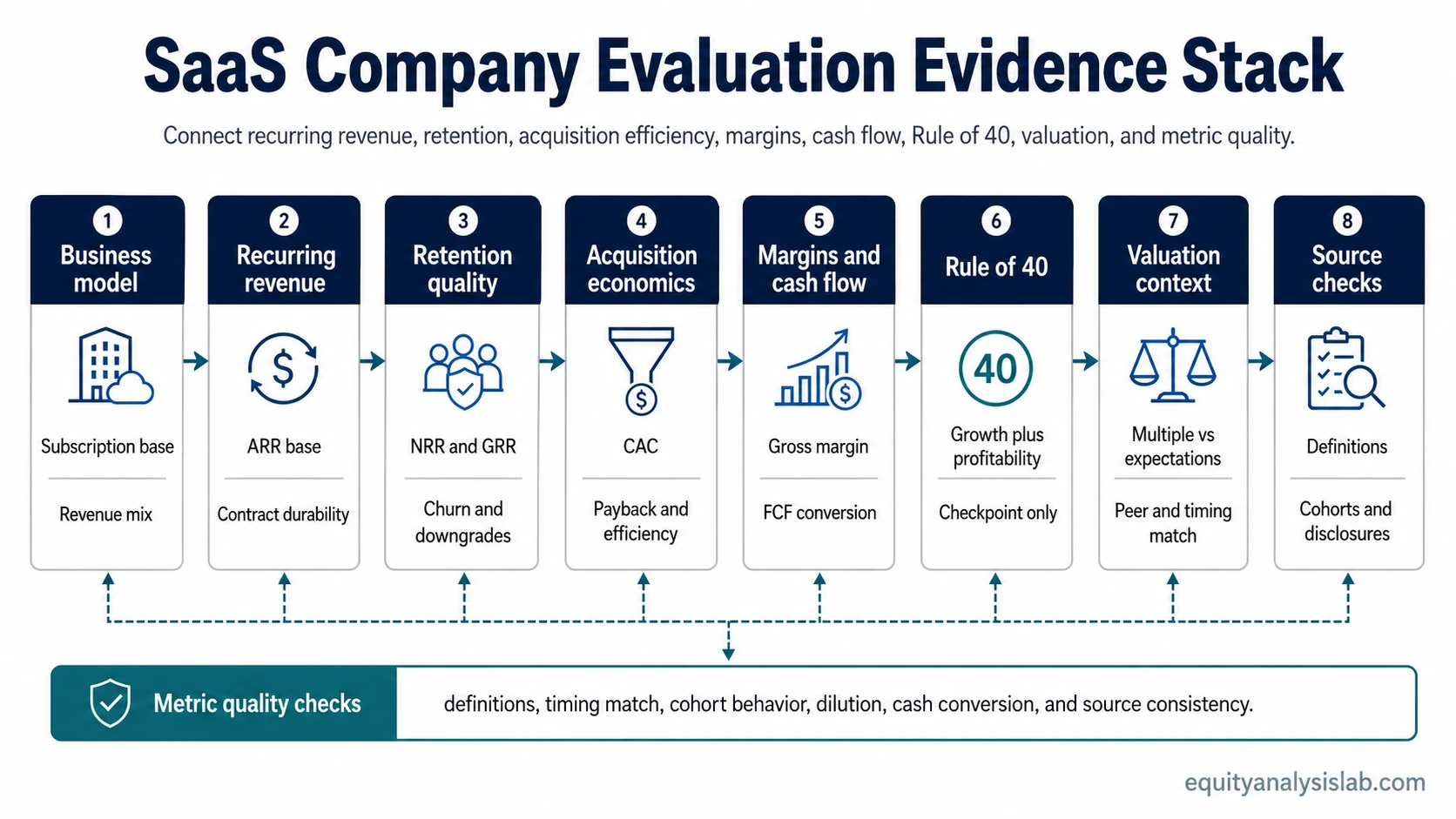

To evaluate a SaaS company, start with the durability of recurring revenue, then test retention, acquisition efficiency, margin structure, cash conversion, growth quality, and valuation context together.

No single SaaS metric is enough on its own. ARR can grow while churn weakens the customer base. Retention can look strong while acquisition cost rises. A valuation multiple can look reasonable while cash conversion, dilution, or growth durability is getting worse.

The practical sequence is to ask what the company sells, how recurring the revenue really is, whether customers stay and expand, how expensive new growth is, whether margins can scale, and whether the valuation already prices in too much future improvement.

Key Points

- SaaS company analysis starts with recurring revenue durability, not with the valuation multiple.

- Retention quality matters because recurring revenue is less valuable when churn, downgrades, or weak customer expansion offset new bookings.

- Customer acquisition cost must be compared with payback, gross margin, sales efficiency, and customer durability.

- Rule of 40 is useful as a growth and profitability checkpoint, but weak inputs can make the score misleading.

- SaaS valuation multiples need context from growth, retention, margins, cash flow, peer quality, dilution, and market conditions.

How Investors Evaluate SaaS Companies

SaaS analysis works best as an evidence sequence. The business model comes first, because subscription revenue only deserves a quality premium when customers remain, expand usage, and produce attractive economics over time.

Revenue growth is the starting signal, not the conclusion. A company can grow quickly by spending heavily on sales and marketing, discounting contracts, selling to less durable customers, or issuing equity to fund losses. Growth becomes more durable when the revenue base is recurring, retention is strong, payback is reasonable, gross margin is healthy, and cash flow is moving in the right direction.

Valuation belongs near the end of the process. A SaaS company with strong growth, high retention, improving margins, and disciplined acquisition economics may deserve a different multiple than a slower, churn-heavy business with weak cash conversion. The multiple is the summary of expectations, not the proof that the business is attractive.

Start With the SaaS Business Model

A SaaS company sells software access through a recurring contract or subscription model. The model can be attractive because revenue may repeat across periods, but the quality of that repeat revenue depends on customer behavior, contract terms, product necessity, and competitive pressure.

Recurring revenue is stronger when customers rely on the software for ongoing workflows, renew without heavy discounting, and expand usage as the customer grows. It is weaker when the product is easy to cancel, easy to replace, or tied to short-lived budget cycles.

Business model quality also depends on revenue mix. Enterprise contracts, usage-based revenue, seat-based pricing, professional services, implementation revenue, and partner revenue can behave differently. Stronger disclosure usually makes clear which revenue streams are recurring, which are one-time, and which depend on customer expansion.

Definition: A SaaS company is evaluated by testing whether subscription revenue is durable, profitable to acquire, scalable through margins, and reasonably priced relative to future growth and cash generation.

Test Recurring Revenue Quality

Annual recurring revenue shows the recurring revenue base the company expects to carry forward. ARR is useful because it helps separate subscription momentum from one-time revenue, but it does not prove revenue quality by itself.

The next question is whether the recurring base is stable, expanding, or leaking. Net revenue retention helps show whether existing customers are expanding after churn and downgrades. Gross revenue retention focuses more narrowly on how much revenue remains before expansion revenue is added back.

SaaS churn rate is the pressure point behind the retention story. A company can report strong new bookings while existing customers quietly leave, downgrade, or reduce usage. Churn is especially important when growth depends on replacing lost revenue before the business can compound.

Disclosure quality matters. Retention metrics become more useful when the company explains customer cohorts, enterprise versus smaller customer behavior, expansion revenue, downgrade pressure, and changes in pricing or packaging.

Check Customer Acquisition Economics

Fast SaaS growth is more valuable when new customers can be acquired at an attractive cost. SaaS customer acquisition cost helps estimate how much sales and marketing effort is needed to add new paying customers.

CAC should not be read in isolation. A company can show strong revenue growth while payback periods stretch, sales efficiency weakens, or new customers arrive with lower retention quality. Acquisition spend is more productive when it creates durable recurring revenue rather than short-lived bookings.

CAC payback period connects acquisition spend to the time needed to recover that spend through customer gross profit. Shorter payback generally gives the company more flexibility, while longer payback increases dependence on outside funding, flawless execution, or continued investor patience.

Limitation: LTV/CAC can look precise while relying on aggressive lifetime, churn, margin, or upsell assumptions. For public investors, payback, retention, gross margin, sales efficiency, and cash flow often provide a cleaner cross-check than a single lifetime-value ratio.

Evaluate Margin Structure and Cash Conversion

SaaS companies often have high potential operating leverage, but that potential has to show up through the income statement and cash-flow statement over time. Gross margin is the first margin checkpoint because it shows how much revenue remains after direct service delivery costs.

High gross margin can support attractive economics, but it does not guarantee operating profitability. Sales and marketing, research and development, customer support, hosting costs, stock-based compensation, and general administrative expenses can absorb the gross profit before it becomes operating income or free cash flow.

Cash conversion is especially important for growth software companies. A company can report strong revenue growth while free cash flow stays weak because acquisition spend, implementation costs, billing terms, or dilution carry the business. A stronger SaaS profile usually shows a path from growth to cash generation without relying only on equity issuance or optimistic future margin assumptions.

Use Rule of 40 as a Checkpoint, Not a Verdict

Rule of 40 combines growth and profitability into one checkpoint. It can help compare SaaS companies that are growing at different speeds or operating at different maturity levels.

The score becomes more useful when the inputs are clean. Revenue growth driven by weak retention, heavy discounting, or inefficient sales spend is not the same as growth supported by customer expansion and strong payback. Profitability supported by underinvestment may also be less durable than profitability created by real operating leverage.

Rule of 40 should therefore be used as a screening question: is the company balancing growth and profitability in a way that looks durable? The answer still depends on retention, CAC payback, gross margin, cash flow, product quality, and valuation.

Put SaaS Valuation Multiples in Context

SaaS valuation multiples compare company value with a revenue or ARR base. The multiple is easy to quote, but it is easy to misuse when the revenue base, timing, growth rate, retention profile, and margin structure are not aligned.

A higher multiple may reflect stronger growth, better retention, higher gross margin, stronger free cash flow potential, a larger market opportunity, or better peer quality. A lower multiple may reflect slower growth, weaker retention, customer concentration, lower margins, dilution risk, or uncertainty about future profitability.

Multiple compression is a major valuation risk. Even if revenue grows, the stock can struggle if investors reduce the multiple they are willing to pay for that revenue. That risk rises when growth slows, cash conversion disappoints, retention weakens, or the broader market pays less for long-duration growth.

SaaS Company Evaluation Route Map

A strong SaaS review connects each metric to the business question it is supposed to answer. The same metric can be useful, weak, or misleading depending on the surrounding evidence.

| Analysis question | Evidence to check | What can distort the reading | Concept to study next |

|---|---|---|---|

| Is the revenue base durable? | Subscription mix, contract terms, renewal behavior, customer dependency | One-time services, weak disclosure, short contracts, heavy discounts | Recurring revenue |

| How large is the recurring base? | ARR, MRR, revenue mix, reported recurring revenue definitions | Different ARR definitions, one-time revenue included in the base, acquisition effects | Annual recurring revenue |

| Are existing customers expanding? | NRR, expansion revenue, upsell, cross-sell, seat growth, usage growth | Price increases masking usage weakness, large-customer concentration, temporary expansion | Net revenue retention |

| Are customers staying before expansion is counted? | GRR, logo retention, downgrade behavior, cohort stability | Expansion hiding base churn, weak cohort disclosure, customer mix shifts | Gross revenue retention |

| How much revenue is leaking? | Revenue churn, logo churn, downgrades, contraction, renewal rates | New bookings offsetting churn, annual averages hiding recent deterioration | SaaS churn rate |

| How expensive is new growth? | CAC, sales and marketing spend, new customer additions, sales efficiency | Long sales cycles, channel mix changes, discounting, weak customer durability | SaaS customer acquisition cost |

| How long does acquisition spend take to recover? | CAC payback, gross profit contribution, cohort economics | Aggressive margin assumptions, delayed churn, customer mix changes | CAC payback period |

| Can revenue become profitable at scale? | Gross margin, hosting cost, support cost, implementation cost, product delivery cost | Low-margin services, infrastructure cost pressure, underpriced contracts | Gross margin |

| Is the company balancing growth and profitability? | Revenue growth, operating margin, free cash flow margin, trend direction | Poor input quality, underinvestment, one-year margin boosts, weak retention | Rule of 40 |

| Does the valuation match the evidence? | Revenue multiple, ARR multiple, growth, retention, margin quality, peer context | Wrong peer set, mismatched timing, multiple compression, dilution, growth deceleration | SaaS valuation multiples |

Common Mistakes When Evaluating SaaS Companies

Treating ARR as automatically high quality: ARR is useful only when the recurring base is durable. Weak retention, discounting, short contracts, or unclear definitions can make the headline number less reliable.

Ignoring churn composition: Logo churn, revenue churn, downgrades, and contraction can tell different stories. Expansion revenue can hide weakness in the underlying customer base.

Overvaluing growth without payback: Revenue growth funded by inefficient acquisition spend may not create durable value. CAC, payback, gross margin, and cash flow need to support the growth story.

Using Rule of 40 as a stock-rating tool: The score is a checkpoint, not a full investment conclusion. Input quality, trend direction, valuation, and business durability still matter.

Reading valuation multiples without context: A multiple can look cheap or expensive for good reasons. Growth durability, retention quality, margin structure, cash conversion, dilution, and peer quality change the interpretation.

When a SaaS Company Looks Strong but Needs More Testing

A SaaS company can look attractive when revenue growth is high, ARR is expanding, and the market still rewards software growth. The evidence becomes weaker if churn is rising, payback is stretching, gross margin is compressing, or dilution is funding the growth.

A stronger review separates growth from growth quality. Durable growth is supported by customers staying, expanding, and producing attractive gross profit over time. Lower-quality growth depends more heavily on new sales spend, optimistic retention assumptions, or valuation support that may not survive a slower growth period.

FAQ

What is the first thing to check when evaluating a SaaS company?

Start with recurring revenue durability. Revenue growth is more useful when the company has a stable subscription base, strong retention, clear revenue definitions, and customers that keep using or expanding the product.

Is ARR enough to evaluate a SaaS business?

No. ARR shows the recurring revenue base, but it does not prove customer quality, retention strength, acquisition efficiency, profitability, or valuation discipline.

Why can SaaS valuation multiples be misleading?

A SaaS multiple can be misleading when the revenue base, growth rate, retention quality, margin profile, cash flow, peer set, or timing period is mismatched. The multiple needs business-quality context.

Should Rule of 40 be used as a final verdict?

No. Rule of 40 is a checkpoint for growth and profitability balance. It still depends on the quality of revenue growth, retention, margins, cash conversion, and valuation context.