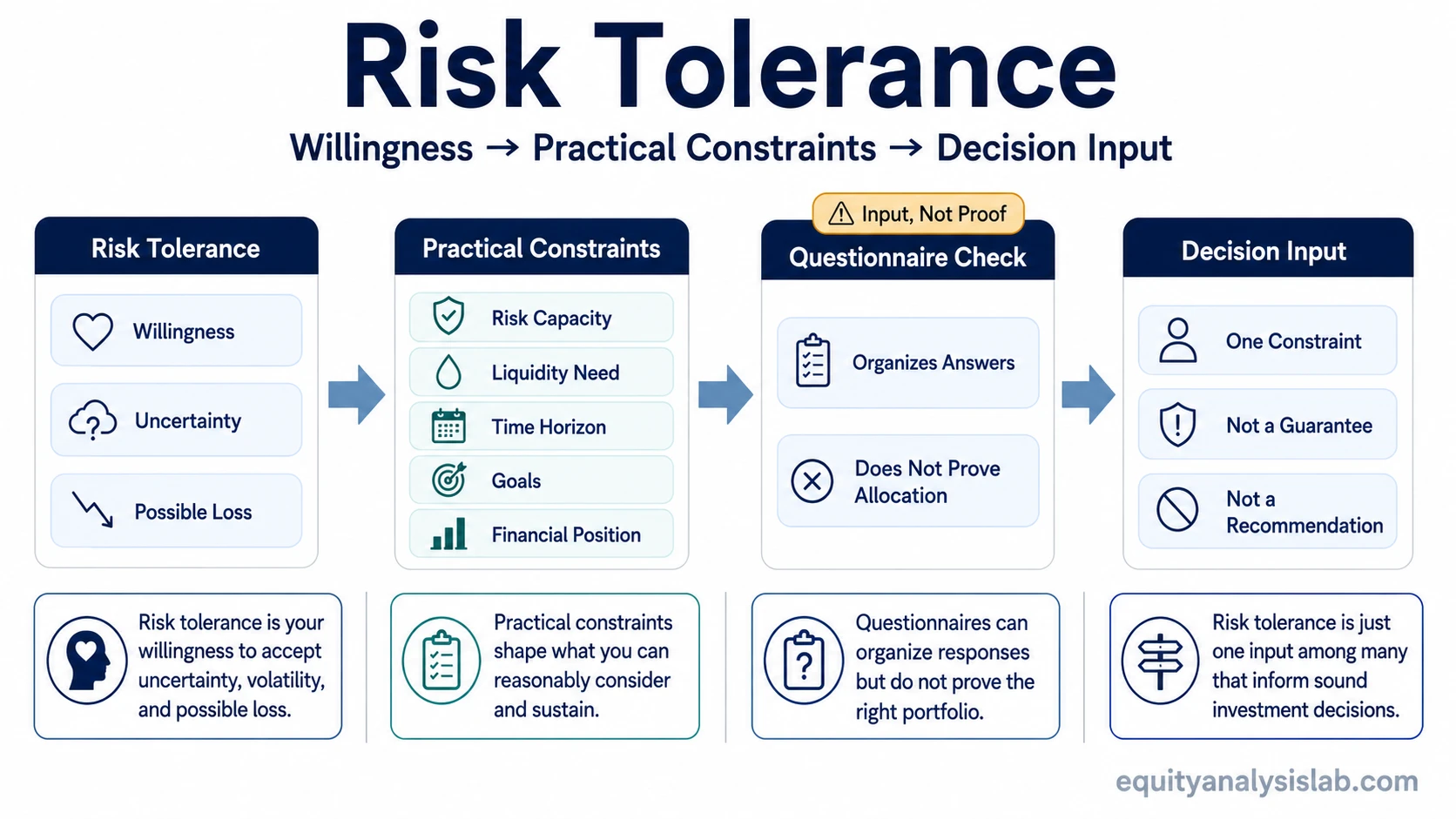

Risk tolerance is an investor’s willingness to accept uncertainty, volatility, and possible loss while pursuing an investment objective. It is one input in the investor decision process, not a portfolio prescription, suitability proof, return forecast, or guarantee that a specific investment choice is appropriate.

In investing, risk tolerance describes the comfort side of risk. It asks how much fluctuation, drawdown pressure, and uncertainty an investor can realistically tolerate without abandoning the plan or making inconsistent decisions. That comfort level matters, but it must be separated from the investor’s actual ability to absorb financial loss.

Key Points About Risk Tolerance

- Risk tolerance is about willingness to accept uncertainty and possible loss.

- It is shaped by goals, time horizon, liquidity needs, financial position, experience, and behavior during volatility.

- It is not the same as the ability to absorb financial damage.

- A questionnaire can help organize answers, but it does not prove the correct portfolio.

- Higher risk tolerance is not automatically better, and lower risk tolerance is not automatically safer.

What Risk Tolerance Means in Investing

Risk tolerance means the degree of investment uncertainty an investor is willing to accept. The uncertainty may appear as price volatility, temporary loss, unclear timing, or the possibility that an investment result differs from the expected outcome.

The useful distinction is that risk tolerance is psychological and behavioral, not only mathematical. Two investors can face the same market decline and react differently. One may remain calm because the decline fits the original plan. Another may feel pressure to sell because the loss feels larger than expected, even if the long-term objective has not changed.

That does not make risk tolerance a license to take more risk. It only describes one constraint that should be considered alongside objective factors such as income stability, cash needs, time horizon, debt, and investment purpose.

What Shapes an Investor’s Risk Tolerance

Risk tolerance is influenced by both personal comfort and decision context. An investor’s past experience with market declines can affect how future volatility feels. A longer time horizon may make some uncertainty easier to tolerate, while a near-term cash need can make the same uncertainty harder to accept.

| Input | What it can reveal | Important limitation |

|---|---|---|

| Time horizon | How long the investor expects capital to remain invested. | A long horizon does not automatically mean high tolerance. |

| Liquidity needs | Whether cash may be needed before an investment has time to recover. | Comfort with risk cannot override a real cash requirement. |

| Investment goals | What the investor is trying to fund or preserve. | A goal can define purpose without proving how much risk is acceptable. |

| Financial position | How much loss or income disruption the investor may be able to withstand. | This belongs closer to capacity than emotional tolerance. |

| Past behavior | How the investor has reacted to volatility or uncertainty before. | Past behavior is informative, but future stress can still differ. |

| Questionnaire answers | How the investor describes comfort with losses, volatility, and uncertainty. | Answers can be inconsistent with real behavior under pressure. |

For that reason, setting investment goals should not be isolated from risk discussion. A goal gives risk tolerance a purpose, while risk tolerance helps test whether the investor can remain aligned with that purpose when results become uncertain.

Risk Tolerance vs Risk Capacity

Risk tolerance is willingness. Risk capacity is the ability to absorb financial damage. The two can point in different directions, which is why they should not be merged into one label.

An investor may feel comfortable with market volatility but still have limited room for loss because cash will be needed soon. Another investor may have strong financial capacity but low emotional comfort with large swings. In both cases, the risk discussion changes when willingness and the ability to absorb financial loss are evaluated separately.

This boundary keeps risk tolerance from becoming too broad. It does not replace income analysis, liquidity planning, debt review, time-horizon review, or the broader investment decision process.

How Questionnaires Can Help and Where They Fall Short

A risk tolerance questionnaire can help organize how an investor thinks about uncertainty, loss, volatility, and decision pressure. It can also expose contradictions, such as saying that long-term growth is the goal while also saying that any short-term loss would be unacceptable.

The limitation is that a questionnaire is a self-assessment tool, not proof of the right investment mix. Answers may change after a real decline, a job loss, a large expense, or a shift in family obligations. A questionnaire can support the discussion, but it should not replace judgment about goals, capacity, liquidity, and constraints.

Common Misunderstandings About Risk Tolerance

Higher tolerance is not automatically better. A high tolerance label can describe comfort with uncertainty, but it does not prove that taking more risk is appropriate, necessary, or affordable.

Conservative tolerance is not automatically safer. Avoiding volatility can reduce one type of discomfort while introducing other issues, such as failing to match the objective or time horizon. The label alone does not decide the tradeoff.

Aggressive, moderate, and conservative labels are only categories. They can help describe broad preferences, but they are not universal allocation rules. The same label can mean different things depending on goals, liquidity needs, time horizon, tax situation, and financial capacity.

Risk tolerance does not replace objective framing. An investor still needs a clear purpose for the capital. That is where formal objective framing becomes separate from emotional comfort with uncertainty.

When Risk Tolerance and Practical Constraints Point Different Ways

Consider a generic investor who says they are comfortable with large market swings because they understand that equity investments can fluctuate. If that same investor also expects to use part of the money for a near-term obligation, the emotional willingness to accept volatility may be higher than the practical ability to wait through a decline.

The scenario shows why risk tolerance should be treated as one input, not the final answer. Comfort with volatility can support a decision, but it cannot override timing, liquidity, and capacity constraints.

How to Assess Risk Tolerance Without Overreading It

Risk tolerance can be assessed by combining self-reflection, questionnaire responses, past behavior, and the investor’s broader decision context. The goal is not to find a perfect label. The goal is to understand whether the investor can stay aligned with a plan when uncertainty becomes visible.

Useful questions include how the investor reacted during previous declines, how much temporary loss would create pressure to change course, whether the money has a defined near-term use, and whether the investor understands the type of investment being considered. Understanding the investment universe also matters, which is where a circle of competence can help separate familiar risks from risks the investor does not yet understand.

The strongest assessment is usually not a single score. It is a consistent view across stated comfort, observed behavior, financial capacity, liquidity needs, and investment purpose.

Risk Tolerance FAQ

What is risk tolerance in investing?

Risk tolerance is an investor’s willingness to accept uncertainty, volatility, and possible loss while pursuing an investment objective. It describes comfort with risk, not a guaranteed investment choice.

Is risk tolerance the same as risk capacity?

No. Risk tolerance is willingness to accept risk, while risk capacity is the ability to absorb financial loss. An investor can have high tolerance but limited capacity, or strong capacity but low tolerance.

Can a risk tolerance questionnaire determine the right portfolio?

No. A questionnaire can help organize preferences and reveal contradictions, but it does not prove suitability, prescribe an allocation, or replace review of goals, liquidity needs, time horizon, and financial capacity.

Is high risk tolerance always better?

No. High risk tolerance only means the investor may be more willing to accept uncertainty and possible loss. It does not mean that taking more risk is appropriate, necessary, or financially sustainable.