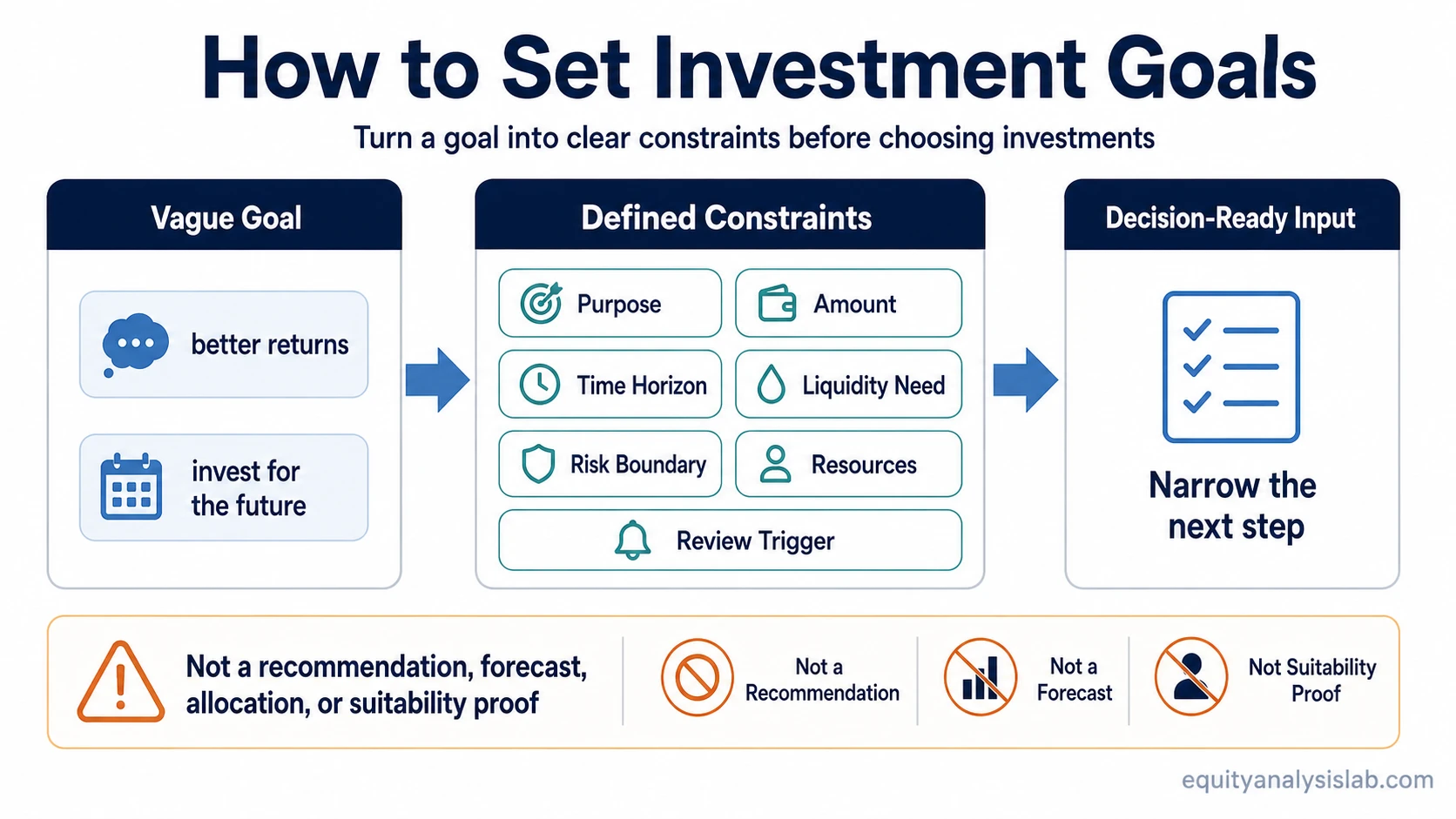

Setting investment goals means turning a financial objective into clear investing constraints: the amount needed, time horizon, acceptable risk boundary, liquidity need, and review trigger.

A goal is not useful for investing just because it sounds desirable. It becomes useful when it defines enough information to narrow decisions without pretending to identify the right stock, fund, account, or allocation.

At that point, the goal starts to behave like a decision input rather than a wish. It can help separate money that may need stability, money that can remain invested longer, and money that should not be exposed to uncertainty before a known deadline.

Key Points

- A usable investment goal includes amount, time horizon, risk boundary, liquidity need, and a review trigger.

- A vague goal is not enough evidence to choose an investment.

- Goal-setting narrows the decision, but it does not prove suitability, expected return, or safety.

What Makes an Investment Goal Usable?

An investment goal is usable when it answers the practical constraints around the objective. The goal should show what the money is for, when it may be needed, how much flexibility exists, and what kind of risk would make the plan unsuitable.

The useful distinction is between a vague preference and a defined objective. “I want higher returns” is a preference. “I need a defined amount within a defined period and cannot accept a large drawdown near the deadline” is closer to a usable goal.

When those constraints are clear, the goal can connect to broader investment objective planning without replacing the full objective-setting process.

Inputs Needed Before a Goal Can Guide Investing

A goal evidence check helps prevent a common mistake: moving from a desired outcome straight to an investment product. The better sequence is to define the decision inputs first.

| Input | What it answers | Why it matters for investing |

|---|---|---|

| Goal purpose | What the money is meant to support | Separates a real objective from a general wish for growth |

| Target amount | How much capital may be needed | Shows whether the goal is measurable or still too vague |

| Time horizon | When the money may be needed | Helps distinguish short, medium, and longer-term constraints |

| Liquidity need | Whether part of the money must remain accessible | Prevents locking all capital into a structure that may not fit the deadline |

| Risk boundary | How much uncertainty would make the goal unacceptable | Creates a constraint before investment selection begins |

| Available savings or contributions | What resources can support the goal over time | Tests whether the goal is realistic enough to evaluate |

| Review trigger | What would require the goal to be updated | Keeps the goal from becoming stale when circumstances change |

These inputs are not a formula for selecting an asset. They are a filter for deciding whether the goal is defined enough to inform the next step.

Weak vs Usable Investment Goals

A weak goal usually sounds clear at first but fails when it is tested against time, amount, and risk. It may express direction, but not enough evidence to guide an investing decision.

| Weak goal | What is missing | More usable version |

|---|---|---|

| I want better returns. | No amount, time horizon, risk boundary, or purpose | I want to grow a defined sum over five years, keep near-term cash separate, and avoid relying on assets that could be materially down when the money is needed. |

| I want to invest for the future. | No deadline, contribution plan, or review condition | I want to build capital for a long-term objective, review the plan annually, and reassess it if income, expenses, or risk capacity changes. |

| I need money in a few years. | No target amount or tolerance for interim loss | I need a defined amount in about five years and should avoid relying on assets that could be materially down when the money is required. |

The stronger versions are still not recommendations. They simply contain enough information to begin evaluating whether an investment approach fits the goal.

Short-Term vs Long-Term Investment Goals

Short-term and long-term goals should not be treated as labels only. The time horizon changes how much uncertainty the goal can absorb before the deadline.

A shorter horizon usually leaves less room for recovery from market declines before the money is needed. A longer horizon may allow more flexibility, but it still needs a risk boundary, a contribution plan, and a reason to review the goal when facts change.

The time horizon also interacts with the investor’s knowledge boundary. A goal can look clear on paper, but the decision still needs to stay inside the investor’s circle of competence before specific investments are considered.

Common Mistakes When Setting Investment Goals

- Starting with a product: Choosing a stock, fund, or account before defining the goal can make the decision backward.

- Using return targets as the whole goal: A desired return does not define the amount needed, deadline, or acceptable risk.

- Ignoring liquidity: Money that may be needed soon should not be treated the same as capital with a longer time horizon.

- Leaving risk undefined: A goal without a risk boundary can become difficult to evaluate during market stress.

- Failing to review the goal: Income changes, spending needs, family obligations, or a shorter remaining horizon can all change the goal’s usefulness.

How Goals Connect to Investment Objectives

An investment goal becomes more decision-ready when it can be translated into an objective. The goal states what the investor is trying to accomplish. The objective adds the constraints that make the goal usable for analysis.

For example, “grow capital” is broad. “Grow capital over a long horizon while maintaining a defined liquidity reserve and avoiding exposure that would exceed the investor’s risk boundary” is more useful. It does not select the investment, but it narrows the field of acceptable choices.

This distinction matters because objectives organize decisions. They do not prove that any specific security, fund, or strategy is appropriate.

How Goals Fit Into Written Investment Rules

Once the goal and constraints are clear, they can later be documented as part of written investment rules. That documentation may include the objective, time horizon, liquidity needs, risk limits, review schedule, and conditions that would require a change.

A written process can reduce inconsistency because the investor is not redefining the goal every time markets move. The documented rules in an investment policy statement can help keep the original constraints visible during later decisions.

The written rules should not be treated as permanent. A goal should be reviewed when the deadline gets closer, income changes, liquidity needs change, or the investor’s ability to tolerate loss changes.

What Investment Goals Cannot Prove

Investment goals organize constraints. They do not guarantee returns, remove uncertainty, or prove that an investment is suitable.

A clear goal can still be paired with a weak investment choice. A realistic deadline can still face market volatility. A well-defined risk boundary can still be tested by events that were not expected when the goal was written.

The purpose of setting the goal is narrower: make the decision more testable before moving into investment selection, portfolio construction, or written policy rules.

FAQ

What is the first step in setting investment goals?

The first step is to define the objective in measurable terms. That usually means naming the purpose, target amount, time horizon, liquidity need, risk boundary, and review trigger before looking at investments.

Are investment goals the same as investment objectives?

No. A goal describes what the investor wants to accomplish. An investment objective turns that goal into clearer constraints that can guide decisions.

Can a goal tell me which investment to choose?

No. A goal can narrow the decision, but it does not identify the correct investment or prove suitability. Investment selection requires separate analysis.