Bank stocks should be analyzed as balance-sheet-driven financial businesses, not as ordinary industrial companies. The investor has to connect funding quality, loan mix, credit losses, capital strength, profitability, and valuation before judging whether a bank looks cheap, durable, or risky.

A bank is built around financial assets and financial liabilities. Deposits, loans, securities, funding costs, provisions, and regulatory capital all affect the value of the equity. That makes bank-stock analysis different from analyzing a software company, retailer, manufacturer, or asset-light service business.

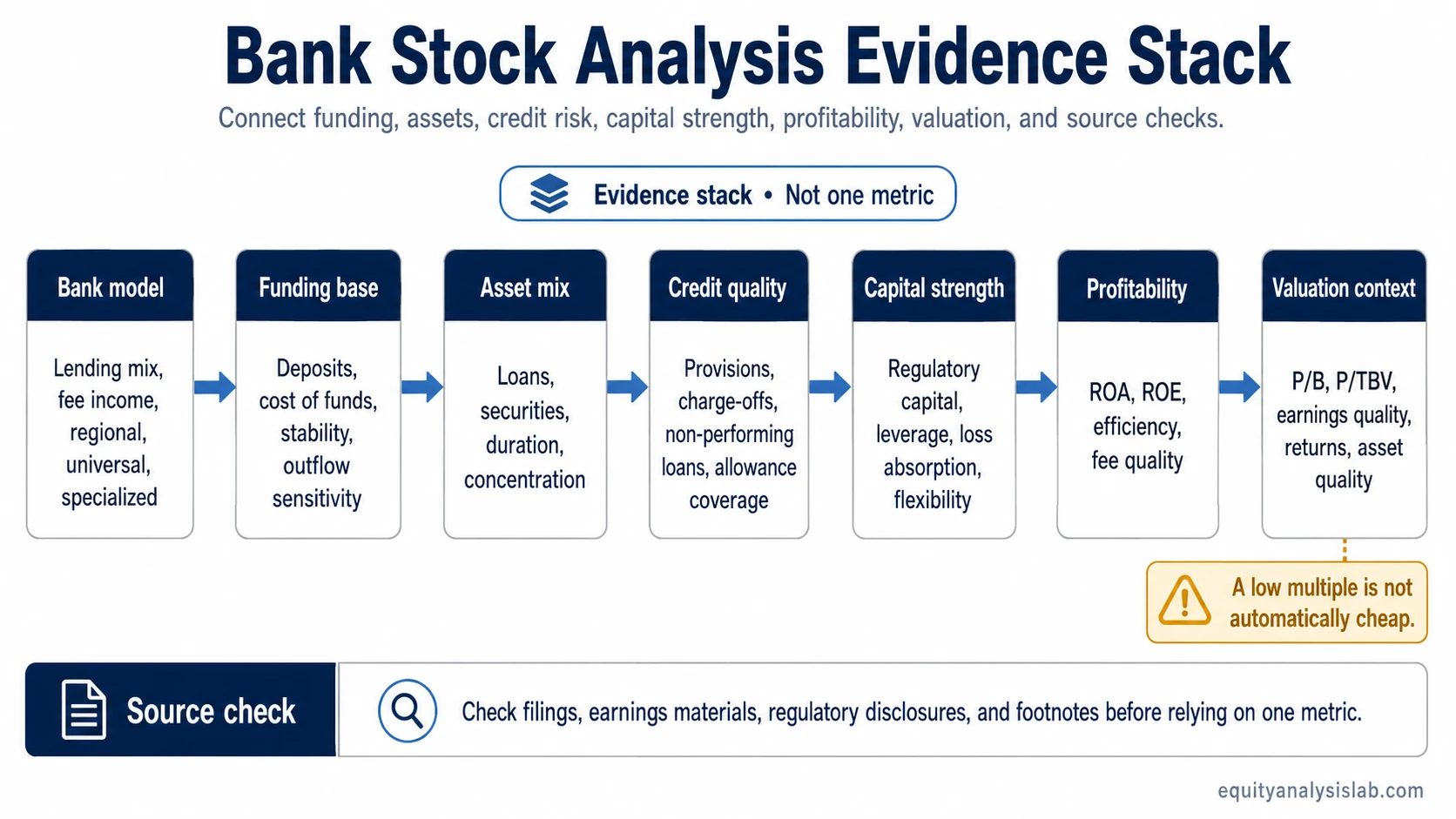

Bank-stock analysis in five checks

- Start with the bank’s business model: commercial lending, investment banking, regional banking, universal banking, or a specialized lending niche.

- Check funding quality before treating earnings as durable. A low-cost, stable deposit base can be more important than a single-quarter margin improvement.

- Read credit quality together with loan mix. Earnings can look strong before provisions, charge-offs, or non-performing loans reveal stress.

- Judge valuation through profitability and risk. A low price-to-book multiple is not automatically cheap if returns, capital confidence, or asset quality are weak.

- Use bank metrics as an evidence trail, not as standalone verdicts.

Why banks need a different analysis framework

Most companies sell products or services and then report revenue, margins, cash flow, assets, and liabilities around that operating model. Banks are different because the balance sheet is the operating engine. Loans and securities produce income, deposits and other funding create cost, and capital rules limit how much risk the bank can carry.

That is why generic ratio analysis can mislead. A bank with a low valuation multiple may be genuinely undervalued, but it may also be priced for weaker credit quality, lower returns, fragile deposits, or capital pressure. A bank with high reported earnings may still deserve caution if those earnings depend on riskier loan growth, temporary rate benefits, or under-recognized credit losses.

The useful starting question is not “Which bank stock is best?” The useful starting question is: what evidence explains the bank’s funding, assets, credit risk, capital position, profitability, and valuation together?

The bank-stock evidence buckets

A disciplined bank-stock review works best as an evidence trail. Each bucket answers a different question, and the conclusion becomes stronger only when the buckets point in the same direction.

| Evidence bucket | What to examine | Why it matters |

|---|---|---|

| Bank business model | Commercial banking, investment banking, universal banking, regional banking, specialized lending, wealth or fee businesses. | Different bank types deserve different metric emphasis. A trading-heavy bank, a deposit-led lender, and a specialized lender do not carry the same risk profile. |

| Funding base | Deposit stability, cost of funds, wholesale funding reliance, customer concentration, and sensitivity to deposit outflows. | Funding quality affects liquidity, net interest margin, and resilience during stress. |

| Asset mix | Loan categories, securities portfolio, trading assets, credit exposure, duration exposure, and concentration by borrower or sector. | The asset side drives income, but it also carries credit, rate, and mark-to-market risk. |

| Net interest economics | Net interest income, net interest margin, asset yields, deposit costs, and rate sensitivity. | Many banks earn through spread economics, but a better spread is not enough if funding or credit quality is deteriorating. |

| Credit quality | Non-performing loans, charge-offs, provisions, allowance coverage, loan growth quality, and borrower stress. | Credit quality can turn reported earnings into a lower-quality signal if losses are rising or under-reserved. |

| Capital strength | Regulatory capital, leverage, loss absorption, balance-sheet growth capacity, and capital return flexibility. | Capital affects how much risk the bank can carry and how much room it has to grow, absorb losses, or return cash. |

| Profitability | ROA, ROE, ROTCE where appropriate, efficiency ratio, fee income quality, and expense discipline. | Profitability explains whether the bank can earn attractive returns on its capital base. |

| Valuation | P/B, P/TBV, P/E, earnings quality, return profile, credit risk, and capital confidence. | Bank valuation is only meaningful when the multiple is connected to returns, asset quality, funding stability, and capital strength. |

| Regulation and cycle | Capital rules, credit cycle, loan demand, deposit competition, rate sensitivity, and macro exposure. | Banks are regulated cyclical businesses, so the same metric can mean different things at different points in the cycle. |

Bank metrics and what can distort them

Bank metrics are useful when they are interpreted as connected evidence. They become dangerous when a single number is treated as the answer.

| Metric | What it usually helps evaluate | What can distort the reading |

|---|---|---|

| Net interest margin | Spread economics between earning assets and funding costs. | Margin can improve while deposit costs, credit risk, or securities pressure also rise. |

| Net interest income | Dollar value of interest income after funding costs. | Growth can reflect balance-sheet expansion, rate effects, or riskier lending rather than durable quality. |

| Return on assets | How efficiently the bank earns on its asset base. | Asset mix, leverage, provisions, and unusual gains can change interpretation. |

| Return on equity | How effectively the bank earns on shareholder capital. | Higher leverage can lift ROE while also increasing balance-sheet risk. |

| Efficiency ratio | Cost discipline relative to revenue. | A better ratio may come from temporary revenue strength, not only better cost structure. |

| Provisions and charge-offs | Current and expected credit-loss pressure. | Provision timing can make earnings look better or worse before losses fully appear. |

| P/B and P/TBV | Market value relative to accounting book value or tangible book value. | A discount can signal opportunity, but it can also reflect weak returns, asset-quality doubts, or capital concerns. |

| Capital ratios | Loss absorption, regulatory room, and balance-sheet flexibility. | Capital strength depends on asset risk, earnings power, and regulatory context, not the ratio alone. |

A practical reading sequence is: first identify the bank type, then inspect funding and assets, then test credit quality and capital, then decide whether profitability and valuation tell the same story.

A simple two-bank valuation scenario

Imagine two banks trade at similar price-to-book levels. The first has a stable deposit base, conservative loan growth, improving credit quality, adequate capital, and returns that appear repeatable. The second has faster loan growth, rising funding pressure, weaker credit trends, and returns that depend heavily on a favorable rate backdrop.

The same book-value multiple does not mean the same thing in both cases. The first bank may deserve a different interpretation because the valuation is supported by funding quality, credit discipline, and profitability durability. The second may look statistically cheap while still carrying more risk. The useful comparison is not the multiple alone, but the evidence behind the multiple.

Beginner mistake map

Most bank-stock mistakes come from reading one familiar metric in isolation. The safer approach is to connect each metric to the part of the bank model it actually measures.

| Mistake | Why it is risky | Safer treatment |

|---|---|---|

| Treating low P/B as automatically cheap | A weak bank may trade below book because ROE, credit quality, or capital confidence is poor. | Interpret book-value multiples through profitability, asset quality, and capital strength. |

| Applying generic DCF logic | Banks use deposits and financial liabilities differently from industrial companies. | Use bank-specific valuation context instead of forcing an industrial-company cash-flow model. |

| Looking at NIM alone | NIM can improve while credit risk or funding risk worsens. | Pair NIM with deposit cost, loan mix, provisions, credit losses, and capital. |

| Ignoring loan mix | A bank can grow loans while also taking on more concentrated or lower-quality risk. | Separate loan growth from loan quality, borrower mix, and sector concentration. |

| Assuming clean earnings mean low risk | Credit losses may appear with a lag, especially after rapid lending growth or economic stress. | Read earnings with provisions, charge-offs, allowance coverage, and non-performing loans. |

| Ignoring rate sensitivity | Rate changes can affect asset yields, deposit costs, securities values, and loan demand. | Check whether the bank benefits from rate conditions or is only temporarily helped by them. |

What bank-stock analysis cannot prove

Bank-stock analysis can improve the quality of the question, but it cannot remove uncertainty. Credit cycles change, deposits can become more expensive, asset values can move, regulation can tighten, and management decisions can change the risk profile. A clean-looking bank analysis is still a probability-based judgment, not proof that a stock is safe or undervalued.

The direct-source check matters. Before relying on a bank-stock conclusion, investors should read the bank’s filings, earnings materials, regulatory disclosures where relevant, capital discussion, credit tables, deposit data, and management commentary. Secondary summaries can help with orientation, but the source documents explain the actual balance-sheet exposure.

Where to go deeper after bank-stock analysis

Bank-stock analysis should point readers toward deeper concepts rather than trying to explain every financial statement, valuation, and profitability topic in one broad overview.

| Question | Deeper concept | Why it helps |

|---|---|---|

| How should a bank balance sheet be read? | balance sheet | The balance sheet is the core operating engine for a bank, so assets, liabilities, and equity need careful interpretation. |

| How does book-value valuation work? | price-to-book ratio | P/B becomes more useful when it is connected to ROE, credit quality, and capital confidence. |

| Does the bank earn enough on shareholder capital? | return on equity | ROE helps explain whether book value is being used productively, but it still needs risk and leverage context. |

| Does the bank have a durable funding or customer advantage? | economic moat | A strong deposit franchise, customer relationship base, or cost advantage can support long-term banking quality. |

| Why do banks require so much balance-sheet capacity? | capital-intensive business model | Banks depend on asset-heavy balance sheets and regulated capital, so growth is tied to capital availability and risk control. |

| How should profitability be understood beyond spread metrics? | net margin | Net margin is not a substitute for NIM, but it helps frame broader profitability discipline across business models. |

FAQ

What is the first thing to check when analyzing a bank stock?

Start with the bank’s business model and balance sheet. The investor needs to know how the bank earns money, how it is funded, what assets it owns, what credit risk it carries, and how much capital supports the balance sheet.

Is a low price-to-book ratio always good for bank stocks?

No. A low price-to-book ratio can signal undervaluation, but it can also reflect weak profitability, poor credit quality, funding concerns, or low confidence in the bank’s capital position.

Which bank metrics matter most?

Common inputs include NIM, NII, ROE, ROA, provisions, charge-offs, capital ratios, P/B, and P/TBV. The strongest analysis connects these metrics instead of relying on one number.

Should bank stocks be analyzed with the same DCF approach as other companies?

Usually not as the main beginner framework. Banks have financial assets, deposits, regulatory capital, and credit risk dynamics that make generic industrial-company DCF logic less straightforward. Bank valuation usually needs book value, returns, asset quality, and capital context.