Business model features help investors separate how a company earns revenue, carries costs, reinvests capital, scales operations, and keeps customers. The useful first step is matching each feature to the investor question it answers.

Definition: Business model features are the structural traits that shape how a company makes money, what resources it needs, how margins can change, and whether customer or scale advantages may become durable.

A feature is not an investment conclusion. Recurring revenue, network effects, scale benefits, or an asset-light structure can improve the quality of a business model, but each claim still needs evidence from margins, cash flow, reinvestment needs, customer behavior, and competition.

Key Points

- Business model features are analysis prompts, not proof that a stock is attractive.

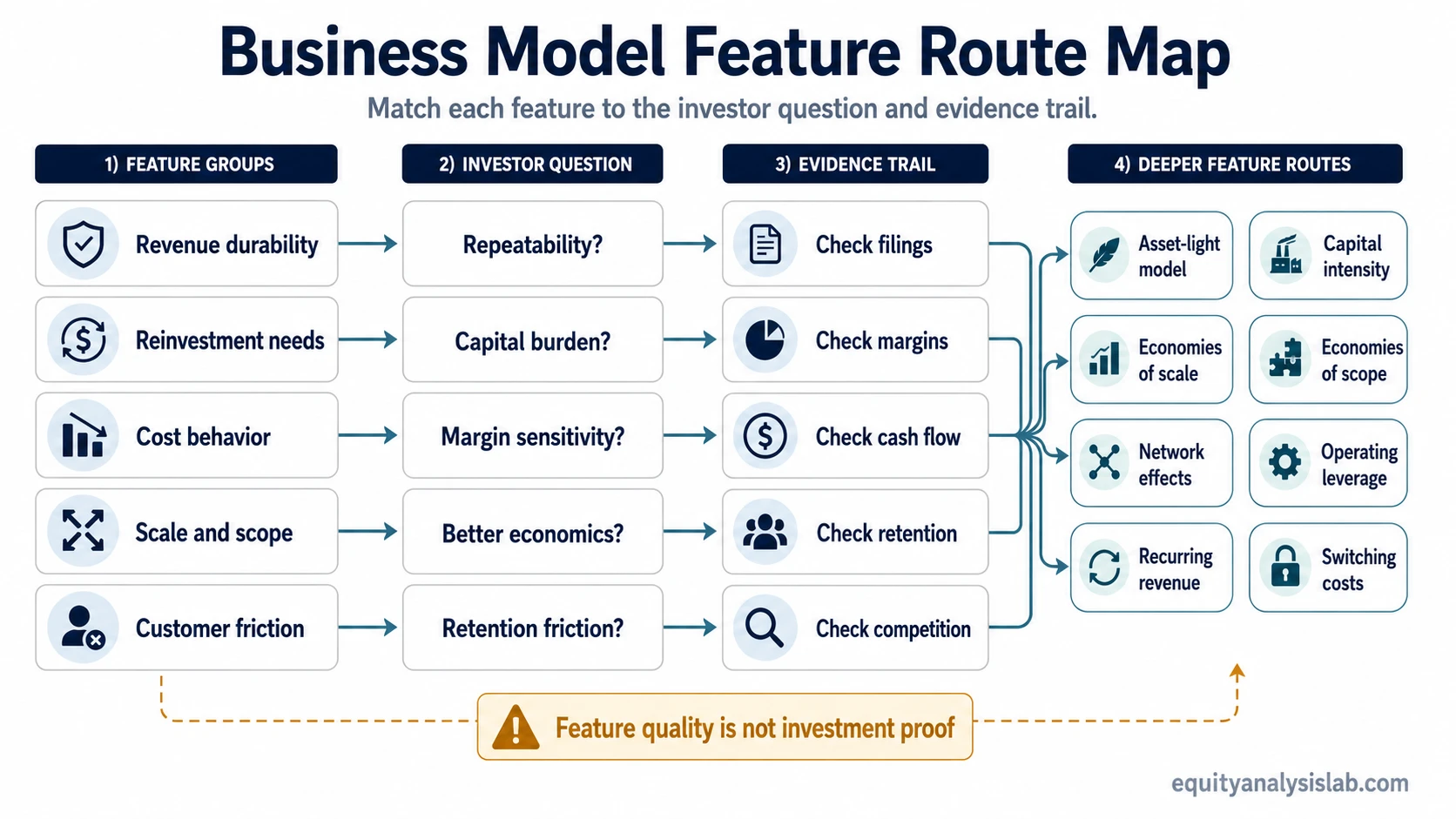

- Revenue durability, reinvestment needs, cost behavior, scale effects, and customer friction answer different investor questions.

- The strongest feature to check first is usually the one tied to the biggest uncertainty in the company analysis.

- Evidence should come from filings, financial statements, management discussion, margin history, retention indicators, and competitive context.

Business Model Feature Groups Investors Usually Separate

Business model analysis becomes clearer when features are grouped by the question they answer. Revenue features address repeatability and customer behavior. Cost and capital features address margin sensitivity and reinvestment burden. Competitive features address whether scale, scope, customer lock-in, or user-base effects can make returns harder to copy.

| Feature group | Investor question | Evidence to inspect |

|---|---|---|

| Revenue durability | How repeatable is the revenue base? | Revenue mix, contract structure, renewal behavior, churn, pricing pressure, customer concentration. |

| Reinvestment and asset needs | How much capital is required to maintain or grow the business? | Capital expenditure, working capital, maintenance spending, R&D, sales and marketing intensity. |

| Cost structure and margin sensitivity | How much do profits change when revenue changes? | Gross margin, operating margin, fixed-cost base, contribution margin, cost flexibility. |

| Scale and scope effects | Can growth improve economics across customers, products, or shared capabilities? | Unit costs, shared infrastructure, product breadth, distribution efficiency, margin progression. |

| Customer retention and competitive friction | What makes customers stay or what makes rivals harder to copy? | Retention data, switching friction, user-base value, pricing power, customer alternatives. |

Business Model Feature Route Map

The feature to inspect first depends on the uncertainty in the company. A high-margin company may still need a capital intensity check. A subscription company may still need churn and acquisition-cost checks. A business with strong user growth may still need evidence that user growth improves economics rather than only increasing activity.

| Feature | Investor question | Evidence to check | Use when the main uncertainty is |

|---|---|---|---|

| asset-light business model | Does the company need a large physical asset base to grow? | Capital expenditure, working capital, lease obligations, software or platform spending, customer acquisition cost. | Whether low visible asset needs are translating into real cash conversion. |

| capital intensity | How much reinvestment is required to sustain operations and growth? | Capex-to-revenue, maintenance spending, depreciation, inventory, receivables, capacity expansion. | Whether growth consumes too much capital before shareholders benefit. |

| economies of scale | Can larger volume reduce unit costs or improve margins? | Unit costs, gross margin trend, operating margin trend, fulfillment costs, platform utilization. | Whether size is improving economics or only increasing reported revenue. |

| economies of scope | Can shared capabilities support multiple products or customer needs? | Cross-selling evidence, shared distribution, product bundling, customer overlap, incremental margin. | Whether product breadth creates efficiency or adds complexity. |

| network effects | Does the product become more valuable as more users, suppliers, or participants join? | User growth, engagement, retention, transaction density, marketplace liquidity, pricing power. | Whether a growing user base is creating a defensible advantage. |

| operating leverage | How sensitive are profits to revenue growth or revenue decline? | Fixed costs, variable costs, contribution margin, margin expansion, downside margin compression. | Whether earnings can expand faster than revenue or contract sharply in weakness. |

| recurring revenue | How repeatable is the revenue base? | Subscription mix, renewals, churn, net retention, contract length, pricing changes. | Whether reported revenue is durable or depends on constant replacement of lost customers. |

| switching costs | How difficult is it for customers to leave? | Implementation costs, workflow dependency, data migration, training burden, contract terms, alternatives. | Whether retention comes from real customer friction or only from temporary convenience. |

Which Feature Should Be Checked First?

The starting feature should follow the unresolved investor question. If revenue durability is unclear, begin with recurring revenue and switching costs. If margin swings are the main issue, begin with operating leverage and capital intensity. If the company claims a strong competitive advantage, test network effects, switching costs, economies of scale, and economies of scope before accepting the claim.

Revenue uncertainty: start with retention, renewal behavior, customer concentration, and recurring revenue quality.

Margin uncertainty: compare fixed-cost sensitivity, gross margin durability, reinvestment burden, and operating leverage.

Competitive advantage uncertainty: look for evidence that scale, user-base effects, switching friction, or shared capabilities improve customer economics.

Asset-light uncertainty: check whether reinvestment is hidden in R&D, sales and marketing, customer acquisition, or platform spending.

Evidence Prompts by Feature

Business model features become more useful when they are tied to observable evidence. Investor materials can describe a feature, but the financial statements and operating disclosures determine whether the feature is visible in results.

| Evidence prompt | What it can clarify | Where it may appear |

|---|---|---|

| Revenue mix | Whether revenue is recurring, transactional, usage-based, cyclical, or concentrated. | Revenue notes, segment reporting, management discussion, investor presentations. |

| Gross and operating margins | Whether scale, pricing, cost structure, or mix shifts are improving or weakening economics. | Income statement, segment margin disclosure, earnings commentary. |

| Capital expenditure and working capital | Whether growth requires heavy reinvestment before cash can compound. | Cash flow statement, balance sheet, notes to financial statements. |

| Retention, churn, or renewal indicators | Whether repeat revenue and switching friction are visible in customer behavior. | Operating metrics, cohort disclosures, SaaS metrics, customer commentary when available. |

| Customer concentration | Whether revenue quality depends on a small number of buyers or contracts. | Risk factors, customer concentration notes, segment disclosures. |

| Unit economics | Whether customer acquisition, fulfillment, support, and retention costs support profitable growth. | Management discussion, investor materials, segment data, operating metrics when available. |

Common Mistakes When Reading Business Model Features

Limitation: A strong business model feature can improve analysis, but it does not prove valuation attractiveness, investment quality, or future return. The feature still has to survive valuation, balance-sheet, cash-flow, management, and competitive checks.

Recurring revenue can still be low quality if churn is high, customer acquisition cost is rising, pricing power is weak, or a small group of customers controls the revenue base. Network effects can be overstated if user growth does not improve retention, liquidity, engagement, or pricing power. Asset-light economics can be overstated if the company needs continuous spending on marketing, product development, incentives, or support to keep growth from fading.

The safer interpretation is comparative. A feature matters most when it changes the evidence trail: better cash conversion, more stable margins, lower reinvestment burden, stronger retention, or clearer durability against competitors.

Simple Business Model Feature Scenario

A software company reports a high share of subscription revenue, but renewal rates are weakening and sales costs are rising. The recurring revenue label may still be useful, but the investor question shifts toward retention quality, acquisition cost, pricing pressure, and cash conversion.

A different company may look asset-light because it owns few physical assets, but growth still depends on heavy product development and customer acquisition spending. The asset-light label becomes more convincing only when cash flow shows that reinvestment needs are not absorbing most of the operating profit.

FAQ

Are business model features enough to judge a company?

No. Business model features organize the analysis, but they do not replace valuation, balance-sheet review, cash-flow analysis, management assessment, or competitive research.

Which business model feature should investors check first?

The first feature should match the largest uncertainty. Revenue uncertainty points toward recurring revenue and switching costs. Margin uncertainty points toward operating leverage and capital intensity. Competitive advantage uncertainty points toward scale, scope, network effects, and customer retention friction.

Can an attractive feature still lead to weak business quality?

Yes. A company can have an attractive feature on the surface while still facing churn, margin pressure, customer concentration, high reinvestment needs, weak cash conversion, or intense competition.