A high conviction portfolio concentrates more capital in a smaller set of investment ideas that an investor believes they understand well. The central issue is not whether conviction is automatically good or bad, but how that conviction changes portfolio weights, overlap, diversification, risk capacity, and review discipline.

High conviction investing becomes a portfolio construction question once the strongest ideas receive larger weights. A position can look attractive in isolation, but its portfolio effect depends on what else is owned, which risks are repeated, how long the thesis needs to work, and what would trigger a reassessment if the evidence changes.

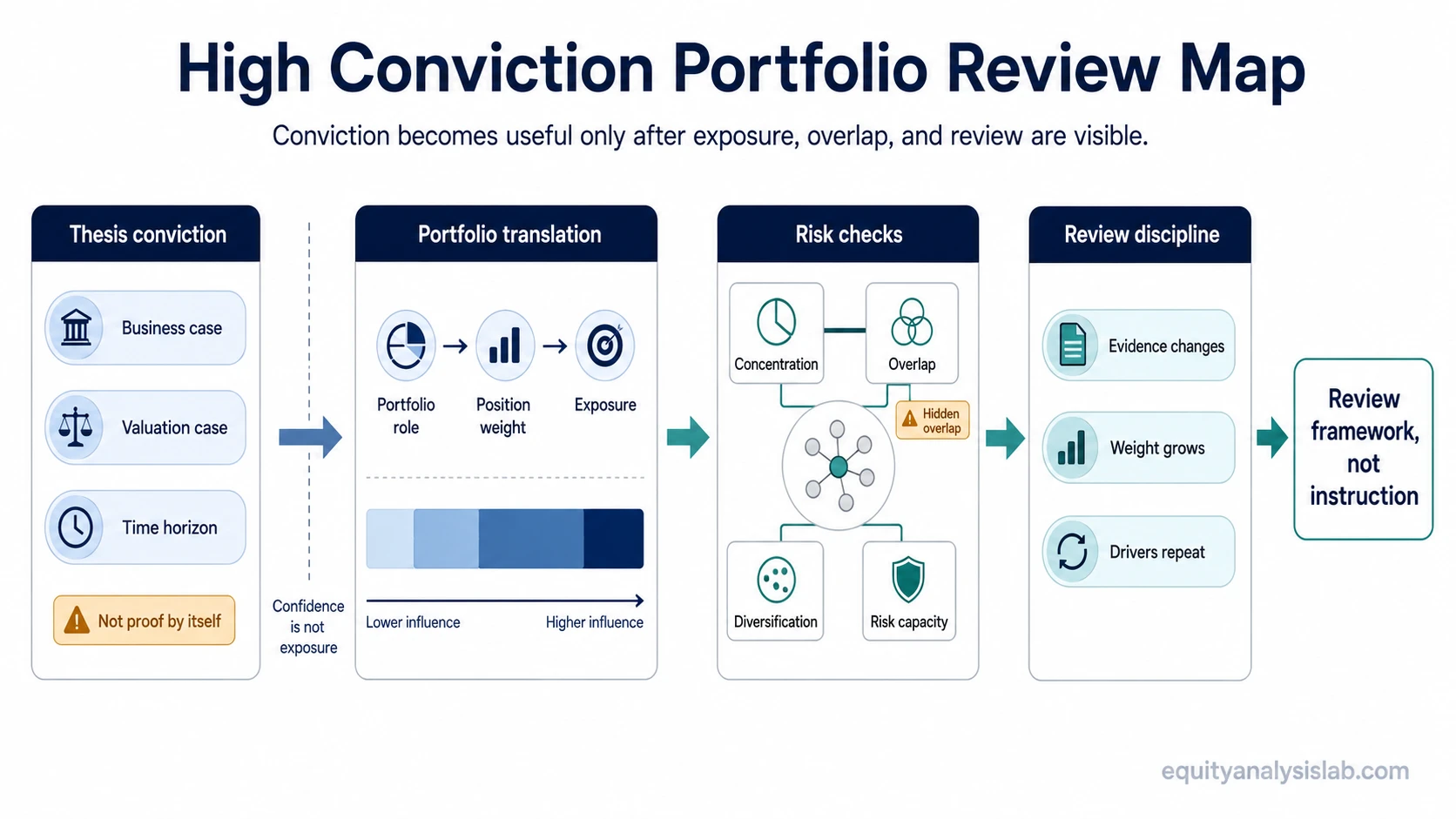

Definition: A high conviction portfolio is a portfolio built around a smaller group of higher-confidence investment ideas, usually with larger position weights than a broadly diversified or rules-based portfolio. It is not a promise of better returns, a stock-pick list, or proof that the investor is right.

Key Points

- A high conviction portfolio turns research confidence into measurable exposure through position weights.

- Concentration is not only about the number of holdings. It also depends on top-weight size, shared drivers, sector exposure, and thesis overlap.

- Diversification can be weak even when the holding count looks reasonable if several large positions depend on the same outcome.

- Review discipline matters because confidence can become inertia when the original thesis weakens.

- Large positions need clearer evidence, clearer risk boundaries, and clearer review rules than small exploratory holdings.

What a High Conviction Portfolio Is

A high conviction portfolio starts from the idea that not every investment deserves the same weight. Some holdings may receive larger allocations because the investor believes the business quality, valuation case, expected role, or thesis durability is stronger than the rest of the opportunity set.

That does not mean every strong idea should become a large position. Conviction has to pass through portfolio construction. The same idea can be reasonable as a small satellite position, too large as a core holding, or unsuitable if it duplicates risks that already dominate the portfolio.

The key distinction is between confidence in a thesis and exposure to a thesis. Confidence is qualitative. Exposure is measurable. A high conviction portfolio needs both sides to be visible.

How Conviction Changes Portfolio Exposure

Conviction changes exposure through weight, concentration, and dependency. A 3% position and a 15% position may be based on the same research view, but they do not create the same portfolio risk. The larger position has more influence over total results and therefore needs a stronger role, clearer evidence, and a more explicit reassessment rule.

Other holdings also change the meaning of a high-conviction idea. If several positions depend on the same earnings cycle, interest-rate environment, commodity price, or sector trend, the portfolio may be more concentrated than the holding count suggests.

Portfolio sequence: thesis conviction leads to portfolio role, portfolio role informs position weight, position weight creates concentration, concentration requires an overlap check, overlap affects diversification, and the whole structure needs a review rule before the thesis becomes stale.

Position Sizing, Concentration, and Overlap

Position sizing is where high conviction becomes visible, while concentration is where that visibility becomes portfolio-level risk. A larger weight says that the idea matters more to the portfolio outcome. That can be reasonable when the thesis is well defined, the role is clear, and the downside effect is understood. It becomes fragile when size increases mainly because the idea feels more exciting.

Higher conviction should not remove the need for risk capacity. A portfolio can hold a strong idea at a size that is still too large for the investor’s financial situation, time horizon, or ability to tolerate a wrong thesis.

| Review area | Question to answer | Why it matters |

|---|---|---|

| Thesis conviction | What makes this holding different from a normal allocation? | Separates researched conviction from preference, recency bias, or excitement. |

| Portfolio role | What job does the position perform? | Prevents every attractive idea from competing for the same role. |

| Position weight | How much portfolio exposure does the idea create? | Turns conviction into measurable risk rather than a vague opinion. |

| Overlap | Do several holdings depend on the same driver? | Reveals false diversification when different names share the same risk. |

| Diversification | What risk remains if the thesis is wrong? | Keeps concentration from becoming hidden fragility. |

| Time horizon | How long does the thesis need to work? | Connects position review to the investment case instead of short-term noise. |

| Review rule | What would weaken, resize, or remove the position? | Prevents conviction from turning into inertia. |

Diversification Is Not Just the Number of Holdings

A portfolio with fewer holdings is usually easier to recognize as concentrated. The harder case is a portfolio that appears diversified because it owns many securities, while the largest positions share the same business driver, valuation assumption, sector exposure, or macro sensitivity.

True diversification depends on what can go wrong at the same time. Fifteen holdings can still behave like a narrow portfolio if the top five positions represent most of the capital and all depend on similar earnings growth, similar interest-rate conditions, or the same market narrative.

Holding count: how many positions the portfolio owns.

Exposure mix: how much capital depends on each idea, sector, factor, or economic driver.

Portfolio diversification: how much the portfolio is protected from one thesis, driver, or assumption being wrong.

This is why a high conviction portfolio should be reviewed against the investor’s investment objectives, not only against a preferred list of names. The objective defines what the portfolio is supposed to accomplish before any single idea receives a larger weight.

Review Rules for a High Conviction Portfolio

Large positions need a review process because they can become difficult to question. The stronger the attachment to the thesis, the easier it is to explain away new evidence that would be treated more critically in a smaller position.

The review rule should match the thesis. A business-quality thesis may require periodic checks on margins, cash flow, competitive position, or balance-sheet risk. A valuation thesis may require a different review if the price rises, the earnings base changes, or the original margin of safety disappears.

The process should also match the investor’s time horizon. A long-term thesis should not be judged by every short-term price move, but a long-term label should not be used to ignore evidence that the thesis itself has changed.

| Review trigger | What it asks | Possible interpretation |

|---|---|---|

| Thesis evidence changes | Is the original reason for the position still intact? | The position may still fit, but conviction needs to be re-earned. |

| Weight grows after price movement | Is the position now larger than the intended risk budget? | Portfolio exposure may have changed even if the thesis did not. |

| Several holdings move together | Are different positions depending on the same driver? | The portfolio may be less diversified than it appears. |

| Investor situation changes | Has risk capacity or required liquidity changed? | A previously acceptable concentration level may no longer fit. |

When High Conviction Becomes a Portfolio Risk

High conviction becomes a portfolio risk when position weights dominate the portfolio, holdings overlap around the same driver, or the review process cannot separate thesis strength from concentration risk. A concentrated portfolio can be disciplined, but only if each large weight has a clear role, a clear reason to exist, and a clear condition that would weaken the case.

Failure condition: conviction becomes fragile when the investor can explain why a position is attractive but cannot explain how much damage a wrong thesis could cause, what evidence would change the view, or whether several holdings are exposed to the same risk at once.

A common mistake is increasing size because confidence feels stronger, without better evidence or a clearer risk boundary. Larger weights require more discipline, not less. The question is not only “Do I believe this?” It is also “What happens to the full portfolio if this belief is wrong?”

This is where risk tolerance and risk capacity should be separated. Risk tolerance describes how much volatility an investor believes they can emotionally handle. Risk capacity describes how much risk the investor can financially afford to take. A high conviction portfolio can fail if either boundary is ignored.

High Conviction Portfolio Checklist

A high conviction portfolio review should make the exposure visible before judging the idea. The checklist below keeps the work focused on portfolio construction rather than confidence alone.

| Checklist item | Pass condition | Risk if unclear |

|---|---|---|

| Thesis | The reason for the position is specific and testable. | The holding may be driven by preference rather than analysis. |

| Role | The position has a defined job in the portfolio. | Several holdings may compete for the same purpose. |

| Weight | The allocation fits the investor’s risk budget. | One thesis may dominate total portfolio behavior. |

| Overlap | Shared drivers across large holdings are identified. | The portfolio may be concentrated without looking concentrated. |

| Diversification | The portfolio can absorb one major thesis being wrong. | Concentration may turn into hidden fragility. |

| Review rule | The investor knows what would trigger a reassessment. | Conviction may become inertia. |

Investors building a portfolio from the ground up can compare this framework with a broader stock portfolio construction process. High conviction is one possible structure, not the default answer for every investor.

High Conviction Portfolio vs Rules-Based Portfolio Approaches

A high conviction portfolio relies on judgment about which ideas deserve larger weights. Rules-based approaches, such as a lazy portfolio or a three-fund portfolio, usually start from predefined allocation rules rather than investor-specific conviction in a small group of holdings.

Neither structure is automatically superior. The useful comparison is process discipline: a rules-based portfolio needs allocation rules and rebalancing discipline, while a high conviction portfolio needs thesis discipline, sizing discipline, overlap checks, and review rules.

FAQ

Is a high conviction portfolio the same as a concentrated portfolio?

Not always. A high conviction portfolio often is concentrated, but concentration describes exposure, while high conviction describes the reasoning behind larger weights. A portfolio can be concentrated without strong research discipline, and a high conviction process can still include diversification rules.

How many holdings does a high conviction portfolio have?

There is no fixed number. The more important question is how much capital sits in the largest positions, how much those positions overlap, and whether the portfolio can handle one major thesis being wrong.

What is the main risk of a high conviction portfolio?

The main risk is that confidence in a few ideas turns into excessive exposure. That risk increases when large positions share the same driver, when review rules are vague, or when the investor cannot separate thesis conviction from portfolio damage if the thesis fails.