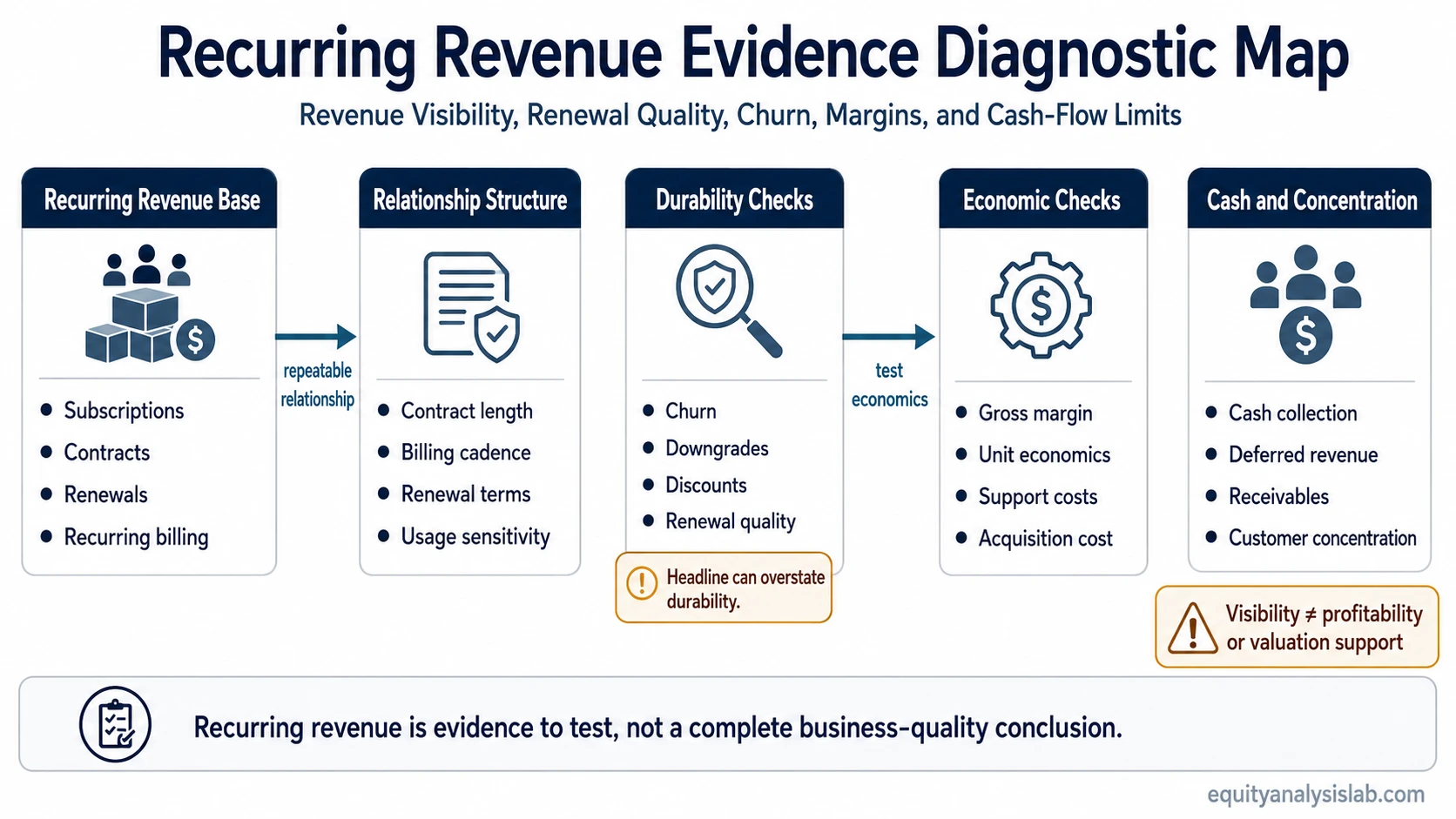

Recurring revenue is revenue a company expects to receive repeatedly from customers through a subscription, contract, renewal relationship, or recurring payment pattern.

Recurring revenue can improve visibility into future sales, but it does not automatically prove business quality, pricing power, profitability, cash conversion, or valuation support. The useful investor question is not only whether revenue repeats, but whether that recurring base is durable, profitable, cash-generative, and difficult to replace.

Definition: Recurring revenue is repeatable customer revenue tied to an ongoing relationship, such as a subscription, service contract, maintenance agreement, renewal plan, licensing arrangement, or recurring billing structure.

Key Points

- Recurring revenue means customer revenue that is expected to repeat across periods.

- It can improve revenue visibility, especially when contracts, renewals, or subscriptions are stable.

- The quality of recurring revenue depends on churn, renewal behavior, margins, unit economics, and cash conversion.

- ARR and MRR are narrower recurring revenue metrics, mostly used in subscription and SaaS-style models.

- Recurring revenue is business-model evidence, not a complete business-quality conclusion.

What Is Recurring Revenue?

Recurring revenue describes a revenue pattern where customers continue paying over time instead of buying once and disappearing from the revenue base. The payment may be monthly, annual, usage-linked, contract-based, or renewal-based, but the core idea is the same: the company has some ongoing customer relationship that can repeat revenue across future periods.

A subscription software company, a maintenance provider, a membership business, a licensing model, or a service contract can all contain recurring revenue. A company can also have a mixed model where some revenue is recurring and some comes from one-time projects, hardware sales, implementation fees, or transaction events.

The recurring label is only the starting point. A revenue stream can be repeatable but fragile if customers can cancel quickly, renew only after heavy discounts, downgrade often, or require high support and acquisition costs to keep the relationship alive.

How Recurring Revenue Is Calculated or Observed

Recurring revenue is usually observed by identifying the revenue base that is expected to repeat during a defined period. The calculation depends on the business model, reporting detail, billing cadence, and whether management separates recurring revenue from non-recurring revenue in disclosures.

| Input | What to check | Why it matters |

|---|---|---|

| Revenue base | Which customer payments are counted as recurring | Separates repeatable revenue from one-time fees, services, or project work |

| Time period | Monthly, quarterly, annual, or contract-period basis | Prevents mixing short-period billing with long-period revenue claims |

| Billing cadence | Monthly billing, annual prepayment, renewal billing, or usage-based billing | Shows whether reported recurrence also supports cash collection timing |

| Customer or contract base | Active customers, active contracts, subscribers, seats, accounts, or licenses | Links the revenue figure to a real customer relationship |

| Churn and downgrades | Cancellations, non-renewals, seat reductions, price cuts, or usage declines | Tests whether the recurring base is durable or shrinking underneath the headline number |

| Expansions | Upsells, price increases, seat growth, cross-sell, or usage expansion | Shows whether recurring revenue grows from existing customers or mostly from new acquisition |

| Exclusions | Setup fees, implementation work, hardware, consulting, pass-through costs, or one-time services | Reduces the risk of overstating the repeatable part of the business |

| Accounting base | Recognized revenue, billings, deferred revenue, or cash collected | Distinguishes reported revenue visibility from actual cash movement |

ARR and MRR are common ways to express recurring revenue in subscription and SaaS-style models. Annual recurring revenue annualizes a recurring revenue base, while monthly recurring revenue expresses it on a monthly basis. Those metrics can be useful, but they are narrower than the broader recurring revenue concept.

Recurring Revenue vs Non-Recurring Revenue

Recurring revenue is expected to repeat because the customer relationship continues. Non-recurring revenue comes from one-time sales, project work, implementation fees, special transactions, equipment sales, or other events that may not repeat without a new sale.

| Revenue type | Typical source | Investor interpretation |

|---|---|---|

| Recurring revenue | Subscriptions, contracts, renewals, licenses, maintenance, membership fees | Can support visibility if churn, renewal quality, and cash conversion are sound |

| Non-recurring revenue | One-time sales, project fees, setup work, hardware, custom services, special transactions | May still be valuable, but future sales usually require new demand or new contract wins |

| Repeat purchasing | Customers buying again without a formal recurring structure | Can show customer habit, but it is not the same as contracted or subscription recurrence |

| Usage-based recurring revenue | Ongoing customer usage with variable billing | Can be recurring in relationship but volatile in amount if usage changes materially |

Repeat purchasing is a common source of confusion. A customer who buys the same product every few months may be loyal, but that does not automatically create recurring revenue. The distinction depends on whether there is an ongoing revenue structure, not merely a history of repeated purchases.

What Recurring Revenue Can Tell Investors

Recurring revenue can make future sales easier to analyze because part of the revenue base may already be tied to existing customers. That can improve forecasting, reduce dependence on new one-time sales, and make customer retention more visible.

The strongest recurring revenue is not only repeatable. It is also supported by renewal behavior, healthy gross margins, reasonable customer acquisition cost, low downgrade pressure, strong cash collection, and limited customer concentration. A high recurring revenue percentage with weak economics can still produce a low-quality business result.

| Diagnostic question | Stronger evidence | Weaker evidence |

|---|---|---|

| Does the revenue actually renew? | Long renewal history, low churn, stable customer base | Frequent cancellations, short contracts, high downgrade activity |

| Is the revenue profitable? | High gross margin and controlled support costs | Heavy service burden, discounting, or low-margin pass-through revenue |

| Does recurrence convert into cash? | Reliable collection, favorable billing terms, limited receivable stress | Revenue recognized faster than cash arrives or collections deteriorate |

| Is the base diversified? | Many customers, limited dependence on one account or contract | A few large renewals dominate the recurring revenue base |

| Can pricing improve? | Customers renew despite measured price increases | Renewals depend on discounts or concessions |

A recurring revenue business model may reduce uncertainty, but the economic value depends on the cost and durability of keeping that revenue. Strong narrative language around repeatable sales can still mislead when margins, retention, or cash flow do not support the story.

When Recurring Revenue Can Mislead

Recurring revenue can create false comfort when the headline percentage hides weak economics. Monthly cancellable subscriptions, incentive-driven renewals, high churn, low switching friction, bundled revenue, or large customer concentration can make the recurring base less durable than it first appears.

Limitation: Recurring revenue improves visibility only when the customer base, contract structure, renewal behavior, margins, and cash collection support the claim. Visibility is not the same as profitability or cash generation.

Low-margin recurring revenue can also overstate quality. A business may keep revenue repeating while spending heavily on support, onboarding, discounts, service delivery, or customer acquisition. In that case, the recurring revenue label may describe the sales pattern without proving that the business creates attractive economics.

Usage sensitivity is another risk. Some models have recurring customer relationships but variable revenue amounts. If customers stay active while reducing usage, seats, transaction volume, or spending tiers, the relationship may remain intact while revenue weakens.

Recurring Revenue Example

Two hypothetical companies both report that 80% of revenue is recurring. Company A has multi-year contracts, low churn, stable renewals, high gross margin, and strong cash collection. Company B has monthly cancellable plans, heavy discounting, high churn, concentrated customers, and weak cash conversion.

The same 80% headline does not carry the same meaning in both cases. Company A’s recurring revenue may provide stronger evidence of revenue durability. Company B’s recurring revenue may still repeat on paper, but the economics behind that recurrence are less reliable.

Example interpretation: A recurring revenue percentage is more useful after checking what keeps the revenue recurring, what it costs to maintain, and whether it converts into cash.

Recurring Revenue and Related Business Model Features

Recurring revenue describes how customer revenue repeats. It is different from an asset-light business model, which focuses on the asset base required to operate the company.

A company can have recurring revenue and still require high infrastructure spending, working capital, onboarding costs, or customer acquisition investment. That is why recurring revenue should be evaluated alongside capital intensity, not treated as a standalone quality label.

Recurring revenue also does not automatically create cost efficiency. If fixed costs, service costs, or acquisition costs grow nearly as fast as revenue, the business may not benefit from stronger operating leverage or better cost behavior as activity grows.

FAQ

What is recurring revenue?

Recurring revenue is repeatable customer revenue that a company expects to receive across future periods through subscriptions, contracts, renewals, recurring billing, or ongoing customer relationships.

Is recurring revenue the same as ARR or MRR?

No. ARR and MRR are narrower recurring revenue metrics, commonly used in subscription and SaaS-style models. Recurring revenue is the broader concept.

Is recurring revenue always better than non-recurring revenue?

No. Recurring revenue can improve visibility, but non-recurring revenue can still be profitable and valuable. The comparison depends on margins, retention, cash conversion, customer concentration, and the cost of generating revenue.

Why can recurring revenue mislead investors?

Recurring revenue can mislead when the headline figure hides high churn, low margins, weak collections, heavy discounts, short cancellation windows, or dependence on a small number of customers.