A three fund portfolio is a simple investing framework that usually combines broad domestic stock exposure, international stock exposure, and bond exposure. The fund count makes the idea easy to recognize, but the real portfolio is defined by the exposures, weights, costs, distributions, account placement, and rebalancing rule behind those three sleeves.

Definition: A three fund portfolio is an investing framework built around three broad portfolio sleeves: a domestic stock sleeve, an international stock sleeve, and a bond or fixed-income sleeve. The framework can be implemented through different fund vehicles, but the label does not prescribe a specific allocation, fund provider, account type, or maintenance rule.

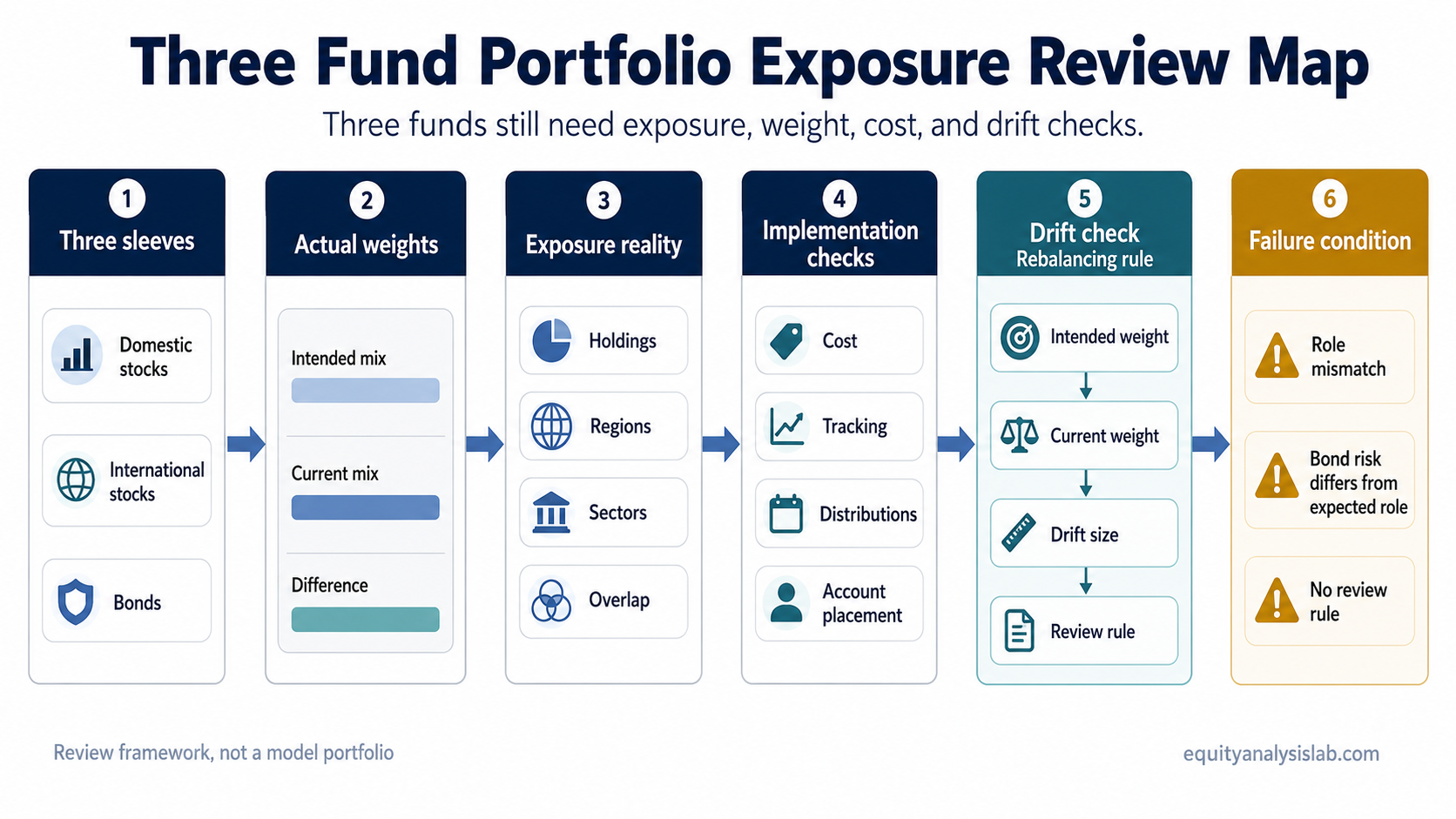

The useful question is not only whether the portfolio has three funds. The stronger question is whether those three holdings still represent the intended risk mix after fees, market movement, distributions, overlap, tax location, and drift are considered.

Key Points

- A three fund portfolio usually separates domestic stocks, international stocks, and bonds into three broad sleeves.

- The same three sleeves can create very different portfolios when the weights change.

- Fund count does not prove diversification unless the underlying holdings, exposures, and concentration are checked.

- Costs, tracking, distributions, and account placement can change how clean the simple setup feels in practice.

- Rebalancing turns the three-fund idea into a repeatable review process, not an automatic transaction rule.

What a Three Fund Portfolio Is

A three fund portfolio is built around broad market exposure rather than individual security selection. The domestic stock sleeve gives exposure to the home equity market, the international stock sleeve adds non-domestic equity exposure, and the bond sleeve adds fixed-income exposure that can change the portfolio’s volatility, income profile, and drawdown behavior.

The approach is often associated with low-maintenance investing because each sleeve can be broad, diversified, and relatively easy to monitor. That simplicity does not remove the need to decide how much belongs in each sleeve, how the funds are held, and how the portfolio will be checked over time.

When the stock sleeves are implemented through market-tracking funds, the vehicle often resembles an index ETF or a similar index-based fund structure. The vehicle is secondary to the exposure question: what market is being owned, how broad the exposure is, and whether the fund behaves as expected relative to its benchmark.

What the Three Sleeves Are Meant to Cover

The three sleeves each have a different job. The domestic equity sleeve usually carries the main home-market growth exposure. The international equity sleeve adds exposure to foreign companies, currencies, markets, and regional cycles. The bond sleeve adds fixed-income exposure, which may serve a stability, income, or risk-balancing role depending on the fund type and the investor’s broader plan.

| Sleeve | Typical role | Review question |

|---|---|---|

| Domestic stocks | Broad home-market equity exposure | Does the fund represent the intended domestic equity market, or is it concentrated in a narrow segment? |

| International stocks | Non-domestic equity exposure | Does the fund add meaningful foreign exposure, or does it overlap heavily with global companies already held elsewhere? |

| Bonds or fixed income | Fixed-income exposure, income profile, and possible volatility dampening | Does the bond ETF or bond fund match the intended duration, credit, currency, and risk role? |

A broad label can hide important differences. A short-duration government bond fund, an aggregate bond fund, and a long-duration credit fund can all sit inside a bond sleeve, but they do not carry the same interest-rate risk, credit risk, or income behavior.

Why the Weights Matter More Than the Fund Count

The three-fund label says little until the weights are visible. A portfolio with 80% stocks and 20% bonds behaves differently from one with 50% stocks and 50% bonds, even if both use the same three categories. The weight mix is the main bridge between the simple label and the actual risk exposure.

Asset allocation determines how much of the portfolio is exposed to equity risk, fixed-income risk, currency exposure, and market drawdown risk. The three-fund structure can organize that mix, but it does not decide the mix by itself.

Limitation: There is no official allocation that makes a three fund portfolio suitable by default. Risk capacity, time horizon, income needs, account structure, and behavioral tolerance can all change whether a simple three-sleeve mix still fits.

The Three-Fund Exposure Reality Check

The strongest use of the framework is as an exposure check. The label suggests simplicity, but the underlying holdings decide whether the portfolio still matches the intended risk mix.

| What the label suggests | What must be checked | What can break the assumption |

|---|---|---|

| Three funds means broad diversification | Underlying holdings, sector exposure, region exposure, and issuer concentration | The funds overlap or concentrate heavily in the same large companies, sectors, or regions |

| Domestic plus international stocks means global equity exposure | Country mix, currency exposure, developed versus emerging market exposure, and global company overlap | The international sleeve adds less diversification than expected or introduces risks the investor did not intend |

| The bond sleeve lowers portfolio risk | Duration, credit quality, currency exposure, yield source, and correlation behavior | The bond sleeve carries more interest-rate or credit risk than the stabilizing role requires |

| Low fund count means low maintenance | Rebalancing rule, review frequency, tax friction, and account placement | The portfolio drifts for years because the simple design creates a false sense of completion |

| Broad funds mean clean implementation | Expense ratios, tracking difference, bid-ask spreads, distributions, and fund structure | The implementation creates avoidable cost, tax, or tracking friction |

Costs, Tracking, Distributions, and Account Structure

A three fund portfolio can look clean at the asset-class level while still carrying implementation details that matter. Costs reduce the return captured by the investor. Tracking difference shows how closely a fund follows its intended benchmark. Distributions can create cash flow, reinvestment, and tax considerations. Account placement can change where friction appears.

These checks do not require a fund-shopping list. They require one basic question for each sleeve: does the vehicle deliver the intended exposure in a cost-aware, understandable, and maintainable way?

| Implementation check | Why it matters | Safe interpretation |

|---|---|---|

| Expense ratio and trading cost | Costs affect the amount of market return retained over time | Lower cost can help, but cost alone does not prove suitability |

| Tracking behavior | A broad fund should behave reasonably close to the exposure it claims to represent | Large or persistent differences deserve attention before assuming the sleeve is doing its job |

| Distributions | Dividends, interest, and capital-gain distributions can affect cash flow and tax handling | Distribution behavior should be understood without turning portfolio review into tax advice |

| Account placement | Taxable and tax-advantaged accounts can handle distributions and turnover differently | Account structure can matter, while detailed tax planning may require qualified guidance |

Rebalancing and Drift

Market movement changes the portfolio even when no new fund is added. A stock-heavy sleeve can grow faster than the bond sleeve during an equity advance. A bond-heavy sleeve can become larger after an equity decline. Over time, the actual weights may no longer match the intended weights.

Portfolio rebalancing is the process that compares current weights with intended weights. A drift check can lead to a decision to rebalance, wait, contribute differently, or reassess the plan. It does not automatically prove that a trade is required.

Review sequence: intended weight → current weight → drift size → account impact → cost and tax friction → decision rule. The sequence keeps the three-fund framework observable instead of relying on the label alone.

When a Three Fund Portfolio May Stop Fitting

A three fund portfolio can stop fitting even when the fund count has not changed. The problem usually comes from a mismatch between the original role and the current portfolio reality.

Common mistake: Treating three funds as automatic diversification proof. The stronger review starts with actual exposures, weights, overlap, concentration, cost, distributions, and drift.

Failure condition: The framework weakens when the three sleeves no longer match the intended risk mix, when the bond sleeve carries a different risk than expected, when equity exposure becomes too concentrated, when account placement creates avoidable friction, or when the portfolio has no repeatable review rule.

The structure remains stronger when each sleeve still has a clear role, the current weights remain close to the intended mix, and the maintenance rule is explicit. If one of those conditions breaks, the answer may be a changed weight, a clearer maintenance rule, a different fund vehicle, a better account-location decision, or no change after the mismatch is judged immaterial.

Three Fund Portfolio vs Nearby Approaches

A three fund portfolio often sits near other simple investing approaches, but the concepts are not identical. The distinction matters because each approach solves a different problem.

| Approach | Main idea | Main boundary |

|---|---|---|

| Three fund portfolio | Uses three broad sleeves for domestic stocks, international stocks, and bonds | Still requires weight, exposure, cost, account, and drift checks |

| Target-date fund | Packages allocation and glide-path decisions into one fund structure | Gives less direct sleeve control and still requires understanding the underlying allocation |

| Lazy portfolio | Emphasizes low-maintenance portfolio design | Can use more or fewer than three funds and may follow different allocation logic |

| ETF portfolio build | Focuses on selecting and combining ETF exposures | Can become product-selection heavy unless the exposure logic stays clear |

Three Fund Portfolio Example in Context

An investor begins with three broad sleeves: domestic stocks, international stocks, and bonds. After a strong equity period, the two stock sleeves become a larger share of the portfolio than intended, while the bond sleeve becomes smaller. The portfolio still has three funds, but the actual risk mix has changed.

The first check is the current equity and bond weight. The second check is whether the international sleeve adds meaningful diversification or mostly repeats the same large global companies. The third check is whether the bond sleeve still matches the intended fixed-income role. The fourth check is whether rebalancing would create cost, tax, or account-location issues that should be considered before acting.

The setup remains useful when it makes those checks visible. It becomes weaker when the simple label replaces the maintenance process.

FAQ

What are the three funds in a three fund portfolio?

The three sleeves are usually domestic stocks, international stocks, and bonds. The exact funds can vary by market, account type, fund provider, and investor constraints, so the structure should be reviewed by exposure rather than by ticker.

Does a three fund portfolio have an official allocation?

No. The framework defines broad sleeves, not a universal weight. Allocation depends on risk capacity, time horizon, income needs, account structure, and the role each sleeve is meant to play.

Is a three fund portfolio the same as a lazy portfolio?

Not exactly. A three fund portfolio can be a type of low-maintenance portfolio, but lazy portfolios can use different numbers of funds, different asset classes, and different allocation rules.

Can a three fund portfolio become too risky?

Yes. If equity sleeves grow beyond the intended mix, if the bond sleeve carries more risk than expected, or if the investor’s risk capacity changes, the same three funds can represent a different risk profile than originally intended.