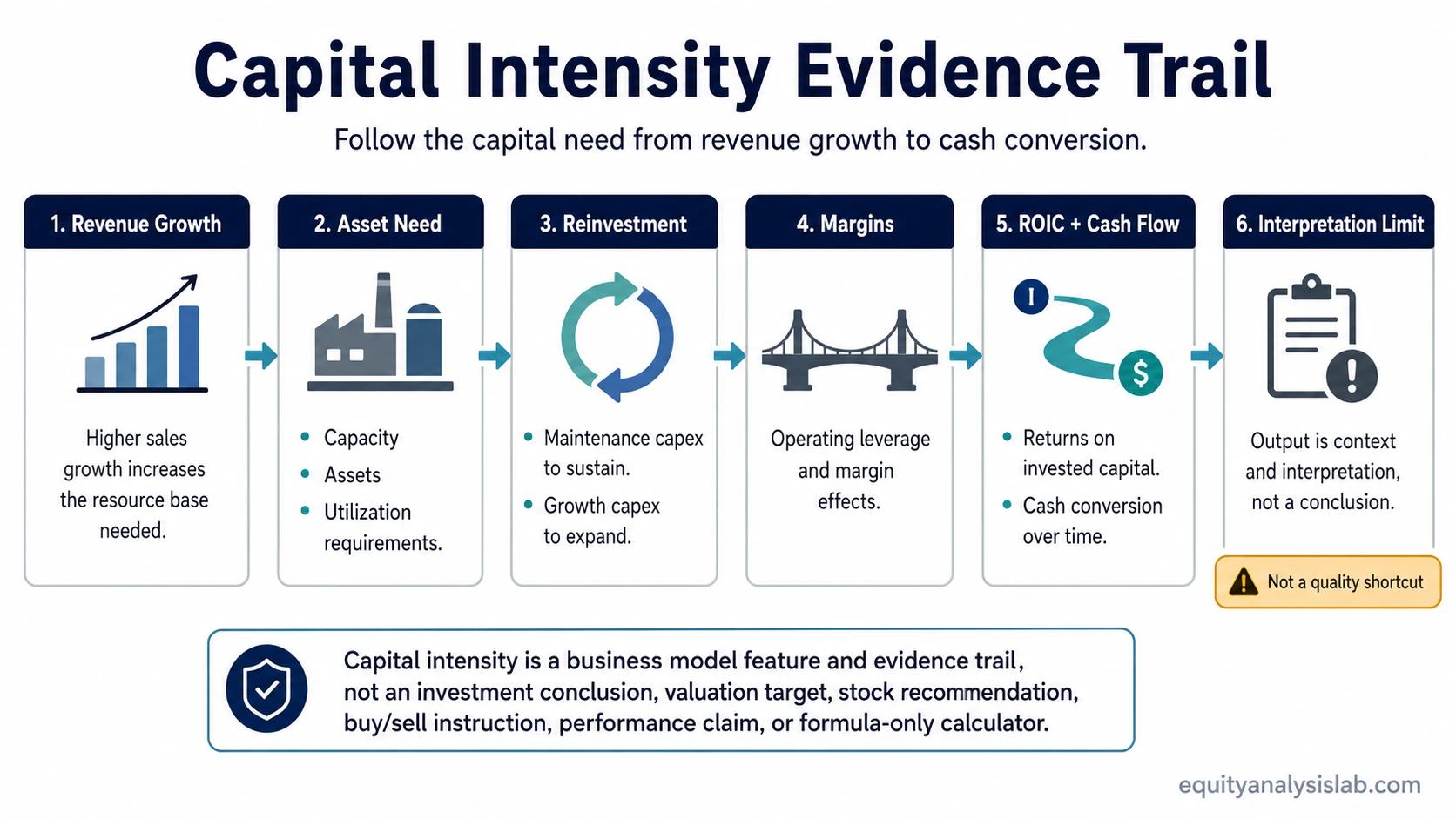

Capital intensity describes how much capital a business must commit to assets, capacity, infrastructure, inventory, or operating base before it can generate and expand revenue. For investors, the concept matters because revenue growth may require ongoing reinvestment before it becomes free cash flow.

Capital intensity is a business model feature, not an investment conclusion. A capital-intensive business may need factories, equipment, aircraft, networks, energy assets, stores, inventory, or specialized infrastructure to operate. A lower-capital business may produce revenue with fewer physical assets, but that does not automatically make it higher quality.

The useful question is not only whether the business uses a lot of capital. The stronger question is whether the capital base earns acceptable returns, protects the competitive position, supports scale, and leaves enough cash after maintenance and growth reinvestment.

What Is Capital Intensity?

Capital intensity is the amount of capital required to support a company’s revenue, production capacity, or operating footprint. A business is more capital intensive when growth requires large investments in fixed assets, equipment, infrastructure, facilities, inventory, or other operating assets.

A capital-intensive business often needs to spend before it can grow. Capacity may need to be built, maintained, replaced, or upgraded before the next unit of revenue arrives. That creates a different investor question than a business that can add revenue mainly through software, licensing, distribution, or existing customer relationships.

Capital intensity becomes most useful when it is connected to cash conversion. A company can report revenue growth and accounting profit while still consuming cash if the asset base constantly requires maintenance capex, replacement spending, inventory, or capacity expansion.

How Capital Intensity Is Calculated

Capital intensity is commonly measured by comparing the capital base to revenue. The exact version depends on the analysis, but the goal is the same: estimate how much capital is needed to produce a given amount of sales.

Common capital intensity ratio:

Average total assets ÷ revenue

Alternative analytical version:

Invested capital ÷ revenue

A higher ratio usually means the business needs more capital to support each unit of revenue. A lower ratio usually means the business can generate revenue with fewer assets. The ratio should be interpreted with the company’s sector, asset age, lease structure, outsourcing model, and accounting treatment in mind.

Capital intensity also connects to asset turnover. A business with a large asset base must generate enough revenue from those assets to justify the capital tied up in them. Low asset turnover is not automatically bad, but it raises the bar for margins, durability, and return on invested capital.

What Capital Intensity Shows About a Business Model

Capital intensity reveals how much of a company’s growth depends on physical capacity, infrastructure, working assets, or replacement spending. That makes it a useful lens for understanding reinvestment burden, scalability, cash conversion, and business model resilience.

| Business model signal | What to look for | Investor interpretation |

|---|---|---|

| Reinvestment burden | Capex needs, replacement assets, maintenance spending, growth projects | Revenue growth may require repeated capital commitments before cash flow improves. |

| Fixed-cost base | Depreciation, facilities, network costs, utilization, capacity expenses | High fixed costs can improve margins when utilization rises, but can pressure margins when demand weakens. |

| Cash conversion | Operating cash flow, capex, working capital, replacement cycle | Reported profit may not fully translate into owner-relevant cash generation. |

| Capital productivity | Revenue per asset dollar, invested capital turnover, ROIC trend | A heavy asset base can still be attractive if it produces durable returns above the cost of capital. |

| Capacity dependence | Utilization rate, expansion plans, bottlenecks, demand cycle | Growth can be constrained by capacity, and unused capacity can drag on profitability. |

The same revenue growth rate can have different meanings across business models. One company may grow by adding users to an existing platform, while another may need new plants, aircraft, towers, equipment, or inventory. The second company may still be attractive, but the cash-flow path is usually more capital dependent.

Capital-Intensive vs Capital-Light Businesses

A capital-intensive business usually needs substantial assets to operate or grow. Utilities, airlines, telecom networks, manufacturers, semiconductor fabrication, energy infrastructure, railways, and some logistics models often have high capital needs because capacity and reliability depend on expensive assets.

An asset-light business model usually relies less on owned physical assets. Software, licensing, marketplace, service, and some distribution models may generate revenue with lower fixed asset requirements.

The distinction can mislead if it becomes a quality shortcut. Capital-light does not automatically mean superior. Capital-intensive does not automatically mean inferior. A capital-light business can have weak retention, poor pricing power, high customer acquisition costs, or fragile margins. A capital-intensive business can have durable demand, regulated returns, scale advantages, or replacement barriers.

The better comparison is like-for-like. A utility should not be judged by the same capital structure expectations as a software company. A capital-intensive airline, telecom network, or manufacturer should be compared against peers with similar asset requirements, utilization cycles, and reinvestment needs.

The Investor Evidence Trail

Capital intensity becomes more useful when it moves from label to evidence. The investor evidence trail connects the capital requirement to revenue growth, margins, cash conversion, and capital productivity.

| Investor question | Evidence to check | Why it matters | Limitation |

|---|---|---|---|

| Does growth require heavy reinvestment? | Capex to sales, fixed assets, expansion projects, maintenance capex clues | Revenue may not convert cleanly into cash if growth needs constant asset spending. | Maintenance capex and growth capex are not always disclosed separately. |

| Is the capital base productive? | Asset turnover, ROIC, capacity utilization, margin trend | Heavy assets can still create value when they generate durable returns. | A low capital intensity ratio is not automatically higher quality. |

| Is the business exposed to cyclicality? | Demand cycle, customer concentration, utilization, fixed-cost structure, operating leverage | Fixed costs can amplify downside when demand or utilization falls. | A capital-intensive business can look worse near a cycle trough and better near a cycle peak. |

| Does scale improve economics? | Unit costs, gross margin, operating margin, capacity use, procurement advantages | Capital intensity can support economies of scale when the asset base is used efficiently. | Scale benefits may fail if demand is weak or the asset base becomes underutilized. |

| Does capital need weaken cash conversion? | Operating cash flow, free cash flow, working capital, replacement capex | Accounting profit may overstate cash available to owners if reinvestment needs are high. | Single-year cash flow can be distorted by cycle timing, inventory swings, or project timing. |

| Do the unit economics justify the asset base? | Contribution margins, payback period, utilization, customer economics, replacement economics | unit economics help show whether the business earns enough at the operating level to support the capital it consumes. | Strong unit economics can be offset by poor capital allocation, weak demand, or excessive replacement needs. |

Capital Intensity, Capital Efficiency, and Business Quality

Capital intensity and capital efficiency are related, but they are not the same. Capital intensity asks how much capital the business requires. Capital efficiency asks how effectively that capital is turned into revenue, profit, cash flow, or returns.

Boundary note: Capital intensity is not the same as asset-light status, valuation attractiveness, economic moat, or business quality. It is one input in the analysis. A capital-heavy company can create value if returns, utilization, pricing, and durability are strong. A capital-light company can destroy value if growth is expensive, churn is high, or margins are weak.

The most important distinction is between capital requirement and capital productivity. A large capital base is a burden only if it fails to produce acceptable returns or if reinvestment absorbs too much cash. A low capital requirement is useful only if the business can defend margins, retain customers, and scale without hidden costs.

When High Capital Intensity Can Be Attractive

High capital intensity can be attractive when the asset base creates a durable advantage rather than only a cost burden. Expensive infrastructure, specialized equipment, regulatory requirements, replacement cost, or capacity control can make it harder for new competitors to replicate the business.

The case becomes stronger when the business earns acceptable returns on invested capital, uses its fixed assets efficiently, maintains pricing discipline, and spreads fixed costs over a larger revenue base. Under those conditions, capital intensity can support operating leverage, scale economics, and durability.

High Capital Intensity Is More Defensible When

- The asset base is hard to replicate or replace.

- Utilization remains high across normal demand cycles.

- Maintenance spending is manageable relative to operating cash flow.

- Incremental capacity can improve unit costs.

- Returns on invested capital remain healthy after reinvestment.

- Customer demand is durable enough to support long asset lives.

The risk is that capital intensity can also lock the company into fixed commitments. If demand weakens, financing costs rise, or assets become obsolete, the same capital base that once supported scale can become a drag on margins and cash flow.

Practical Scenario: Same Growth, Different Cash Conversion

Consider two businesses growing revenue at a similar rate. One can add customers through existing software infrastructure with limited incremental asset spending. The other must build new facilities, buy equipment, hold more inventory, and replace aging assets to support the same revenue growth.

The second business may still be valuable, but the growth is not as cash-light. More of the operating cash flow may need to be recycled into the business before owners see durable free cash flow. The interpretation depends on whether that reinvestment produces stronger returns, capacity advantages, or long-term durability.

Common Mistakes When Interpreting Capital Intensity

Mistake 1: Treating low capital intensity as automatically better. A business with fewer assets can still have weak pricing power, fragile demand, poor retention, or high acquisition costs.

Mistake 2: Treating high capital intensity as automatically bad. Heavy assets can support barriers to entry, regulated returns, scale advantages, or reliable capacity if returns justify the capital.

Mistake 3: Using one formula as the whole thesis. A capital intensity ratio is a starting point. It needs sector context, utilization, margins, reinvestment needs, and return analysis.

Mistake 4: Ignoring maintenance versus growth capex. Growth capex can expand earning power, while maintenance capex is needed to preserve the existing business. The distinction is not always clean in reported financials.

Mistake 5: Comparing unrelated sectors. Capital intensity is most useful inside a relevant peer group. A capital-heavy infrastructure business and a software business operate with different asset requirements.

Related Business Model Features

Capital intensity connects closely with asset-light models, fixed-cost behavior, scale economics, unit economics, and capital productivity. These related concepts help separate the amount of capital required from the quality of returns generated by that capital.

- Asset-light business model: helps compare businesses that can grow with fewer owned assets.

- Operating leverage: helps interpret how fixed costs can magnify margin changes as revenue rises or falls.

- Economies of scale: helps assess whether a large asset base can reduce unit costs as volume grows.

- Unit economics: helps test whether each customer, unit, or transaction supports the capital burden.

- Return on invested capital: helps judge whether the capital base produces acceptable returns.

FAQ

What is capital intensity?

Capital intensity is the amount of capital a business needs to support revenue, production, capacity, or operations. A more capital-intensive business usually needs more assets, infrastructure, equipment, inventory, or facilities to grow.

How is capital intensity calculated?

A common approach is average total assets divided by revenue. Analysts may also use invested capital ÷ revenue when they want a narrower capital-base view. The result should be interpreted with sector context, asset age, lease treatment, utilization, and reinvestment needs.

Is lower capital intensity always better?

No. Lower capital intensity can help cash conversion, but it does not automatically mean the business is better. The company still needs durable demand, pricing power, margins, retention, and capital discipline.

Can a capital-intensive business be attractive?

Yes, if the assets create durable returns, scale advantages, replacement barriers, regulated economics, or capacity advantages. The key is whether the capital base produces acceptable returns after maintenance and growth reinvestment.

How is capital intensity different from capital efficiency?

Capital intensity measures how much capital the business requires. Capital efficiency measures how well that capital is converted into revenue, profit, cash flow, or returns.