An asset light business model is a company structure that relies less on owned physical assets and more on partners, leases, platforms, software, intellectual property, or third-party infrastructure to deliver its product or service. For investors, the label matters only when it changes observable capital needs, margins, cash conversion, unit economics, and control risk.

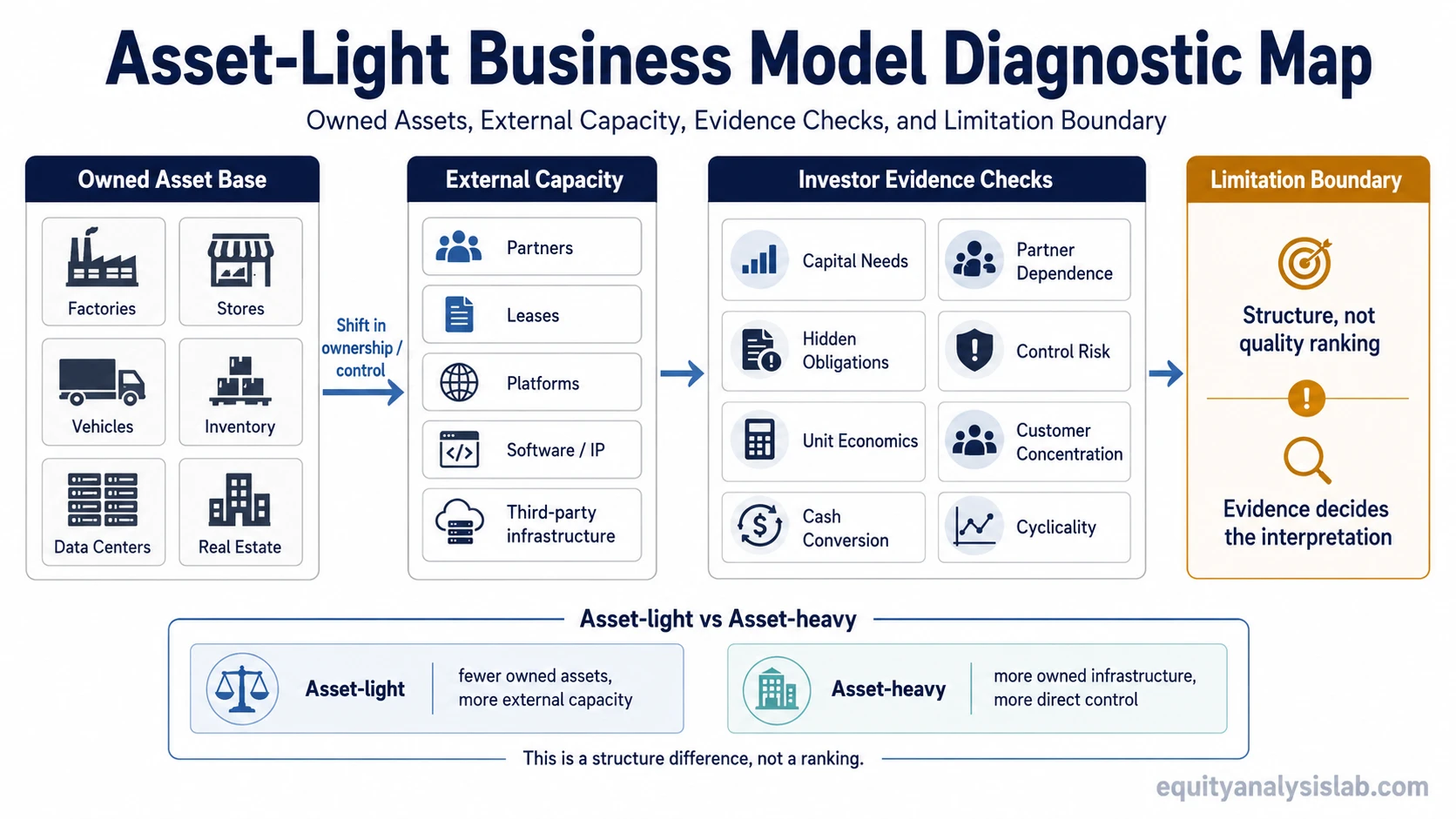

Definition: An asset-light business model reduces the amount of owned assets required to operate the business. Instead of owning most factories, stores, inventory, data centers, vehicles, or real estate directly, the company uses external capacity, contracted partners, licensed technology, shared infrastructure, or intangible assets to support revenue generation.

Key Points

- Asset-light does not mean asset-free. The company may still depend on assets, but many of them sit outside direct ownership.

- The model can reduce upfront capital needs, but it may increase dependence on partners, vendors, platforms, or contract terms.

- Investor analysis should test whether the structure improves economics, not just whether the company owns fewer assets.

- The strongest evidence usually comes from margins, reinvestment needs, cash conversion, unit economics, and control risks.

What Is an Asset Light Business Model?

An asset-light business model describes how a company delivers value while owning relatively fewer hard assets than a more asset-heavy operator in the same or a nearby industry. The structure is common in marketplace, franchise, licensing, software, management-contract, and platform-style models, but it can appear in many sectors.

The concept is a business model feature, not a complete judgment about business quality. A company can be asset-light and still have weak margins, fragile suppliers, high customer churn, poor cash conversion, or limited pricing power. Another company can be asset-heavy and still have strong competitive advantages if its assets create scale, reliability, or barriers to entry.

The useful question is not whether the business sounds light. The useful question is whether the lower owned-asset base changes the economics that investors can observe.

How an Asset Light Business Model Works

An asset-light structure usually works by moving part of the operating asset base outside direct ownership. A company may lease facilities instead of owning them, use contract manufacturers instead of building factories, rely on franchisees instead of operating every location, or use cloud infrastructure instead of owned data centers.

This often reduces upfront capital intensity, because the company does not need to fund every asset required by the operating system. Capital that would have gone into property, plants, inventory, or equipment may instead support product development, customer acquisition, technology, distribution relationships, or brand investment.

The cost structure can also change. Some costs that would have been fixed under direct ownership may become variable or contract-based. That can make the business more flexible during slower periods, but it can also transfer margin power to suppliers, franchisees, landlords, infrastructure vendors, or other partners.

Asset-light models often concentrate management attention on the parts of the business that are intended to create differentiation, such as software, brand, data, distribution, customer relationships, intellectual property, or coordination across a network. The risk is that the company may depend on external parties for execution quality that customers still associate with the brand. The comparison is most useful against peers in the same sector, not against every company generally.

Asset Light vs Asset Heavy Business Models

The asset-light and asset-heavy distinction is mainly about who owns and funds the operating asset base. It is not a ranking system. Each structure can create strengths or weaknesses depending on sector economics, demand stability, financing conditions, and execution quality.

| Area | Asset-light model | Asset-heavy model |

|---|---|---|

| Owned assets | Relies more on partners, leases, platforms, software, IP, or third-party infrastructure. | Owns more of the physical infrastructure, facilities, equipment, inventory, or operating base. |

| Capital needs | May require less upfront capital to expand revenue capacity. | Often requires larger reinvestment before capacity can grow. |

| Cost structure | May shift some fixed costs toward variable or contracted costs. | May carry higher fixed costs, but may also capture more economics if utilization is high. |

| Control | May have less direct control over service quality, timing, capacity, or partner behavior. | May have more direct control, but also more operational complexity and asset risk. |

| Investor risk | The label can overstate quality if unit economics, partner dependence, or customer concentration are weak. | The asset base can look burdensome, but may support scale, reliability, or entry barriers when well used. |

What Investors Should Check Before Trusting the Asset-Light Label

An asset-light label is only useful when it is connected to evidence. The table below separates the narrative from the checks that usually matter in company analysis.

| Evidence check | What to examine | Why it matters |

|---|---|---|

| Revenue driver | Whether revenue comes from transaction fees, subscriptions, licensing, commissions, management fees, product sales, or service contracts. | The revenue model determines how much of the asset-light structure can convert into durable economics. |

| Margin driver | Whether margins come from pricing power, software-like delivery, partner leverage, cost pass-through, or temporary underinvestment. | High margins are stronger when they come from durable economics rather than deferred costs or partner pressure. |

| Capital needs | Capital expenditure, working capital needs, lease commitments, software development costs, acquisition spending, and outsourced operating costs that may not appear as owned fixed assets. | Some businesses look asset-light because they own fewer physical assets, while still carrying meaningful contractual, technology, working-capital, or partner-related investment needs. |

| Operating leverage | How profit changes when revenue rises or falls. | A variable cost base can reduce downside pressure, but it may also limit upside if partners capture much of the incremental economics. |

| Unit economics | Contribution margin, customer acquisition cost, retention, payback period, fulfillment cost, and support cost. | Scale is less valuable when each added customer or transaction has weak economics. |

| Customer concentration | Dependence on a small group of customers, channels, marketplaces, franchisees, or enterprise accounts. | Low asset ownership does not remove revenue concentration risk. |

| Cyclicality | How demand behaves in downturns, inventory cycles, travel cycles, advertising cycles, or credit tightening periods. | A flexible asset base does not make revenue immune to cyclical demand. |

| Cash conversion | Operating cash flow, free cash flow, receivables, payables, deferred revenue, and working-capital timing. | Reported earnings are less informative if cash conversion is weak or heavily timing-dependent. |

| Partner dependence | Reliance on suppliers, infrastructure vendors, franchisees, contractors, marketplaces, or distribution partners. | External capacity can reduce ownership needs while adding negotiation, quality, availability, and pricing risk. |

| Control and quality risk | Whether the company can maintain customer experience, delivery standards, compliance, and brand reputation through third parties. | An asset-light system can weaken if the company controls the customer promise but not the full operating process. |

Advantages and Limits of Asset-Light Models

The main advantage of an asset-light model is that growth may require less owned physical infrastructure. If the economics hold, the company may expand revenue with lower reinvestment needs than an asset-heavy operator. This can support better cash generation, faster geographic expansion, and more flexible capacity management.

Asset-light structures can also support economies of scale when added volume spreads technology, brand, coordination, or platform costs across a larger revenue base. The limitation is that economies of scale only matter if incremental revenue keeps attractive economics after partner costs, support costs, customer acquisition costs, and quality-control expenses are included.

The same structure can create risks. A company that depends on outside partners may have less control over cost, availability, service quality, compliance, and customer experience. If partners gain bargaining power, the asset-light company may keep the brand relationship but lose part of the margin advantage.

Limitation: Asset-light is not a shortcut for quality. The label can make returns on assets or invested capital look attractive because the denominator is smaller, but the economic question is whether the business can sustain cash generation, pricing power, partner access, and customer retention over time.

For investors, the stronger test is not whether reported asset efficiency looks high, but whether cash generation remains durable after partner costs, customer acquisition, support needs, and reinvestment are included.

Asset-Light Example

A marketplace that connects buyers and sellers without owning the inventory is a simple asset-light example. The marketplace may earn transaction fees while sellers hold inventory, manage fulfillment, or carry some operating costs. That can reduce the marketplace company’s owned asset base, but the investor still has to check take rates, customer acquisition costs, seller concentration, payment risk, service quality, and whether the platform can keep enough value as the network grows.

The same logic can appear in franchise or management-agreement models, where brand systems and operating standards matter even when the company does not own every physical location.

Common Mistakes When Reading Asset-Light Businesses

- Treating asset-light as proof of quality: A lighter asset base can help, but it does not prove demand durability, pricing power, or competitive advantage.

- Ignoring partner dependence: Outsourced assets still matter if suppliers, franchisees, contractors, or infrastructure vendors can raise prices or reduce service quality.

- Confusing ratio optics with economics: A company may show attractive asset-based ratios because it owns fewer assets, not because the business has stronger cash economics.

- Assuming scalability without unit economics: Growth can destroy value if customer acquisition, support, fulfillment, or partner costs rise faster than revenue quality.

- Overlooking concentration and cyclicality: Low asset ownership does not remove exposure to a narrow customer base, one distribution channel, or cyclical demand.

Related Concepts

Asset-light analysis often starts with how much capital the business needs, but it should not stop there. Shared capabilities, brand systems, technology platforms, and distribution relationships can also affect how efficiently the model expands across products or markets.

The connection to shared business capabilities matters when the same platform, brand, data, or operating system supports multiple revenue lines without requiring a separate asset base for each one.

FAQ

What does asset light mean in business?

Asset light means a business relies less on owned physical assets and more on partners, leases, software, intellectual property, platforms, contracts, or third-party infrastructure. It still depends on assets, but many of those assets are not owned directly by the company.

Is an asset-light business model always better?

No. An asset-light model can reduce capital needs, but it can also create partner dependence, quality-control issues, supplier pricing risk, or weak unit economics. The model is useful only when the underlying economics support it.

How is asset light different from asset heavy?

An asset-light model owns fewer operating assets and relies more on external capacity or intangible assets. An asset-heavy model owns more infrastructure, equipment, inventory, facilities, or real estate. Neither structure is automatically superior.

What should investors check in an asset-light company?

Investors should check capital needs, margins, cash conversion, unit economics, customer concentration, cyclicality, partner dependence, and control risk. The label matters less than whether the structure produces durable economic evidence.