Economies of scale are cost advantages that can appear when a business produces, sells, purchases, distributes, or serves more volume at a lower average cost per unit. The basic mechanism is that some costs grow more slowly than activity, so each unit or customer carries a smaller share of the cost base. A scale claim should still be checked against margins, unit economics, cash conversion, and durability rather than accepted from size or revenue growth alone.

Definition: Economies of scale describe a decline in average cost per unit as output, volume, purchasing power, operating capacity, or platform usage increases.

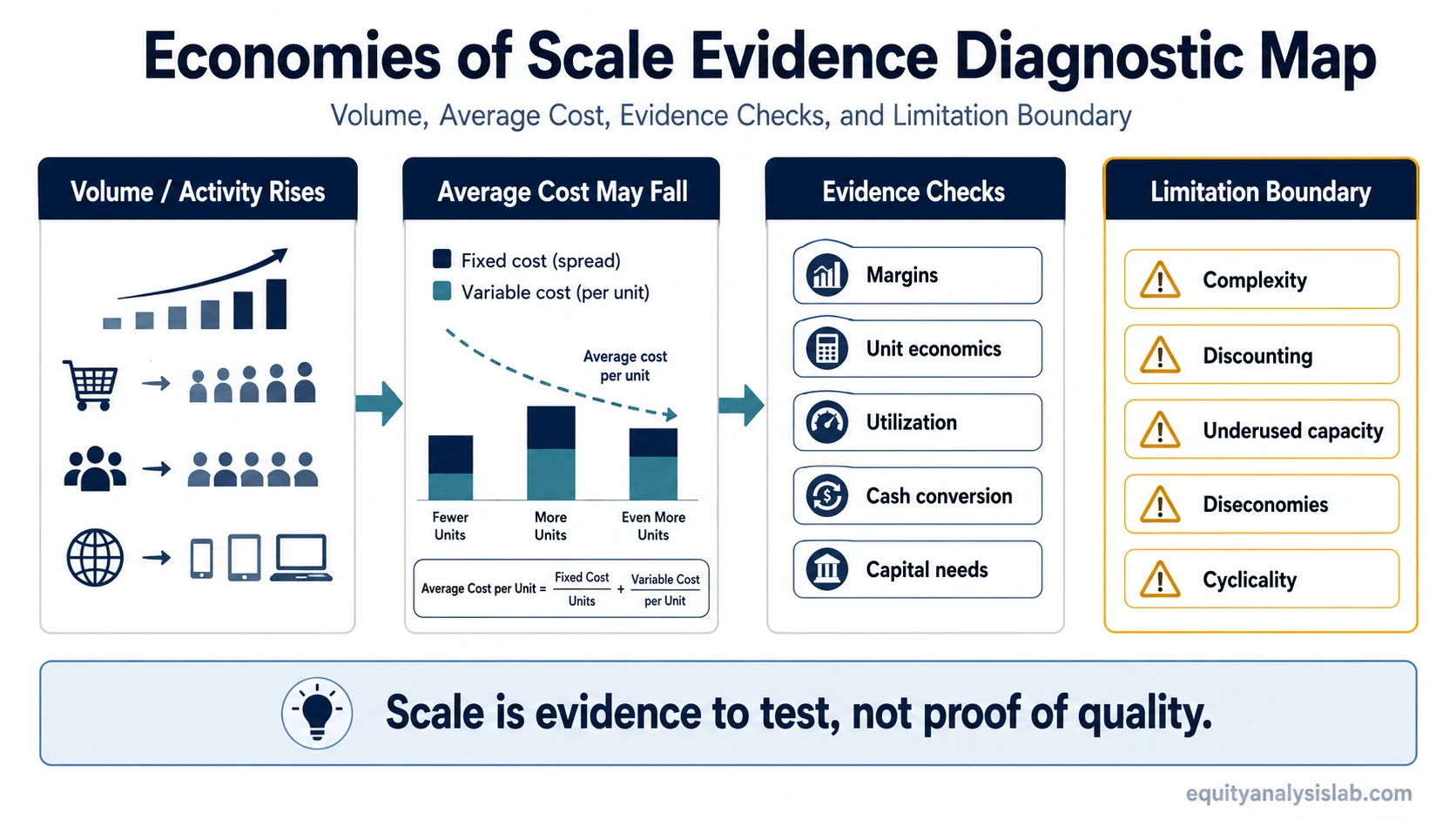

Key Points

- Economies of scale are about lower average unit costs, not size by itself.

- Scale can come from production, purchasing, logistics, technology, financing, or operating systems.

- The useful question is whether scale appears in margins, unit economics, utilization, cash conversion, or durable cost advantage.

- Diseconomies of scale can offset the benefit when complexity, underused capacity, bureaucracy, or price competition rises.

- Economies of scale do not automatically prove moat, quality, valuation upside, safety, or investment attractiveness.

What Economies of Scale Mean

Economies of scale occur when higher activity allows a company to spread costs across a larger base or negotiate better input terms. A factory may spread fixed equipment costs across more units. A distributor may move more volume through the same warehouse network. A software company may serve more users without increasing every infrastructure, engineering, or support cost at the same rate.

A simple way to express the mechanism is: average cost per unit falls when total cost grows more slowly than output. This does not require every cost to fall. Some costs may rise, but the overall cost per unit can decline if the business gains enough efficiency from scale.

Fixed-cost spreading is the most familiar version. If a business has rent, equipment, salaried teams, technology infrastructure, or logistics capacity already in place, higher volume can reduce the share of those costs assigned to each unit. Other sources of scale can include bulk purchasing, better supplier terms, specialized labor, automated processes, lower distribution cost per order, or more efficient financing.

How Economies of Scale Show Up in a Business Model

Scale is more useful when it can be observed in business evidence, not just described in management language. A company may grow revenue quickly and still fail to create economies of scale if support costs, marketing costs, capital spending, inventory needs, discounting, or operating complexity rise at the same pace.

| Scale evidence check | What to look for | What can weaken the signal |

|---|---|---|

| Gross margin trend | Improving gross margin as volume rises can suggest purchasing, production, or delivery efficiency. | Margin can improve for reasons unrelated to scale, such as pricing, mix shift, input-cost timing, or accounting effects. |

| Operating margin trend | Operating expenses growing more slowly than revenue can show fixed-cost leverage across the organization. | Temporary cost cuts, underinvestment, or deferred spending can make margin expansion look stronger than it is. |

| Unit economics | Revenue, contribution profit, or service cost per unit, order, customer, or transaction can show whether scale improves the basic economics of activity. | Rising acquisition costs, churn, returns, support costs, or fulfillment costs can absorb the apparent benefit. |

| Capacity utilization | Higher use of existing factories, warehouses, software infrastructure, or distribution assets can reduce average cost. | Underused new capacity can raise cost per unit until demand catches up. |

| Cash conversion | Scale is stronger when lower unit costs translate into cash generation rather than only accounting profit. | Inventory buildup, receivables pressure, working-capital strain, or heavy reinvestment can weaken the cash benefit. |

| Capital needs | Scale is cleaner when the business can grow without constantly adding expensive assets at the same rate. | A higher capital-intensity profile can absorb cost benefits through depreciation, maintenance, financing, or replacement needs. |

| Customer and demand mix | Broad demand can support repeatable scale economics across customers, products, or regions. | Customer concentration, price concessions, or cyclical demand can make scale less durable. |

The strongest scale case usually combines several signals. Lower unit cost is more convincing when margin structure, operating efficiency, utilization, and cash conversion point in the same direction.

Internal vs External Economies of Scale

Economies of scale can be internal or external. Internal economies of scale come from advantages inside one company. Examples include better purchasing terms, more efficient production, stronger logistics density, shared technology infrastructure, lower per-unit management cost, or financing advantages that come from size and operating stability.

External economies of scale come from the surrounding industry, supplier base, infrastructure, labor pool, or ecosystem. A company may benefit because a region has specialized suppliers, trained workers, logistics density, or common infrastructure that lowers costs for many firms in the same industry.

| Type | Where the advantage comes from | Business-model implication |

|---|---|---|

| Internal economies of scale | The company’s own operations, purchasing, production, systems, financing, or management structure. | Can create company-specific cost advantage if the efficiency is durable and not competed away. |

| External economies of scale | The industry, supplier network, labor pool, infrastructure, or regional ecosystem around the company. | Can lower costs for multiple firms, which may reduce how unique the advantage is for any single company. |

Example of Economies of Scale

Consider a generic distributor that already has warehouses, routing software, purchasing systems, and salaried operating teams in place. If order volume rises and the existing network handles more shipments without a similar increase in fixed costs, the cost assigned to each order may decline. Better warehouse utilization, fuller delivery routes, and larger supplier orders can all support the same scale effect.

The same example has a boundary. If the distributor must add underused warehouses, offer deeper price discounts, hire support teams faster than revenue grows, or carry more inventory, the apparent scale benefit may not improve business quality. The scale claim becomes more credible only when lower average cost also appears in margins, unit economics, and cash conversion.

When Economies of Scale Can Be Overstated

Economies of scale can be overstated when size adds complexity faster than efficiency. Larger organizations may face slower decision-making, duplicated management layers, coordination costs, weaker accountability, or systems that become harder to change. These pressures are often called diseconomies of scale.

Main limitation: Scale is not the same as durable advantage. A company can be large, high-volume, or fast-growing and still fail to convert that scale into lasting unit-cost advantage.

Several conditions can weaken the interpretation. Capacity may be added before demand is ready. Competitors may force price cuts that pass cost savings to customers. A supplier, customer, or platform partner may capture part of the economics. Cyclical demand can make a scaled cost base look efficient near peak volumes and fragile when volumes fall.

Scale also needs to be separated from investment attractiveness. Economies of scale can support a stronger business model, but they do not by themselves determine valuation, risk, expected return, or whether a stock is attractive.

Economies of Scale vs Related Business Model Concepts

Economies of scale often overlap with nearby business-model ideas, but the concepts are not interchangeable. The distinction matters because each concept points to a different kind of evidence.

| Concept | Core question | How it differs from economies of scale |

|---|---|---|

| Capital intensity | How much capital or asset investment is required to operate and grow? | Economies of scale focus on lower average cost as volume rises; capital intensity focuses on how much asset base is required to support that growth. |

| Asset-light business model | How much of the operating model depends on owned assets versus external capacity? | An asset-light business model may scale with fewer owned assets, but it does not automatically create lower unit costs or durable cost advantage. |

| Economies of scope | Can shared capabilities support multiple products, services, customers, or markets? | Economies of scale come from more volume in an activity; shared capabilities across products or markets point to scope rather than volume alone. |

| Operating leverage | Do profits become more sensitive to revenue once fixed costs are covered? | Operating leverage describes profit sensitivity to revenue changes; economies of scale describe lower average cost as activity expands. |

| Unit economics | What does each customer, order, transaction, or unit contribute economically? | Unit economics can show whether scale is actually improving the economics of each activity, but the concept is broader than scale advantage alone. |

| Network effects | Does the product or platform become more valuable as more participants join? | Network effects are about value feedback loops. They may coexist with scale, but they are not the same as lower average cost. |

FAQ

Are economies of scale always good for investors?

No. Scale can improve a business model, but it can also be offset by complexity, price competition, capital needs, weak cash conversion, customer concentration, or cyclical demand.

What is the difference between internal and external economies of scale?

Internal economies of scale come from efficiencies inside one company. External economies of scale come from industry, infrastructure, supplier, labor, or ecosystem advantages that may benefit several companies.

Do economies of scale create a moat?

They can support a moat when the cost advantage is durable, difficult to copy, and not passed away through price competition. Scale alone does not prove that a moat exists.