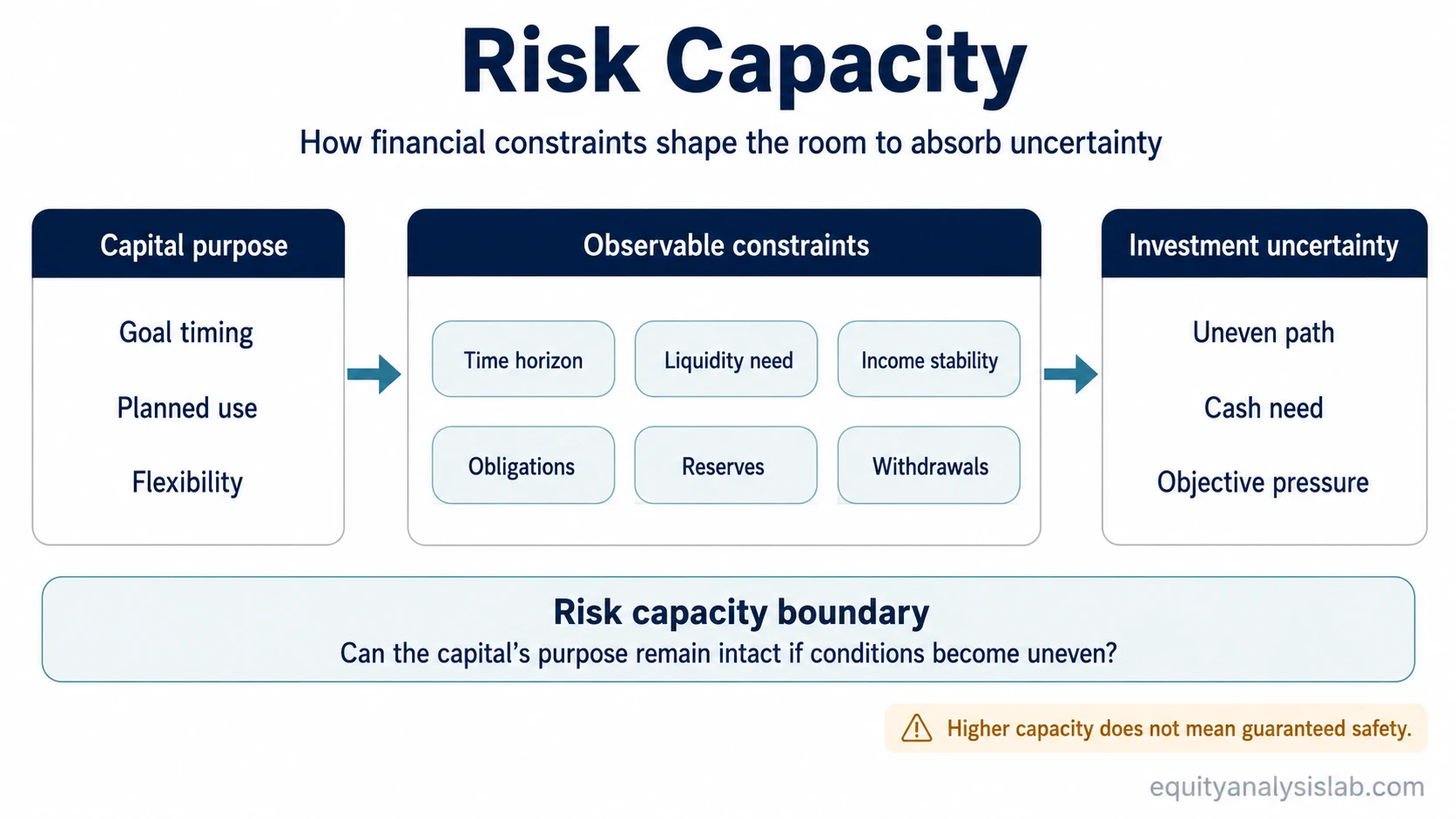

Risk capacity is the amount of investment risk an investor’s financial situation can take before the purpose of the capital comes under pressure. It is shaped by observable constraints such as time horizon, liquidity need, income stability, obligations, assets, liabilities, planned withdrawals, and goal timing.

Definition: Risk capacity is an investor’s objective ability to take investment risk without putting the capital’s intended purpose at risk. It is not the same as risk tolerance, which describes willingness or comfort with uncertainty.

- Risk capacity is based on financial constraints, not only emotions or confidence.

- The same market volatility can have different consequences for investors with different cash needs.

- Capacity can change when income, obligations, liquidity needs, or goal timing changes.

- Higher capacity does not make an investment safe or predict the outcome.

What Determines Risk Capacity?

Risk capacity depends on how much flexibility the investor has if an investment path becomes uneven. The issue is not only whether the investor dislikes losses. The issue is whether the capital can still serve its purpose if values fluctuate, cash is needed, income changes, or obligations become more demanding.

| Input | How it affects risk capacity |

|---|---|

| Time horizon | A longer evaluation window can give an investor more flexibility. A near-term goal usually lowers capacity because the capital may be needed before uncertainty has time to resolve. |

| Liquidity need | Capital that may be needed soon has less room to withstand large or prolonged drawdowns. |

| Income stability | Stable income can reduce pressure to sell investments during difficult periods. Unstable income can make the same investment path harder to manage financially. |

| Assets and reserves | More liquid reserves may increase flexibility. Concentrated or illiquid assets may reduce the ability to meet unexpected needs. |

| Debt and liabilities | Required payments reduce flexibility because cash must be available regardless of market conditions. |

| Planned withdrawals | Regular withdrawals can lower capacity because selling during weak periods may damage the objective. |

| Dependents and obligations | Family, business, tax, education, or other obligations can make capital needs less flexible. |

| Goal timing | A goal with a fixed date usually has lower capacity than a goal that can be delayed or adjusted. |

Risk Capacity vs Risk Tolerance

Risk capacity and risk tolerance answer different questions. Risk capacity asks what the investor’s financial situation can take. Risk tolerance asks how much uncertainty the investor is emotionally willing to experience.

| Concept | Main question | Based on |

|---|---|---|

| Risk capacity | Can the investor’s situation handle the risk without damaging the objective? | Time horizon, cash needs, income, obligations, assets, liabilities, and withdrawals. |

| Risk tolerance | How comfortable is the investor with uncertainty, volatility, or temporary loss? | Temperament, experience, confidence, emotional response, and behavioral discipline. |

The two can point in different directions. An investor may feel comfortable with volatility but have low capacity because the capital is needed soon. Another investor may have strong financial flexibility but low tolerance because uncertainty creates emotional pressure. A complete investor decision process needs both inputs: capacity as the objective constraint and tolerance as the behavioral constraint.

How Risk Capacity Changes an Investment Plan

Risk capacity changes the interpretation of the same investment uncertainty. A decline, delay, or uneven return path may be manageable for capital with a flexible purpose and long timing window. The same path can be damaging when the money is needed for a fixed obligation, near-term withdrawal, or non-negotiable goal.

This is why risk capacity connects directly to investment objectives. The objective defines what the capital is meant to do. Capacity tests whether the investor’s financial situation leaves enough room for uncertainty while pursuing that purpose.

Important boundary: Risk capacity does not say which investment is suitable, which allocation is correct, or which outcome will occur. It only helps frame whether the investor’s constraints leave enough flexibility before the objective is placed under pressure.

A Short Risk Capacity Example

Two investors may both say they are comfortable with market volatility. One expects to use the capital within a year and has limited cash reserves. The other has a longer time horizon, stable income, and no planned withdrawals from the account. Their emotional comfort may look similar, but their risk capacity is different because the first investor has less room for an unfavorable investment path before the money is needed.

The example is not an allocation recommendation. It shows the difference between willingness and financial flexibility. Capacity is about what the investor’s situation can handle, not how confident the investor feels.

Common Mistakes When Using Risk Capacity

Mistake 1: Treating confidence as capacity. Confidence can rise during calm markets, but it does not remove a near-term cash need, a debt obligation, or an unstable income source.

Mistake 2: Treating capacity as a guarantee. Higher capacity may create more flexibility, but it does not make an investment safe or protect against loss.

Mistake 3: Treating capacity as fixed. Capacity can change after a job loss, new liability, large expense, planned withdrawal, inheritance, liquidity event, or change in goal timing.

Mistake 4: Reducing capacity to a questionnaire score. A questionnaire may organize inputs, but the useful judgment comes from understanding the real constraints behind the answers.

How to Think About Risk Capacity Before Setting Goals

Risk capacity becomes clearer when the investor separates purpose, timing, and constraint. The purpose defines what the capital is meant to achieve. The timing defines when the capital may be needed. The constraints define how much stress the investor can manage along the way.

For investors still organizing those inputs, the process usually begins with how to set investment goals. Goals make capacity easier to interpret because they give the capital a specific purpose and time frame.

Risk capacity also differs from the circle of competence. Capacity is about the ability to handle financial risk. Circle of competence is about whether the investor can understand, evaluate, and monitor the investment with enough evidence.

Related Concepts

Risk tolerance: separates financial ability from emotional willingness.

Investment objectives: define what the capital is meant to accomplish before judging how much risk it can handle.

How to set investment goals: helps organize objective, timing, and constraints when they are not yet clear enough to evaluate capacity.

Circle of competence: separates the ability to handle risk from the ability to understand the investment itself.

FAQ

Is risk capacity the same as risk tolerance?

No. Risk capacity is the objective ability to absorb investment risk. Risk tolerance is the willingness or comfort level an investor has when facing uncertainty.

Is risk capacity a questionnaire score?

No. A questionnaire can help organize inputs, but risk capacity is not the score itself. The important part is the investor’s actual ability to absorb risk without impairing the objective.