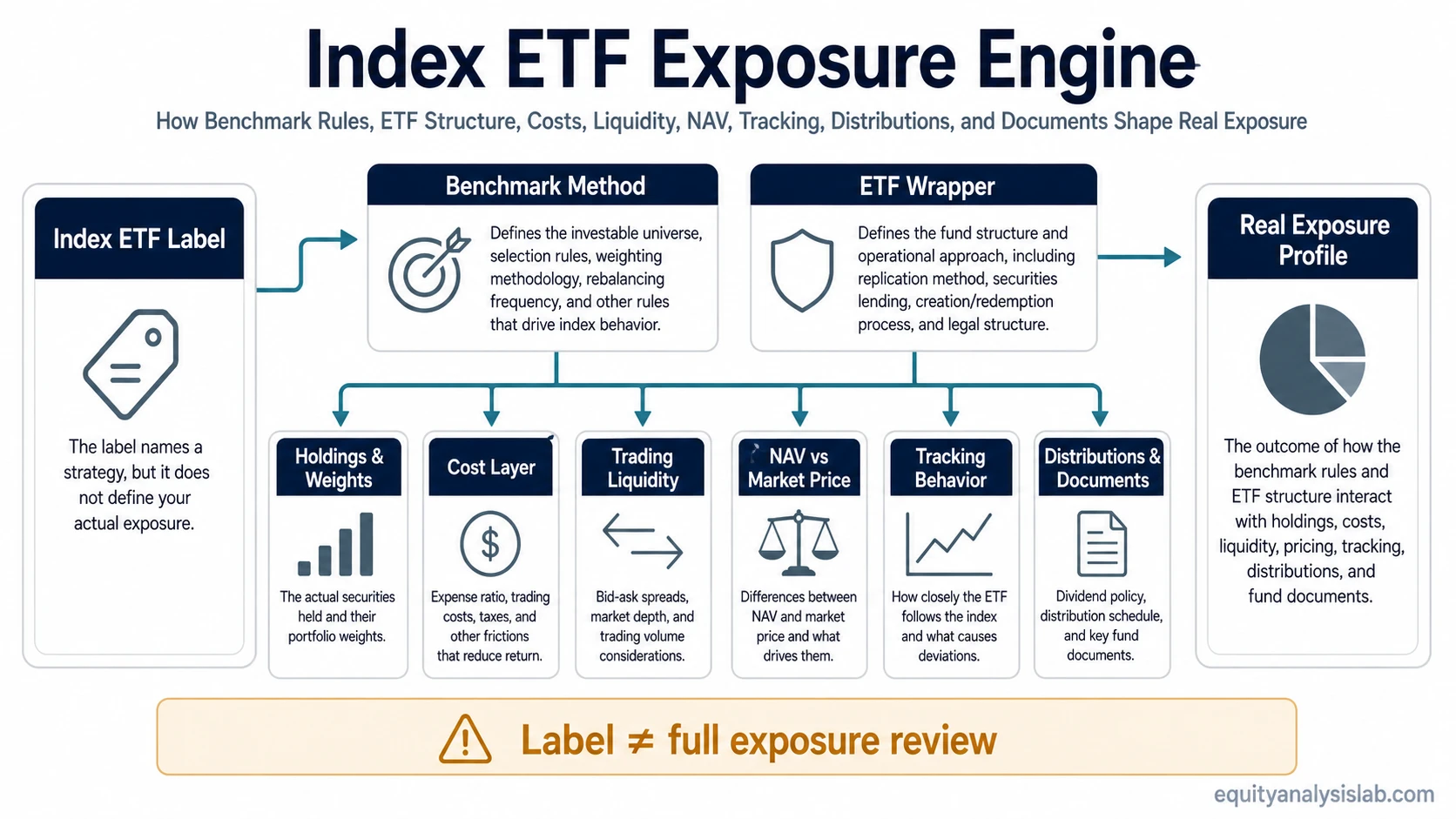

An index ETF is an exchange-traded fund designed to track a specified market index or index segment. The label identifies the tracking objective, but it does not fully describe the exposure an investor receives. Actual exposure depends on the index rules, holdings, weighting method, costs, tracking behavior, trading liquidity, market price versus NAV, distributions, and fund structure.

Definition: An index ETF is an ETF that seeks to follow the performance of a benchmark index by holding, sampling, or otherwise referencing the securities or assets represented by that index.

The useful distinction is that “index” describes the benchmark method, while “ETF” describes the exchange-traded fund wrapper. An index fund can also be structured as a mutual fund, so the index label and the ETF wrapper should be read as two separate parts of the exposure profile.

Key Points

- An index ETF tracks a benchmark index, such as a broad market index, sector index, factor index, bond index, commodity-linked index, or other defined index segment.

- The ETF wrapper means the fund trades on an exchange, so market price, bid-ask spread, trading volume, and premium or discount to NAV can affect the investor’s experience.

- Tracking is an objective, not a guarantee. Fees, sampling, rebalancing, cash drag, liquidity, and implementation choices can create differences from the index return.

- Two index ETFs with similar labels can still differ because their indexes, holdings, weighting rules, costs, distributions, and structures are not identical.

What Is an Index ETF?

An index ETF combines an index-tracking mandate with an exchange-traded fund structure. The fund usually seeks to mirror a defined benchmark by owning the benchmark’s components, holding a representative sample, or using another permitted method described in its fund documents.

The benchmark may be broad or narrow. It may cover a total stock market, a large-cap segment, a sector, a country, a bond market, a commodity-linked index, a dividend screen, a factor rule set, or another rules-based exposure category. The index methodology matters because it decides what belongs in the benchmark and how each component is weighted.

The ETF structure matters separately because the investor buys and sells ETF shares on an exchange. That adds practical observables that do not exist in the same way for traditional mutual funds, including intraday market price, bid-ask spread, trading volume, and premium or discount to net asset value.

How an Index ETF Tracks an Index

An index ETF begins with a benchmark. The benchmark sets the eligible universe, inclusion rules, weighting method, rebalancing schedule, and sometimes concentration limits. The ETF then tries to translate that benchmark into a fund portfolio.

| Tracking element | What it controls | Why it matters |

|---|---|---|

| Benchmark selection | The index or index segment the ETF seeks to follow. | Similar names can hide different market coverage, sector exposure, country exposure, or security-selection rules. |

| Holdings method | Whether the ETF fully replicates the index, samples it, or uses another permitted implementation method. | Implementation choices can affect tracking, liquidity needs, turnover, and concentration. |

| Weighting method | How much influence each holding has inside the benchmark. | Market-cap weighting, equal weighting, factor weighting, or rules-based weighting can produce different risk and return behavior. |

| Rebalancing | When the index and fund adjust holdings to match updated rules. | Rebalancing can create turnover, trading costs, tax effects, and temporary tracking differences. |

| Tracking difference | The gap between ETF performance and the benchmark over a period. | Fees, cash holdings, trading costs, sampling, securities lending, and timing differences can prevent perfect index matching. |

Full replication is easier to understand: the fund holds the index components in similar weights. Sampling is more selective: the fund holds a representative portfolio intended to behave like the index. Sampling can be practical for large, illiquid, or complex benchmarks, but it also makes the implementation layer more important to review.

What Can Make Two Index ETFs Different

Two index ETFs can look similar at the label level while delivering different exposure profiles. A broad market label, sector label, dividend label, or factor label is only the starting point. The details decide what the investor actually owns, how the fund trades, and how closely it follows the benchmark.

| Exposure checkpoint | Question to ask | Possible interpretation issue |

|---|---|---|

| Index rules | What does the benchmark include, exclude, and rebalance? | The same category label can produce different holdings if the rules are different. |

| Holdings and concentration | How much of the ETF is controlled by the largest holdings, sectors, countries, or issuers? | A fund can be diversified by holding count while still concentrated by weight. |

| Expense ratio | What ongoing fund cost is deducted from the portfolio? | Costs affect tracking, but the lowest listed fee is not the only exposure variable. |

| Liquidity and spread | How actively does the ETF trade, and how wide is the bid-ask spread? | Thin trading or wide spreads can increase trading friction, especially for larger or less liquid orders. |

| NAV versus market price | Does the ETF trade close to its net asset value? | Premiums and discounts can appear when market price and underlying portfolio value diverge. |

| Distribution profile | What income, capital gain, or other distributions can the fund make? | Distributions affect investor cash flows and may have tax consequences that depend on the investor and jurisdiction. |

| Fund structure and documents | What structure, distribution policy, and fund-document disclosures apply? | Legal, distribution, and tax details are fund- and jurisdiction-specific, so they require fund documents and tax review rather than a generic ETF label. |

Example: Two index ETFs may both appear to track the same broad market category, but one may follow a broader benchmark while the other uses different weighting rules, trades with wider spreads, or distributes income differently. The label gives the category; the exposure checklist explains the mechanics behind that category.

Index ETF vs Index Fund

An index ETF is a type of index fund, but not every index fund is an ETF. The index fund idea describes a fund that tracks an index. The ETF wrapper describes a fund whose shares trade on an exchange during the trading day.

A traditional index mutual fund also tracks an index, but it usually transacts with the fund company at end-of-day net asset value rather than through intraday exchange trading. That difference changes the trading experience, not necessarily the benchmark objective.

Core boundary: Index tracking answers “what is the fund trying to follow?” The ETF wrapper answers “how do investors buy and sell fund shares?” Confusing those two layers can make ETF exposure look simpler than it is.

Index ETF vs Nearby ETF Types

An index ETF is different from an actively managed ETF because the index ETF starts with a benchmark rule set, while active management gives the manager discretion to select, avoid, overweight, or underweight holdings within the fund’s mandate.

Asset exposure can also change the analysis. Bond ETFs add fixed-income variables such as duration, credit quality, yield behavior, and bond-market liquidity.

Commodity exposure through ETFs can involve physical holdings, futures, derivatives, producer equities, or baskets, so commodity ETF structures require a separate exposure check.

The neighboring categories matter because “index ETF” describes a tracking style and wrapper, not a complete statement about asset class, risk profile, tax treatment, or portfolio role.

Limits of Index ETF Exposure

Index ETFs can make market exposure easier to access, but the structure does not remove the need to understand what the fund tracks and how it operates. A benchmark can be concentrated, narrowly defined, heavily tilted toward a few companies or sectors, or exposed to risks that are not obvious from the category name alone.

Key limitation: Tracking an index does not mean matching the index perfectly, avoiding losses, guaranteeing diversification, or creating a complete portfolio by itself.

Tracking can differ because of expense ratios, cash balances, sampling, rebalancing, trading costs, securities lending, market closures, currency effects, or liquidity constraints. Market price can also differ from NAV, particularly when underlying assets are less liquid or when trading stress affects the ETF market.

Tax and distribution outcomes should be handled carefully. ETF structure can influence distribution mechanics, but tax impact depends on the fund, account type, investor location, holding period, and applicable rules. Generic ETF structure is not a substitute for reading the fund documents or obtaining tax guidance where needed.

FAQ

Is an index ETF the same as an index fund?

An index ETF is one form of index fund, but index funds can also be structured as mutual funds. The index part describes the benchmark objective, while the ETF part describes the exchange-traded wrapper.

Can an index ETF fail to match its index?

An index ETF can differ from its benchmark because of fees, trading costs, sampling, rebalancing, cash holdings, liquidity conditions, and other implementation factors. Tracking is an objective, not a guarantee.

Why can two index ETFs with similar labels behave differently?

Similar labels can hide differences in benchmark rules, holdings, weighting, concentration, costs, liquidity, NAV behavior, distributions, and structure. The exposure profile depends on those details, not only on the fund label.